Braemar have now released their full year results for the year ending 2014.

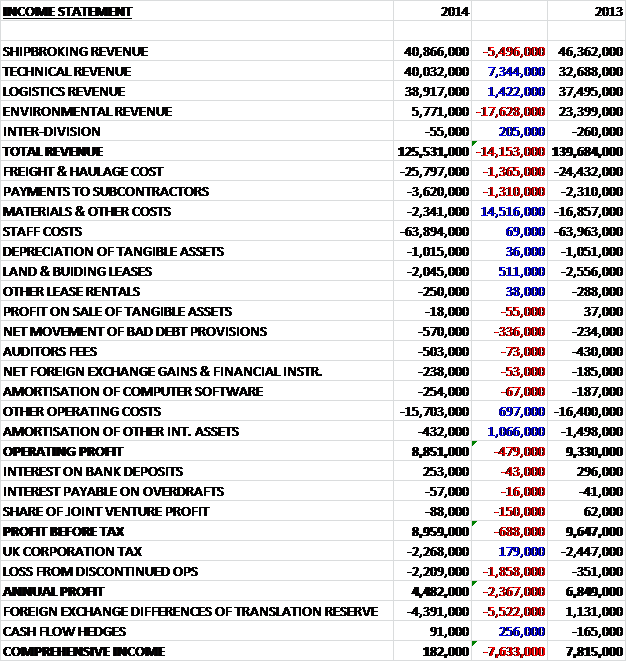

Overall revenues were down by a considerable £14.2M on last year. This was driven by a £17.7M decline in Environmental revenue as the work on the Rena finished and a £5.5M fall in Shipbroking revenue due to a difficult market. These falls were somewhat mitigated by a £7.3M increase in Technical Revenue and a small hike in Logistics revenues. Costs have also decreased over the last year, predominantly driven by the £14.5M fall in Material costs relating to the Environmental division. There was also a decrease in the amortisation of intangibles and other operating costs, somewhat counteracted by increases in freight and haulage costs, and subcontractor payments. This all gives an operating profit some £480K lower than last year. The group made a small loss on the joint venture compared to a small gain last year to give the profit from continuing operations £688K lower at just under £9M. When the £2.2M loss from the discontinued operation (including the £800K loss on disposal) and the tax paid is taken into account, however, the annual profit for the year is £4.5M, £2.4M lower than in 2013. Not really a bad performance given the end of the Environmental work and the loss making business that was sold.

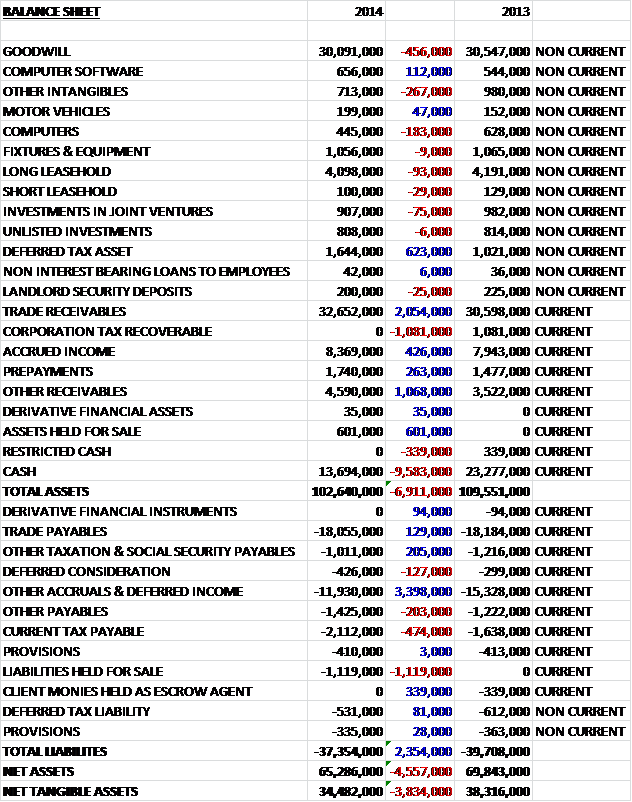

Overall, total assets fell by just under £7M over last year. This was driven by a £9.6M decline in cash levels and the lack of £1.1M in recoverable corporation tax. These increases were partically mitigated by a £2.1M increase in trade receivables and a £1.1M growth in other receivables. The small fall in Goodwill relates to goodwill associated with the sold Casbarian business. Liabilities also fell when compared to last year, predominantly driven by a £3.4M reduction in accruals and deferred income. The Deferred consideration represents the potential payment with regards to the Lawrence Holt acquisition. Overall these changes meant that net tangible assets were some £3.8M lower at £34.5M which is a little disappointing, although it should be noted that due to the strong Sterling, translation differences adversely affected the balance sheet to the tune of £4.4M.

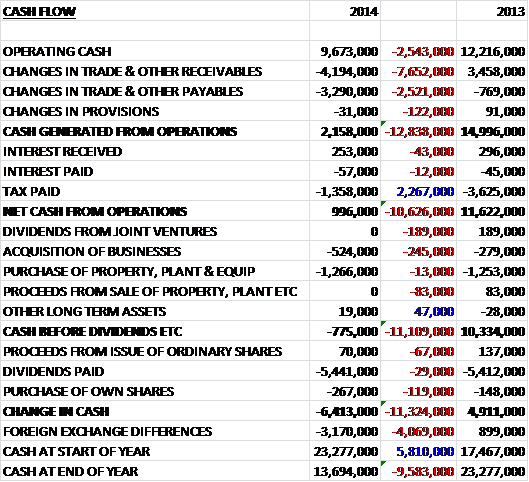

Before the movement in working capital, cash profits were some £2.5M lower at £9.7M. A large increase in receivables and decrease in payables, apparently due to a shift in the business mix towards the Technical division and the higher level of revenue in the final quarter of the year, meant that cash generated was just £2.2M, a huge £12.8M less than in 2013. The group did pay less tax though, which meant that net cash from operations, at just £1M was down by £10.6M. The group then spent £1.3M on capital expenditure and £500K on acquisitions so before any financing issues the group had a cash outflow of £775K. The £5.4M spent on dividends then took the outflow to a rather unsustainable £6.4M, an £11.3M reverse when compared to last year, although the group did receive £2M from the LNG Engineering contract just after year end.

The discontinued operations referenced throughout the income statement relates to Casbarian, part of the Technical division. It was decided that it did not align with the other businesses and was sold to the local management team in March, generating a loss on disposal of £800K. The group also completed the sale of the Morrison Tours business from the Logistics division that provided on-shore excursions for passenger cruise ships in Scotland. In October, the group acquired Lawrence Holt Ltd, based in Felixstowe, generating £278K of goodwill from an initial £200K cash consideration and deferred consideration of £426K.

The Shipbroking division had an operating profit of £2.6M, down by 51% on last year. The shipping market continued to suffer from over capacity by some 25%, not helped by recent new builds as ship owners look to own cheaper, more efficient vessels, and therefore supply growth as continued to run ahead of demand, supressing charter rates. The market for oil tankers is changing rapidly as US domestic crude oil from unconventional sources replaces their reliance on imports with the displaced tonnage now refined closer to source in the Middle East and India. In addition, there have been some European refinery closures, meaning higher petroleum product imports from a variety of sources. This has had the effect of reducing demand for crude oil tankers and increasing demand for product tankers. An improvement in freight rates for Deep sea Tankers was apparent in the second half of the year, driven by a trend for slow steaming which helped spread the tonnage and some improvement is expected for next year. For specialised tankers, results were similar to last year but the forward order book has grown substantially due to the conclusion of long term charter business exporting shale gas from the US to Europe, commencing in 2015. There are also signs that revenue will improve next year from spot and contracts being renewed at a higher rate. The group opened e new office in Oslo during the year which is also expected to contribute to revenues.

The dry cargo market is somewhat driven by the carriage of iron ore which is showing a slow recovery after bottoming out in 2012. The group invested in the Singapore office which led to improved performance in the second half of the year and while freight rates have faltered at the start of the new year, the group expect another recovery in the second half of this year. The container market has the most over capacity and due to the young age of the fleet, demand recovery is very slow and chartering rates also remained low but while the market remained poor in chartering, there have been opportunities for sale and purchase as older vessels are decommissioned. The fortunes of container shipping are closely aligned with global GDP levels so should improve in the long term. The group are optimistic that the markets are showing a recovering trend but do not think that the recovery will be strong for the foreseeable future.

As the search for oil and gas continues to grow, the demand for offshore services increases and management are expecting to see this area show growth in the foreseeable future. The offshore sector delivered a strong performance with 20% more transactions being completed compared to last year and a record number of sale and purchase deals were concluded during the year. Revenue from the sales and purchase team overall, which is mostly generated from the sale of second hand tankers and bulk carriers was lower this year than in 2013 though as ship owners concentrated on newer “eco” vessels. The demolition desk had an active year, although the generally improving sentiment in freight markets led to owners delaying plans to scrap older vessels.

The Technical division had an operating profit of £6.8M, an 82% jump on the figure recorded in 2013. The biggest contributor to the operating profit was Braemar Offshore, with Engineering also making a significant contribution and Adjusting reporting an improved performance. Braemar Offshore had a very busy year with good performances from both the marine warranty survey and offshore engineering activities. The increase was due to the higher number of offshore construction projects and rig movements in the Asia Pacific region. Revenue from marine warranty work remained the core driver, contributing more than two thirds of the total. The pace of revenue growth is likely to be slower in the year ahead but the business is apparently now well positioned for long term expansion.

Despite a quiet year for significant incidents in the energy sector, Braemar Adjusting still achieved higher revenues than last year. An uneventful hurricane season affected the performance of the Houston office but the Rio and London offices performed as expected with the new office in Dubai finishing the year strongly after a slow start. Braemar SA recorded an increase in activity and profits despite a reduced level of marine casualties being reported, indicating a growth in market share. The largest increase in the number of cases came through the London insurance market with an increase in local cases won in the Far East also boosting the overall result and higher value work undertaken in America due to more complex cases. The number of staff in this area have been increased in order to handle the greater work load and this year has started well as a result.

Braemar Engineering experienced the most successful year in its history with strong performances from both the UK and the US offices. In the first half of the year, the team from the UK started work on a three year contract for the design and site supervision to build six new LNG carriers. The design and planning stage has now been completed and construction oversight started in March of this year. The Houston office is developing a large range of projects and is involved in a project to develop the world’s largest floating LNG production and export facility as well as developing several potential LNG export and bunkering facilities in the US. Both offices are forecasting a higher level of activity for the next couple of years and have seen a strong start to the current financial year

Logistics profits of £2M were somewhat flat on last year, down by 1%. The underlying trading at all UK ports remained consistent and the group expect to see some improvement in the coming year. They also aim to grow their overseas presence with further hub agency operations. Despite the challenging environment, the number of forwarding jobs increased during the year, although the container consolidation element of the business fell by 21% mainly due to economic weakness in Spain. The liner business provided support for broadly the same number of calls as last year. A new Reefer department was established to target the perishables logistics segment which should take effect this year.

Environmental profits collapsed from £2.7M to just £100K this year. The work on the Rena was successfully completed in February 2013 and without a replacement project, the division’s activity returned to a more routine level. Revenue from the UK operations remained at the same level as the previous year with work including tank cleaning and waste reduction measures, as well as ad hoc incident responses. There was also flood prevention work available during the heavy rains in the UK and the overseas consultancy continued to grow in West and Central Africa.

It was announced that non-executive director John Denholm will step down after 12 years in the job.

Pre-tax profit has now fallen for the third consecutive year. The final dividend remained unchanged over last year and the yield currently stands at 5.2%, which is clearly a very decent return. It must be stated, however, that this payment is not fully covered by cash generated from operations. At the current share price the P/E ratio stands at a rather demanding 24.3 but when the sold Casbarian business is taken out of the equation, this falls to a more fairly valued 16.3. If one scratches the surface the results are better than they initially appear. If the Rena business and Casbarian are discounted, profits were up, driven by a very strong Technical division performance. Net assets would have increased had the exchange rates stayed the same and although the poor cash flow is a concern, it seems mainly due to the higher proportion of work in the technical division and a pick up of orders in the final quarter. There does, however, seem to be no let up in the problems facing the shipbroking industry, which makes the acquisition of ACM (more on that later) a little surprising and the Technical division is not going to make the same gains that it has done this time. I am happy to bank the dividend for now, though, and see how the acquisition progresses.

On the same date that the group released their results, they also announced the proposed acquisition of ACM Shipping Group, a publically listed shipbroking company. Under the scheme, ACM shareholders will receive two new shares and 250p in cash for each share they own which will result in former ACM shareholders owning 28% of the enlarged group. This merger values ACM at £55M, a 6.8% premium to the closing price on the announcement date. ACM is predominantly a shipbroking business and it is hoped that the acquisition will strengthen Braemar’s core shipbroking business and enable to strengthen its service through better market coverage.

It is estimated that Braemar will pay £10.4M in cash for the acquisition to be funded by cash reserves and a new loan facility. ACM reported a turnover of £24.1M and a pre-tax profit of £3.1M, not including amortisation and impairment of intangibles and net assets of £8.3M in 2013. Following the merger the board will include the current chairman, ceo and finance director of Braemar in those positions of the englarged group with the executive chairman becoming an executive director and the non-execs being taken from the board of both groups

On the 4th July the group released an interim statement covering the first three months of the year. Shipbroking performance was slightly ahead of the same period of last year and the division has experienced an improvement in the total forward order book with the Offshore and Sale & Purchase departments performing particularly well. There was a significantly improved performance from the Dry Cargo department but weaker freight rates have affected the income for the Tanker department.

In Technical, Braemar Adjusting and SA both started the year well and Engineering has continued to work on a number of LNG projects with the site supervision work on the construction of six LNG carriers commencing on schedule. Braemar Offshore remained busy across all offices in the Far East and is pursuing new projects to replace the high levels delivered last year. In Logistics, the group focused on growing market share in the UK and Singapore and announced a new office in Houston – no indication of current trading levels though. The Environmental division continued its routine levels of business with now new significant project work. Overall then, the expectations for the year remain unchanged and I remain a holder.