Communisis is a provider of personalised customer communication services. These communications are typically of a marketing, operational or regulatory nature and can be distributed either on paper or in digital formats, through e-mail, text message, mobile content, social media or as in-store marketing collateral. Many of these services are business critical and of operational necessity for clients which provides a degree of stability of revenue streams irrespective of macro-economic and other market conditions.

The group has three operational segments. The design segment services brand strategies by utilising creative, data analytic, and digital marketing skills to devise and implement marketing campaigns that engage customers, so it is a marketing business then. The produce segment services are mostly provided under multi-year contracts and comprise the specialist, high volume and predominantly personalised printing of outgoing customer communications of an operational nature such as direct mail, invoices, statements and chequebook, the processing of incoming customer correspondence and the production of shareholder mailings such as AGM notices and dividend cheques. The deploy segment services provide brand deployment support through the management of third party supply chains for the sourcing and distributing of in-store marketing collateral, mainly in overseas market.

Pass through revenue represents the pre-agreed or contracted revenues representing charges for print, postal and other marketing materials which are passed onto clients at cost as part of a wider service. Postal charges are recognised on despatch to the postal carrier, and print and other marketing material charges are recognised on despatch by the supplier.

The group has a traditional strength in the financial services sector but has been diversifying the client base in recent years. Clients include all the major UK banks, the top ten building societies, major telecoms and media groups, utilities, global consumer goods distributers, high street retailers and supermarkets, government departments and charities. The financial services market accounts for nearly half of all revenues but the consumer goods market is the one that is growing the most, up to just under a quarter. Communisis has now released its final results for the year ended 2014.

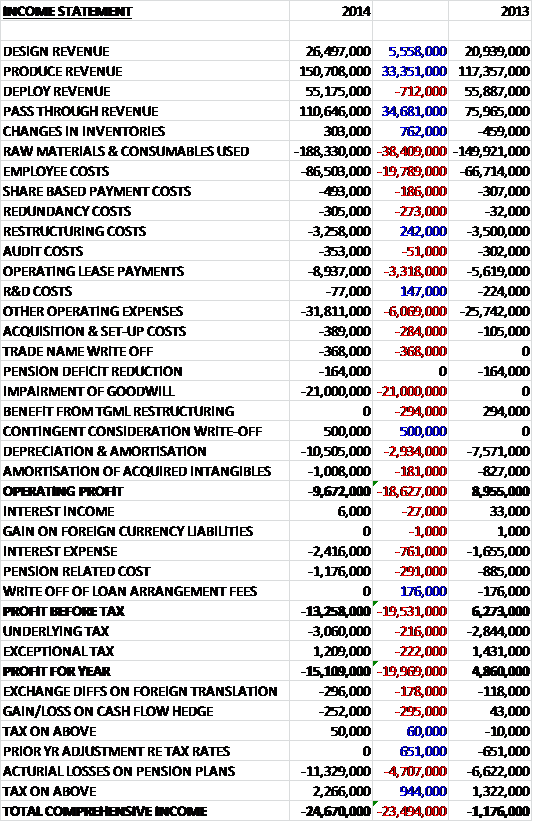

Overall revenues increased when compared to last year as a £712K decline in Deploy revenues was more than offset by a £34.7M increase in pass through revenue, a £33.4M growth in Produce revenue and a £5.6M increase in Design revenue. Raw materials cost £38.4M more than last year and employee costs were £19.8M above last year. We also see a £3.3M increase in operating lease costs, a £2.9M growth in depreciation and amortisation, and a £6.1M growth in other operating costs. The operating profit was adversely affected by a £21M impairment of goodwill this year, however, which meant that it was £18.6M below that of 2013. We then see an increase in interest costs and a small growth in taxes so that the loss for the year came in at £15.1M, an adverse movement of £20M year on year. Clearly if it were not for the goodwill impairment, however, then the profit would be ahead of last year.

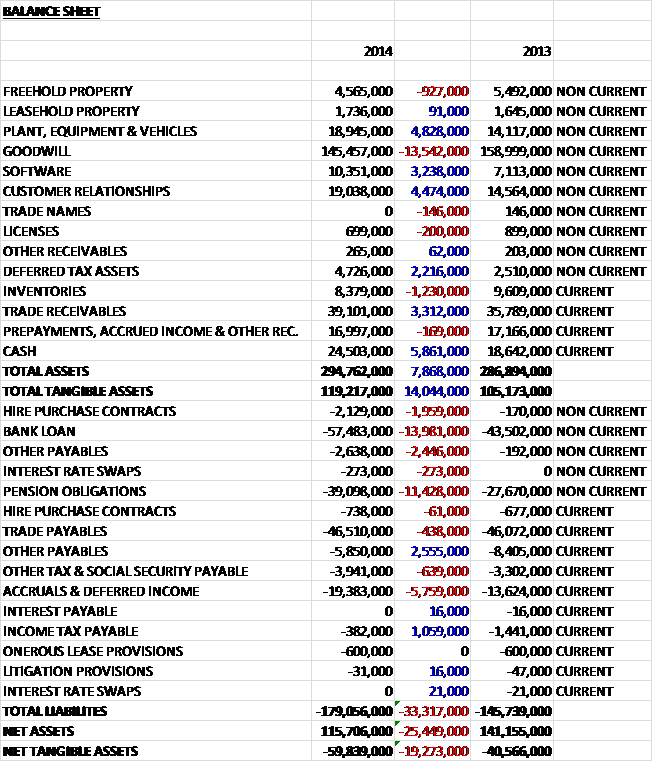

When compared to the end point of last year, total assets increased by £7.9M driven by a £5.9M growth in cash levels, a £4.8M increase in plant and equipment, a £4.5M growth in customer relationships, a £3.3M increase in trade receivables and a £3.2M increase in the value of software. Total liabilities also increased due to a £14M growth in bank loans, an £11.4M increase in pension obligations and a £5.8M growth in accruals and deferred income. The end result is a net tangible asset level of -£59.8M, a deterioration of £19.3M which doesn’t look all that good to me.

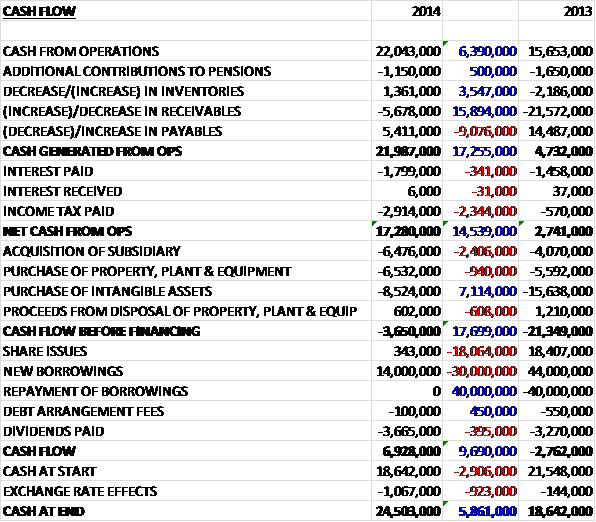

Before movements in working capital, cash profits increased by £6.4M to £22M. There was a broadly neutral working capital situation this year compared to the large outflow last year driven by a huge increase in receivables so, despite an increase in interest and tax, the net cash from operations, at £17.3M, was £14.5M greater than last year. This was enough to cover the purchase of fixed assets and intangibles but not the acquisitions so that before financing there was a cash outflow of £3.7M. After dividends were paid out and the group took out new borrowings of £14M to give a cash flow of £6.9M for the year and a cash level of £24.5M at the year-end.

Most of the contracts for the “Produce” segment are for outgoing communications from the group’s clients to their customers but the range of services was extended early in the year with the acquisition of imaging and mail processing capabilities for incoming customer communications under an outsourcing contract with Lloyds. The most recent new contract award, in February, was a six year commitment from AXA for both incoming and outgoing marketing and operational customer communication services for all its UK brands including Sun Life, Wealth, Insurance and PPP Healthcare.

The UK economy continued to recover during the year, providing a boost to business confidence and marketing budgets. Ongoing cost and profitability pressures, especially in the financial services sector, stimulated further outsourcing of customer communications activities leading to new business opportunities. These beneficial effects are offset to some extent by economic weakness in the Eurozone and social unrest in other parts of the world. There is an underlying erosion in some of the group’s more mature markets, such as those for chequebooks, but margins are maintained through tiered pricing mechanisms and adjustment to the cost base. The progressive shift from paper to digital communications is an important trend and the group is adapting its business model accordingly.

The deploy segment had a decent year with a contract extension from P&G until the end of 2019 whilst revenues from its brand deployment services grew significantly, both through an extended network of European offices and from the addition of new consumer goods clients in the drinks, healthcare and technology sectors.

The underlying operating profit in the design segment was £2.8M (actual profit £2.2M), a reduction of £400K year on year. Turnover increased considerably mainly due to revenues from acquisitions offset by a substantial reduction in data sales which resulted from a continuing decline in demand for prospect lists from the insurance sector that has been the group’s historical focus for their data activities. The loss of contribution from the data sales together with the costs associated with a reorganisation of the business and refocusing its activities on data analytics has led to the reduction seen in operating profit.

The underlying operating profit in the produce segment was £18.5M (actual loss £5.3M including the £21M goodwill impairment), an increase of £1.9M when compared to last year. The two new Lloyds contracts accounted for most of the growth seen in turnover offset by an 8% reduction in demand for transactional documents and higher margin chequebooks due to the ongoing migration from print to digital formats and the changing pattern of payment methods. While the additional turnover contributed to higher adjusted operating profit, non-recurring costs incurred during the transition phases of new contracts together with a loss of contribution from changes in product mix resulted in lower overall margin.

The underlying operating profit in the deploy segment was £13.8M (actual profit was the same), a growth of £4.2M when compared to 2013. The small decline in turnover was the net effect of a 13% increase in managed fee income, linked to the international expansion of brand deployment services for P&G and a 14% decrease in other revenue following a strategic decision to withdraw from or outsource low margin commodity print management services. These same factors generated the increase in adjusted operating profits.

The group is rather dependent on a small number of large clients with one accounting for 22% of total revenues and one accounting for 15% and the top five clients accounting for about 62%.

One major contract extension during the year was with Lloyds Banking. In February the group was awarded a further new outsourcing arrangement with the bank for the imaging and processing of incoming mail from customers. The arrangement is for an initial ten year term with a five year renewal option. It involves an investment of about £7.5M in working capital and mobilisation costs, about £3.2M of which was paid during the year with the rest falling due over the next two years. Under the arrangement the group is handling more than 30 million incoming customer documents for all of Lloyd’s brands. Documents are scanned and digitised with the content being indexed for archiving and onward distribution by the bank. The group are also responsible for the design and creation of operational customer facing documents.

The arrangement brought a new service line to the group and resulted in the acquisition of fourteen existing Lloyds sites with the main operational centres being in Edinburgh, Leeds and Andover. This outsourcing contract followed a similar award in the previous year for Lloyd’s ongoing customer communications. Combining the outsourcing of both incoming and outgoing communications provides the group with a significantly expanded client relationship and substantial new capabilities and growth opportunities.

In February 2015 the group was awarded a new six year contract with AXA for the provision of incoming and outgoing marketing and operational customer communication services including creative, print, digital and postal distribution and document management services. Under the outsourcing arrangements, the group will assume responsibility for a number of AXA’s existing UK inbound and print centres.

During the year the group made a substantial commitment to the development of a second transactional centre within Lloyd’s facility at Copley to allow the transfer of production from, and the closure of, the other Lloyd’s transactional site at Crawley. Net capital expenditure during the year has consequently been higher than normal at £14.2M of which £9.2M relates to Copley including £3M of capital equipment purchased from Lloyds. Additional expenditure of £1.4M to complete the facility will be incurred next year and two HP T400 and one T300 high speed colour digital platforms were also commissioned as part of this investment, all under operating leases.

There have been a number of technological developments that have taken place during the year which have included production automation to enable value to be driven from the HP technology investments; the replacement of legacy systems to improve productivity and support overseas growth; multi-channel document management, supporting client needs to provide a seamless customer experience; and analytics and decision making tools that increase clients’ return on investment and help them target their customers more effectively.

The latest triennial valuation of the pension scheme in March resulted in a reduced deficit at £19.5M and annual deficit reduction payments that have been halved to £1.5M from the previous level of £3M. Despite this, the pension scheme deficit increased to £39.1M this year primarily due to a significant reduction in corporate bond rates.

One major risk to the group relates to the speed of migration from paper to digital communication formats. Each year, the number of paper based communications on existing business tends to fall but overall growth is achieved from new services and market share gains. The group’s services include the composition of the underlying document, the processing of the personalised data that is added to each communication and the distribution of that communication by the most appropriate channel. All of these services continue to be relevant and add value in the digital environment. During the year about 10% of the group’s transactional communications were delivered digitally.

As can be seen there were a large number of non-underlying costs during the year (as there seems to be most years). There were costs of £3.3M incurred in respect of organisational restructuring which included ongoing rationalisation across the group, along with further costs in relation to the closure of the cheque production facility at Trafford Wharf, the integration costs relating to the new design agency, Psona, and recently acquired contracts. The £368K trade name write-off relates to the creation of Psona which has resulted in a name change for Kieon and the Communications Agency to Communisis Digital and Psona (this kind of gives an indication as to what a nonsense some intangible assets are. How can a company give value to a brand name it is acquiring if it is just going to impair it and re-brand it?!). The pension deficit reduction costs relate to legal and consultancy expenses of £164K which were fully paid by the end of the year.

The largest cost related to a £21M goodwill impairment in the produce segment which arose from acquisitions made at the beginning of the last decade. The impairment has arisen to the reductions in demand for some mature product lines. Again, this just supports why I never include goodwill in my calculations. The situation would be better if the asset was amortised as given how old it was, it would probably been fully amortised by now but instead it all gets amortised at once and conveniently discounted.

There were a number of acquisitions during the year. In April the group acquired Jacaranda Productions, a video film specialist creating, managing and measuring the effectiveness of video content for global brands. The consideration paid was £1.7M satisfied by cash of £876K and new shares to the value of £600K. As part of the purchase agreement a contingent consideration has agreed equal to 10% of the annual gross profits of the business which will be payable at the end of the next three years. The contingent consideration is capped at £500K with the fair value estimated at £200K. The acquisition generated goodwill of £994K and contributed profit of £28K since April.

Also in April, the group acquired Public Creative which creates and drives brand awareness with digital media using web and mobile apps. The acquisition cost £379K and generated goodwill of £295K. Since the date of acquisition, the business generated a loss of £12K. In June the group acquired the Communications Agency, an agency that specialises in brand response and CRM across all media channels. The acquisition offers considerable scope for growth and revenue synergies with the group’s existing client portfolio. The consideration payable amounted to £7.8M satisfied by £5.3M in cash and through the issue of 2,404,643 new shares along with deferred consideration of £571K subject to the business generating EBITDA of £888K. The acquisition generated goodwill of £5.6M and contributed profit of £531K during the year.

In August the group acquired the Meaningful Marketing group, a CRM agency with specialist knowledge of the financial services sector. The consideration paid amounted to £647K satisfied with cash of £390K and an amount of up to £625K being payable to the sellers spread over the next five years and equal to 10% of gross profit up to £1.5M and 12.5% of gross profit over this amount. The acquisition generated goodwill of £540K and generated profit of £187K during the year.

After the end of the year, in January the group acquired Life Marketing Consultancy, a research and insight-led shopper marketing agency whose clients are leading consumer goods groups especially in the food, drinks, tech and pharmaceuticals sectors. The acquisition was a big one, on an enterprise value of £22.6M and net assets of just £1.4M. The total consideration was £23.3M with an initial consideration of £14M satisfied by the issue of a two-year bank guaranteed promissory note, £700K in cash and through the issue of £4M in new shares. As part of the acquisition, an amount up to a maximum of £6M will be payable at the end of 2016 if the business generates EBITDA of £3M. The fair value of this consideration has been estimated at £4.6M. There is also another contingent consideration up to £3.3M payable based on the achievement of defined synergies over the next three years and this has been valued at £2.5M. I have to say that I think the group might have over stretched itself with this one – they didn’t have enough headroom in their debt facility and the bank was obviously unwilling to let them borrow more.

The group’s debt currently attracts an interest rate of LIBOR+2.5% to LIBOR+4.25% depending on the ratio of net debt to EBITDA. There is currently only £7M of undrawn facilities so hopefully the group will concentrate on reducing debt and building up their balance sheet in the short term. The group does somewhat hedge against increases in interest rates with a fixed rate of 3.63% paid on one tranche of £10M and 4.15% on another £10M tranche. If interest rates had been 100 basis points higher for the year, pre-tax profits would have been £380K lower.

After an 11% increase in the full year dividend, the shares currently yield 3.7% which seems pretty decent to me. The net debt position at the year-end is £35.9M compared to £25.7M at the end of last year, although this is flattered by seasonal differences and it is refreshing to see the group state the average bank debt as being £41.4M. At the current share price, the shares trade in a PE ratio of 18.8 if we discount the goodwill impairment but this falls to 9.7 on next year’s consensus forecast, no doubt discounting any “non-underlying” costs.

Overall then this has been a bit of a mixed year for the group. There was a loss recorded but this was only due to the goodwill impairment and discounting this, profits did increase year on ear. Operating cash flow also improved and not including the acquisition, there is some free cash flow here but it doesn’t seem to be enough for the group to be able to pay back any of its borrowings. The real problems seem to lie with the balance sheet, however. There is a hefty net tangible liability situation here and it seems to be getting worse.

Operationally the group seems to be operating fairly well. The design division was adversely affected by a fall in demand from insurance companies for lead lists and the produce division is likely to be in a slow structural decline due to less documents being sent by post as many people migrate to digital communications and the phasing out of chequebooks, which is a high margin part of this business. This year, these falls were offset by the large contract started with Lloyds for handling all their ingoing and outgoing mail. The deploy segment seems to be performing well as their contract with P&G gives them a lot more work.

So, with a PE of 9.7 and a dividend yield of 3.7% these shares look rather cheap but when we consider the long term structural decline of the sector, the terrible balance sheet, the large debts and the acquisitions that the group can’t really afford (they seem to be buying market companies, presumably to try and mitigate against the move away from written communications) then I don’t think I can invest in these shares. They may offer some upside to more risk-tolerant investors but its not really for me at the moment.