Dechra Pharmaceuticals has now released its final results for the year ended 2016.

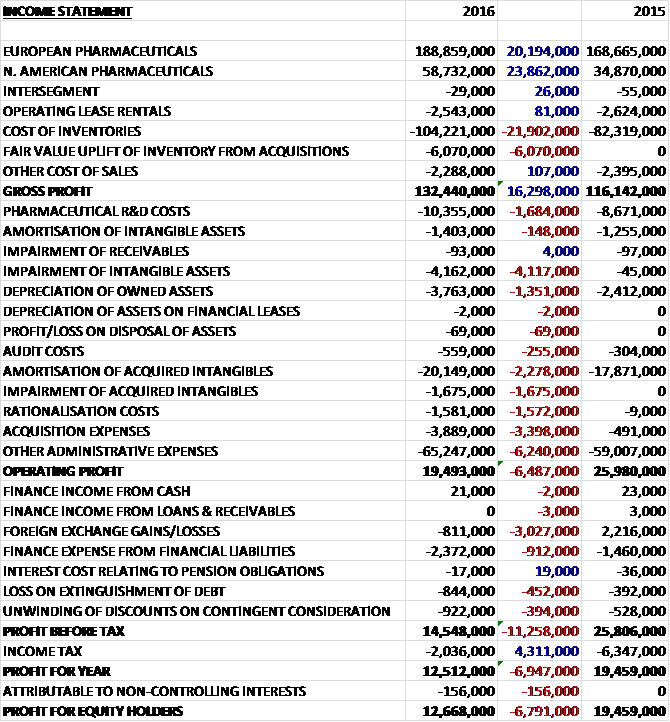

Revenues increased when compared to last year with a £23.9M growth in North American revenue and a £20.2M increase in European revenue. Cost of inventories increased by £21.9M and there was a fair value uplift of inventory from acquisitions which cost £6.1M to give a gross profit £16.3M above that of last year. R&D costs were up £1.7M, depreciation increased by £1.4M and there was a £4.1M increase in intangible asset impairments. We also see a £2.3M growth in the amortisation of acquired intangibles, a £1.7M impairment of acquired intangibles, £1.6M of rationalisation costs, a £3.4M increase in acquisition costs and a £6.2M growth in other admin expenses which meant that the operating profit fell by £6.5M. There was also a £3M negative swing to forex losses, a £912K growth in interest costs, a loss on extinguishment of debt and a £922K unwinding of discounts on contingent consideration, although tax charges declined by £4.3M. This all meant that the profit for the year was £12.7M, a decline of £6.8M year on year.

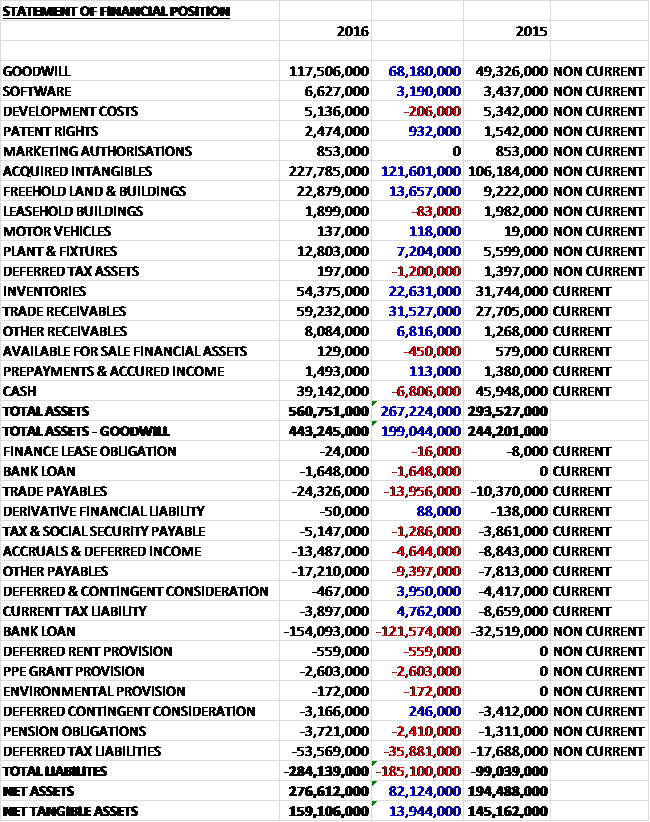

When compared to the end point of last year, total assets increased by £267.2M to £560.8M driven by a £121.6M growth in acquired intangibles, a £68.2M increase in goodwill, a £31.5M growth in trade receivables, a £22.6M increase in inventories and a £13.7M growth in freehold land and buildings. Total liabilities also increased during the year due to a £123M growth in bank loans, a £35.9M increase in deferred tax liabilities relating to an increase in value of intangible assets, and a £14M growth in trade payables. The end result was a net asset level (excluding goodwill) of £159.1M, a growth of £13.9M year on year.

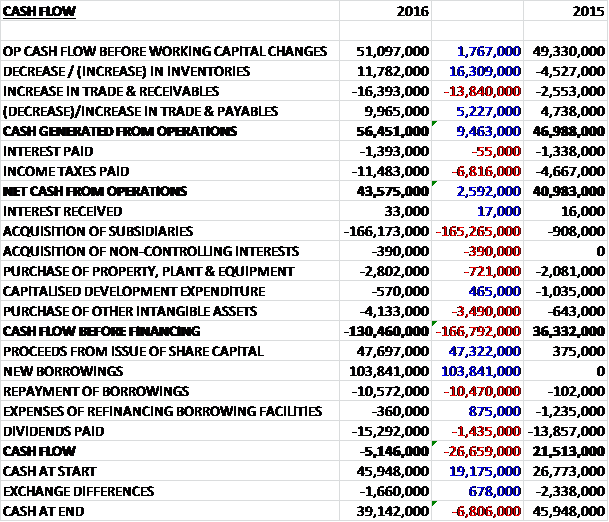

Before movements in working capital, cash profits increased by £1.8M to £51.1M. There was a cash inflow from working cap as an increase in receivables was more than offset by movements in inventories and payables. Tax payments increased by £6.8M to give a net cash from operations of £43.6M, a growth of £2.6M. The group spent £2.8M on property, plant and equipment and £4.7M on intangible assets but the big expenditure was the £166.2M spent on acquisitions to give a cash outflow of £130.5M before financing. The group received £46.7M from the issue of share capital and £103.8M in new borrowing proceeds but spent £10.6M on repaying loans and £15.3M on dividends. The end result was a cash outflow of £5.1M and a cash level of £39.1M at the year-end.

Excluding the losses from acquisitions, like for like profits increased by 5.1% at constant exchange rates but with growth adversely impacted by forex losses of £800K compared to forex gains of £2.2M last year, profits actually declined by 1% at actual exchange rates.

The operating profit in the European Pharmaceuticals division was £51.7M, a growth of £3.7M year on year on like for like revenues that were up 5.7%. The companion animal product sales were driven predominantly by a strong performance in endocrinology, and anaesthetics. Within endocrinology, Vetoryl continues to grow in all major territories and the launch of Zycortal into 14 countries has strengthened their position in that sector. The equine portfolio has also performed well with Osphos being launched across all major territories and performing to expectations. They are also re-positioning Equipalazone following palatability trials.

The recovery in farm animal products that was reported in the first half of the year has continued in the second half. The decline in antibiotic sales in Germany has slowed and after several years of decline in the Netherlands they are now seeing sales flatten. Against this background, overall growth has been achieved by increasing market penetration in Poland and in countries where they had a lower market share historically such as UK, France, Italy and Spain. They have also launched Solamocta, a new antibiotic lifecycle improvement which will be key to the recovery in Germany. Other new product registrations have been received in the division and are being prepared for imminent launch in Europe which should ensure that the positive momentum continues.

Diet sales have not fully returned to previous levels following the supply problems last year. Whilst there was growth in a number of markets, this was offset by the loss of a large corporate account in Scandinavia and palatability issues for some of the cat diet products. They have appointed an experienced manager to focus on developing the business and have recently won two new contracts with major vet groups which should ensure an improved position in the future.

The operating profit in the North America Pharmaceuticals division was £17.5M, an increase of £6.9M when compared to last year on revenues that increased by 37.9% on a like for like basis. The US has driven the majority of this growth as they continue to gain strong market penetration in their key focus areas of dermatology and endocrinology. This growth has been enhanced by a good performance from Phycox, a strong growth and traction with Osphos and the successful launch of Zycortal in March.

The biggest product, Vetoryl capsules, delivered double digit growth as the group has maintained its educational and marketing campaign and introduced a low dose 5mg capsule to increase flexibility on dosing options. The Canadian business delivered a good performance across the portfolio which was enhanced by the launch of Psphos and Zycortal. The business has also benefited from the acquisition and launch of HY-50 in the territory, a product that they have marketed in Europe since its acquisition in 2012.

The primary focus of the management team towards the end of the period was to integrate the commercial team from the recent acquisition of Putney. This enlarged team will give the group improved penetration and more direct contact with US vet practices to enhance sales.

During the year Zycortal, a novel canine endocrine product for the treatment of Addison’s disease, has received approval throughout the EU, US, Canada and Australia. Following the registration of Osphos last year in the US and UK, approval was subsequently received in 17 additional EU countries in September 2015. They have also had numerous successes in the farm animal product portfolio in Europe; two water soluble antibiotics, Solamocta and Phenocillin have been approved in 17 member states; a liquid antibiotic, Metaxol, was approved in 18 member states; and the existing antibiotic aerosol, Cyclospray, was extended into 12 new territories. The new Croatian facility has achieved approval for a poultry vaccine, Avishield ND, to treat Newcastle disease in 12 major European markets and has also achieved a number of other national registrations including Egypt and Ukraine.

In the period the group has terminated an early stage project for canine ophthalmology and a canine cardiology product. They have, however, initiated eight new projects across both markets and development has continued on the Genera vaccines and Putney generics since acquisition with significant filings being made from both businesses.

Geographical expansion is progressing well. In addition to the acquisition of Brovel, which creates a foothold in the Mexican market, the acquisition of Genera provides access to the smaller markets of Croatia, Bosnia, Serbia and Slovenia. A greenfield start-up subsidiary has been established in Austria which started trading in January and sales are progressing well. The subsidiaries in Canada and Poland, established in the prior year, are performing well, with Poland being above expectations.

Last year the group made an investment to upgrade the pre-mix department in Bladel to increase batch sizes and reduce the cost of goods. This department is now fully commissioned and product transfer to the new lines is underway. They have also invested in a new tablet and capsule blister packaging line in Skipton which will increase volumes and speed. This is currently being commissioned and it is anticipated it will be effective from the beginning of the new year. Other initiatives to reduce the cost of goods and improve efficiencies have been implemented, resulting in raw material price reductions, predominantly for the farm animal product division. They have also seen a small reduction in material wastage rates and batch reject rates are lower than the previous year.

Manufacturing volumes have increased overall due to internal sales increasing but like for like external sales have decreased by 4.8% due to reduced volume with some customers. Overall contract manufacturing has increased following the Genera acquisition. Service to customers has increased with on-time delivery ahead of internal targets and the previous year.

In October 2015 the group completed the acquisition of 92.26% of Genera for €36.6M which was funded from existing cash and debt facilities. The transaction generated goodwill of £4.5M. The business reports in the EU pharmaceuticals sector and contributed a £3.2M loss to the results in the period. In May 2016 the group acquired a further 1.13% for £400K which gives them an interest over 93.39% of the business. The acquisition enables the group to enter the fast growing poultry vaccines market. The group have already rationalised the business to improve efficiency and have integrated many of the teams into the global operations.

In January 2016 the group acquired Brovel, a veterinary pharmaceuticals company based in Mexico. They paid £3.3M on completion and a further £591K is contingent upon the business reaching registration milestones for the group’s products in Mexico. The transaction generated goodwill of £2.6M. The business reports under the North American Pharmaceuticals segment and contributed a £100K loss to results during the period. The board believe that this acquisition will help open the significant Mexican animal health market to the group and enable them to register and market their products in the country. Several products have been identified as suitable and the registration process with the authorities has started.

In April 2016 the group acquired Putney Inc, a veterinary pharmaceuticals company based in Maine for £134.2M in cash with the transaction generating £49.3M of goodwill. The business will report in the North American pharmaceuticals sector and contributed a £6.7M loss to results in the period. The acquisition was the most complementary US opportunity they had identified and provides significant scale and access to a strong drug pipeline in the North American market. They currently market eleven approved products and has a further ten generic products in its pipeline which are expected to be launched over the next five years.

There were a number of “non-underlying” items this year. Rationalisation costs of £1.6M relate to the integration and restructuring programmes implemented since the acquisitions of Genera and Putney. The fair value uplift of inventory acquired through business combinations accounted for £6.1M; the impairment of acquired intangibles and associated deferred consideration accounted for £1.7M and includes the impairment of a US generic pharmaceutical product following the acquisition of Putney, as Putney had already developed a similar product. It also includes the impairment of an acquired intangible due to the cessation of sales following a competitor registration in the US.

The roll out of the Oracle ERP system continues to be one of the primary operational objectives of the group. In April the core Oracle solution was implemented into the US business and they are currently targeting a roll out to most sites in 2017 followed by an upgrade to the current manufacturing Oracle system. During the year the group raised £47M from the issue of 4.4M shares in order to help pay for the Putney acquisition.

The current chairman, Michael Redmond, will step down from the board in October at the AGM and his successor will be non-executive director Tony Rice. Chris Richards also stepped down from the board as a non-executive director after nearly six years of service to further other opportunities. Anne-Francoise Nesmes, the CFO, has also resigned from the board. She left the company at the end of July to take up a role as CFO with a FTSE 100 business. Richard Cotton is expected to join the company in January 2017 as CFO.

Going forward, although the board anticipate a degree of uncertainty following Brexit, the business is naturally hedged by its geographical spread and international sourcing. Any significant downturn in the UK economy may impinge on growth rates but they do not anticipate any material effect on the group, although they are potentially susceptible to additional admin burden. Good progress has been made on the integration of the acquisitions. The pipeline has also been strengthened through both new internally generated ideas and the integration of acquired development programmes. The group continues to deliver growth and identify opportunities across all aspects of the strategy and they therefore look to the future with confidence.

At the current share price the shares are trading on a PE ratio of 100.2, mainly due to one-off cots but this reduces to 26.2 on next year’s consensus forecast which is not exactly cheap. After a 9% increase in the dividends, the shares are yielding 1.3% which increases to 1.4% on next year’s forecast. Net debt at the year-end was £116.6M compared to a net cash position of £13.4M at the end of last year and this was not helped by the Sterling depreciation following the Brexit vote due to the debt in Euros and dollars.

On the 9th September the group announced that it received approval from the US FDA for a generic antibiotic. The product is expected to be a first generic market entrant in a substantial antibiotic market and it is the first registration the group has achieved through Putney’s development pipeline since it was acquired.

On the 16th September the group announced that it had agreed terms to acquire Apex Labs, a privately owned vet pharmaceutical business which manufactures, markets and sells branded non-proprietary prescription and other related companion animal products in Australia and New Zealand. The acquisition will provide the group with direct access to the established and growing Australian companion animal product market, which they currently operate through partners. Last year the business made an operating profit of £3M. The total consideration is £31.3M which will be funded from existing debt resources. It is expected to be earnings enhancing in the first year.

Overall then this has been a year of progress that has rather obscured the underlying performance of the group. Profits declined as the numerous acquisitions took their toll, with like for like profits up at constant currency but down at actual exchange rates. Net assets increased, as did operating cash flow, although all the cash was used on acquisitions, leaving a big cash outflow before financing.

The European business performed fairly well, with the companion animal side showing growth from Vetoryl, Zycortal and Osphos, while it is encouraging to see the farm animal side halting the decline seen in previous years, in part as a result of increased penetration in to Poland. The diets side of the business still seems to be struggling, however. In North America, the business seemed to grow strongly but this year has been defined by acquisitions, with Putney and Apex Labs being particularly sizeable. I am starting to get a bit concerned that the group has gone a bit “acquisition-happy” and would prefer they bedded in the ones already completed before doing more.

They also seem to be getting more exposed to high debt levels so would really like to see this brought down a bit too. On top of this, the forward PE of 26.2 and yield of 1.4% makes the shares look expensive and prone to any issues. Despite this, I am continuing to hold for the time being.

On the 21st October the group released a trading update covering Q1 where performance was in line with management expectations with all of the recent acquisitions performing well. In September they announced that their generic antibiotic, Amoxiclav, had received approval from the US FDA. This registration is for two of four different dosage strengths of tablets and the remaining two are in the final stage of registration with approval expected before the end of 2016. This is the most significant product within the recently acquired Putney pipeline.

The £31.3M acquisition of Apex Labs was completed in October which provides access to the Australian market with a wide range of companion animal products and includes a new manufacturing facility and development pipeline. The group have three products registered in Australia which will also be sold through this business once approved. It was also announced that the Chairman of 14 years, Michael Redmond retired to be replaced with Tony Rice.

Not much to note really, things are going as they were it seems.

On the 5th December the group announced that director Tony Rice purchased 20,000 shares at a value of £250K which seems a fairly substantial investment.

On the 17th January the group released an update covering the first half of the year. Reported group revenue increased by about 34% at constant exchange rates (56% at actual exchange rates) and excluding the benefit of the acquisitions, it was 7% at constant currency and 22% at actual rates.

The European pharmaceuticals segment increased total reported revenues by 12% at constant rates. This was driven by contributions from both the Genera and Apex acquisitions and from a strong companion animal and equine performance.

Diet sales returned to modest growth in the period following two years of decline as they changed manufacturer and resubmitted the range. Revenue from food animal producing products also showed limited growth in the period which was constrained by the planned reduced production in the injectable antibiotics suite which was undergoing modifications.

Total reported North American segment revenue increased by about 112% at constant currency. The US business growth includes an uplift in sales from the stocking of the North American distribution chain with products from the acquired Putney business. Sales of Putney products have also benefited after the integration from sales and marketing efforts of the enlarged Dechra team. Both the companion animal and equine portfolios performed well during the period.

The group received FDA approval for their generic antibiotic Amoxi-clav during the period which was the first major approval from the Putney pipeline following the acquisition. Pipeline delivery continued with the approval of Altidox, a new FAP generic water soluble antibiotic, in 13 EU territories. Osphos, the equine lameness product, received approvals in Canada and Australia. Successful registrations were also gained from the Genera pipeline including Genoxytab, a FAP uterine antibiotic, in four EU territories, and Canihelmin, a CAP dewormer, in six EU territories. Apex labs received Australian approval for a liquid formulation of benazepril, a CAP cardiac medication.

This all seems fine to me and I continue to hold.