InternetQ is engaged in the trading and development of software and related products and services used in wireless and telecoms. It has been listed on the AIM exchange for four years now and has now released its final results for the year ended 2014.

Revenues mainly consist of telecoms traffic that is generated from the end users/subscribers and are based on the activity and flow of premium rate telephone minutes and SMS messages. The group also gains revenue from the supply of mobile phone content, entertainment and other services and acts as an intermediate to network operators for branded mobile campaigns.

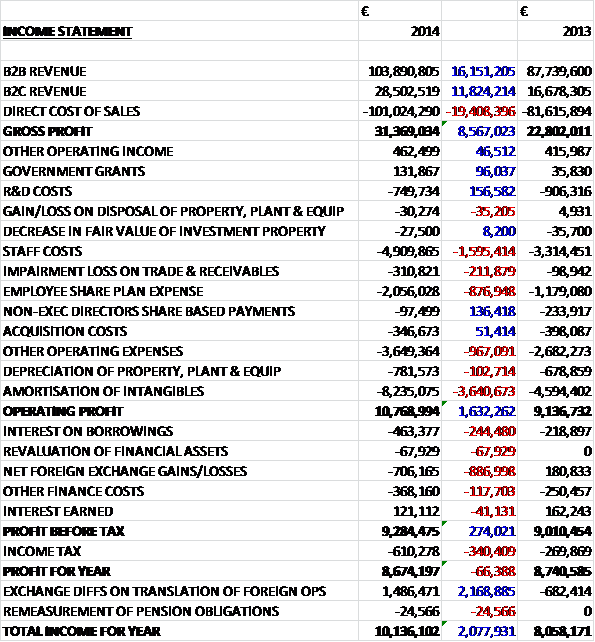

Revenues increased year on year with a €16.2M growth in B2B revenue and a €11.8M increase in B2C revenue. Cost of sales also increased to give a gross profit some €8.6M ahead of last year. We then see a modest fall in R&D expenditure more than offset by a €1.6M increase in staff costs, an €877K increase in staff share plan expenses, a €212K growth in receivables impairments, a €3.6M increase in amortisation charges and a €967K growth in other operating costs to give an operating profit £1.6M higher than in 2013. There was also an €887K detrimental movement in foreign exchange representing the unrealised foreign exchange losses on inter-company loans between the holding company and various subsidiaries, and an increase in interest which, when combined with a €340K growth in the tax bill (mainly as a result in the reduction of capital allowances for tax incentive plans), meant that the profit for the year, at €8.7M was actually €66K below that of last year.

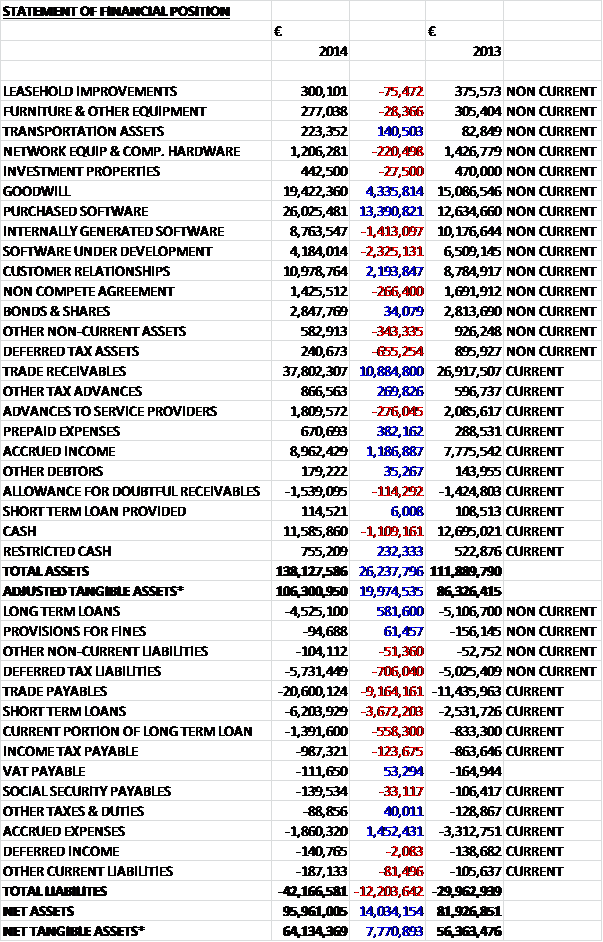

When compared to the end point of last year, total assets increased by €26.2M driven by a €13.4M increase in purchased software, a €10.9M growth in trade receivables, a €4.3M increase in goodwill and a €2.2M growth in the value of customer relationships partly offset by a €2.3M decline in software under development and a €1.4M fall in the value of internally generated software. For the tangible asset calculation, I have decided that given the nature of the group’s business the software is probably worth something so the “tangible” asset level in this case also includes the software. Liabilities also increased during the year as a €9.2M growth in trade payables and a €3.7M growth in short-term loans was partially offset by €1.5M fall in accrued expenses to give a net tangible asset level of €64.1M, an increase of €7.8M year on year. There are also outstanding operating leases off the balance sheet totalling €1.3M which does not seem particularly material.

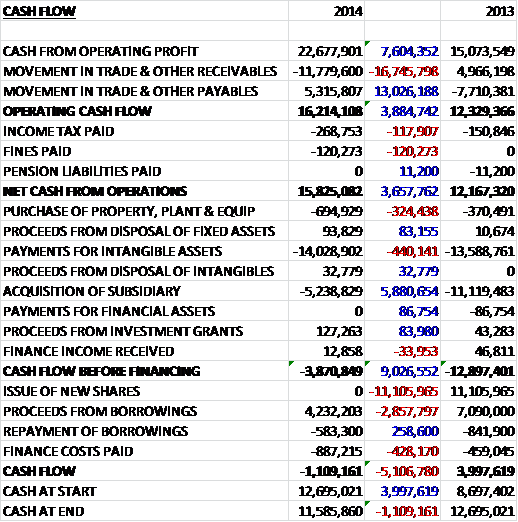

Before movements in working capital, cash profits increased by €7.6M to €22.7M which was eroded somewhat by a large increase in receivables and after the Polish fines and tax was paid, the net cash from operations came out at €15.8M, an increase of €3.7M year on year. This was only just enough to cover capital expenditure, with a €14M spend on software relating mainly to the development of Minimob platform, Akazoo music platform and BADABEE mobile portal, and a €695K spent on fixed assets but the €5.2M acquisition meant that before financing there was a €3.9M cash outflow. After new borrowings were received the cash outflow for the year stood at €1.1M to give a cash level of €11.6M which is fine but at some point this company is going to have to start generating free cash flow if it is going to sustain itself without the help of increased borrowings and share placings (as occurred last year).

The operating profit at the Business to Business sector was €13.2M, an increase of €3.3M year on year. Mobile marketing has evolved in recent years and mobile is expected to be the biggest driver of global advertising growth. The group has gained traction across their key geographies during the year with several new clients and contract wins such as Moviestar in Spain and Latin America, Viva in the Dominican Republic and CellC in South Africa which is part of a growing pipeline for mobile network operators’ campaigns that have been integrated with Minimob. The acquisition of UP Mobile also makes the group an important player in the large Mexican market.

The operating loss at the Business to Customer sector was €2.5M, a €1.6M deterioration when compared to last year. Some major contracts with MNOs have helped to drive international expansion with key partnerships with Sony Mobile and Orange Poland secured during the year. The increase in revenues over the year was largely driven by a focus on improving the competitive proposition of Akazoo’s music streaming service with new features being added. The biggest geographic growth was seen in Asia and Europe with multiple new contracts secured in the Asian market including a pilot launch in Thailand, a successful launch with Ninetechnology and the OEM brand partner of Gmobi in Malaysia, the launch of the Blackberry messenger partnership in Indonesia and the launch of a co-marketing initiative with device manufacturer Smartfren Indonesia to promote an add-on service offering.

The group also strengthened Akazoo’s position in Europe through the launch of a bundle agreement with Orange in Poland and the release of a co-branded add-on service offering with MTN in Cyprus. There is good visibility going into 2015, with a strong pipeline of launches and partnerships with leading MNOs, Internet Service Providers and device manufacturers in Indonesia, Singapore and other markets. They also plan to launch Akazoo in another Western European market in the coming months.

The group has a number of software assets. Minimob provides a full suite of messaging and smart ad delivery tools enabling automated alerts, rich media messaging and subscriptions. The technology platform helps app developers maximise the success of their apps, allowing them to build a communication strategy that will bring people back to the apps day after day. For maximising the advertising revenue, the group developed tools and services for precisely targeting the delivery of advertising to the right audience. During the year they invested in phase 5 of the software development as well as the addition of an add delivery end point and total development costs for the year amounted to €7.6M while €2.6M is included as software under development.

In the latest phase the following features have been developed: ad formats – advertisers can choose to deliver their offers in several formats, selecting each time the one that is going to maximise message efficiency and conversion rates; account balance, including reports on daily earnings, payouts and payment methods; and monetisation, developers who open their applications to third-party advertising can earn money depending on app distribution and traffic. At the same time a new form of global advertising demand has emerged, focusing on driving mobile consumers to take action in response to a well-timed offer or a call to action which can be a message, advert or video. In response to this trend, the group is developing the add delivery end point phase of the platform that includes video ad packages, in page video adds and HTML5 adds.

Akazoo is the group’s digital/mobile music social steaming platform, optimised for online and mobile access. At the core of the package lies a music store capable of concurrently serving content with metadata aggregation to millions of users. The music store module is able to use external content delivery networks supporting both http progressive downloads and adaptive media streaming for content distribution to users through all widely accepted channels in multiple music formats and bit rates. The Akamai HD network which is utilised by Akazoo is a live and on demand streaming technology platform that can support the largest online events. The total development costs on the platform during the year were €5.2M with €200K included in software under development.

New features this year included a global content reporting platform, a third party data aggregation platform and A/B engagement metrics analytics. Subsequently the mobile digital streaming radio solution where the Akazoo radio app supports a wide range of radio stations which are constantly being enhanced has been developed.

Badabee is a messaging application for android that allows customers to send SMS to any mobile number via the application interface. This is a subscription based service running in various countries under a daily or weekly model. This year, development costs on this platform totalled €600K in order to update the previous version where the new version offers various methods to send and receive SMS.

The mobile gaming market is becoming a more important focus for the group and Minimob now delivers a significant number of campaigns including games such as Tribal Wars, Puzzle Coin Hunter, Brave Frontier and Dragon Nets. The group’s role has always been to convert a mobile customer into a paying customer but they are now being rewarded with a specific payment by a third party for encouraging a mobile consumer to effect a transaction, be it making an app download or signing up for subscription services. This additional revenue, whether it comes direct from brand names like BBM and WeChat or from third party demand side ad networks and agencies working for major clients, is a line of business that will feature more prominently in 2015.

During the year non-executive director Michael Joliffe announced his retirement. The group is still 46% owned by the CEO and founder Panagiotis Dimitropoulos but also has some heavy weight institutional investors such as Legal & General, Schroder and Standard Life. None of the other directors seem to have significant share holdings, though.

The group seems very reliant on a small number of customers. Three clients with whom the group conducts campaigns in the Middle East, Africa and Russia account for an astonishing 77% of the B2B sector revenues (accounting for the same percentage last year) and two customers accounted for 30% of the total revenues in the B2C sector. There is also some exposure to foreign currency exchange between Sterling and Polish Zloty and Singapore Dollar with a 1% change affecting profits by €137K. Also, given the geographic reach of the group there are some country risks to look out for. Specifically the adverse economic conditions in Greece and Cyprus could affect revenues but with just €2.9M of sales being generated in Greece the risk is not that material and perhaps Russia would be more of a risk given the statement above.

The group has been imposed two fines from Polish regulators amounting to €196K. The first fine of €120K was paid during the year with the rest to be paid shortly. They have also received a number of civil court claims regarding certain mobile marketing campaigns in Poland with some €37K outstanding. In addition, they have received four payment orders from third parties for the total of €165K. No further details are given and whilst these are relatively modest amounts, it is rather concerning to see so many outstanding legal issues which might point towards some dubious practices.

In May the group acquired Up Mobile Holdings, a mobile marketing and interactive TV and radio content provider in Mexico. It is the number one provider of interactive solutions for radio stations and also provides mobile solutions to media organisations and the public sector in Mexico. The key benefits of the acquisition are that it significantly increases the group’s presence in Latin America, it provides an entry into Mexico’s dynamic market and builds increased value by capitalising on the synergies of both company’s clients and services. The total consideration paid is €6.7M and the acquisition generated €4.5M of goodwill and comes with €3.3M of customer relationships so there is a negative net tangible asset level. Initially €3.2M will be paid in cash with a contingent consideration of shares to be issued to a value of €3.5M.

In the seven months since acquisition, the company made a loss of €35K on revenues of €895K. Had the acquisition occurred at the start of the year, Up Mobile would have contributed a loss of €411K. I am sure management know what they are doing with this acquisition but it seems to me that it needs quite a lot of work in order to get it contributing to profits.

Going forward, the group has made a solid start to 2015 and the board is confident of delivering further growth during the year. The increase in mobile advertising and the massive uplift in installed apps are significant drivers for growth.

At the current share price the shares trade on a PE ratio of 16.9 which comes down considerably to 9.5 on Cannaccord’s next year forecast. The group was in a net cash position of €220K at the year-end compared to €4.7M at the end of last year. The current focus is on growing the group so it is not considered appropriate to pay a dividend at this time.

Overall then, this is an interesting company and one I am finding quite hard to value. Profits were broadly flat year on year but were not helped by adverse forex movements. Net tangible assets seem pretty good if we include software and improved year on year but the big increase in receivables could be something to watch as despite the improvement in operating cash flow the group does not produce much free cash and any that is produces is used to go towards further acquisitions. On that subject, I am not sure if the latest acquisition is of a great quality despite the large potential market – it is market leader in Mexico and unable to make a profit!

The B2B business is basically Minimob and this seems to be decently profitable but the B2C business which is Akazoo, a music streaming service, just absorbs investment and I am not sure the group will be able to actually make any money from it. One real stand-out risk is the reliance on three main customers who are located in some rather dicey markets – Russia, the Middle East and Africa to be precise. As I said, this is a difficult one. The product (at least, Minimob) seems to be quite exciting but there are quite some risks with the company – could be an interesting educated punt but not something I am going to put too much money in.

On the 21st May the group released a trading update covering Q1. The group achieved growth across both mobile marketing and digital entertainment divisions with revenues up 11% to €33.5 and EBITDA (there is a very hefty Amortisation charge to come out of this) up 28% to €6.2M with profit margins higher than expected. In the mobile marketing division the group completed a campaign through Minimob with Foodpanda, an Indian Rocket Internet company which provides entry into ten new geographies; ad agencies accounted for the majority of new campaigns (over 70%, followed by brands and operators; ten new marketing campaigns were started in Latin America, including Claro Chile and Vodacom Lesotho (that sounds like Africa to me…), mobile entertainment subscription services were started in South Africa; and a major new marketing campaign was signed with Andalabs in Indonesia.

In the digital entertainment sector there was a renewal of campaigns with key clients, including Sony Mobile in Malaysia; the Akazoo service was launched with Smartfren Indonesia; and the Akazoo radio streaming platform was developed with a new release on the Akazoo Business Intelligence platform. Apparently going forward there is good visibility with a strong pipeline for both businesses, particularly in Asia and Latin America.

On the 9th July the group announced a strategic investment into Akazoo by a consortium led by Toscafund Asset Management and Penta Capital. Tosca is investing about €17M in cash into the UK registered entity that will hold the Akazoo business. Also, the shareholders of R&R Music (a company that combines algorithms and behavioural science expertise with social media and human curation to create a profiling and recommendation engine) have agreed to contribute their business to the new Akazoo group. The cash investment will be used to grow Akazoo’s operations and expand the new entity’s proposition across new verticals.

Based on the terms of the new investment, the valuation of the enlarged Akazoo business is about €104M with InternetQ holding just over 69% of the shares with Tosca and R&R Music’s shareholders owning the rest. In all, this sounds like a good development for the group. They were clearly struggling to get Akazoo profitable and this should really help in that goal whilst also enabling InternetQ to retain an interest whilst concentrating on the Minimob platform.

On the 28th July the group released a trading update for H1 2015. Overall it was a solid first half with increased revenue and EBITDA on last year driven by growth in performance based ad campaigns. The group had growth across both business divisions during the period, revenue increased to €72M, up 10% year on year, mainly fuelled by growth at Minimob, replacing the legacy Mobi Dialogue business which has much lower margins. Adjusted EBITDA increased by 35% to over €13M reflecting higher margins in Minimob and maturity of the Akazoo model. The company has a strong pipeline with good visibility for the coming half year and is on track for even better growth in the historically stronger second half and they are confident that full year results will be in line with market expectations.

In Mobile Marketing there was increased traction for Minimob with new contracts secured with global brands, including Delivery Hero, a food ordering service; Lazada, SE Asia’s leading online shopping platform; and Bravofly, a flight search engine. In all, there were 15,000 new performance-based ad campaigns that were run through Minomob and there were also successful marketing campaigns with leading operator Claro in Paraguay, CellC in South Africa and Zain in Bahrain. In the Digital Entertainment division, the integration of Akazoo and R&R’s operations is already underway and there was strong traction and performance of the product in SE Asia with the growth rate in regional subscriber count exceeding 20%. This all sounds pretty positive to be honest.

It is quite difficult to take anything from this chart, the down trend since March could still be in play or the uptrend since July – who knows?!