IQE has now released their interim results for the year ending 2018.

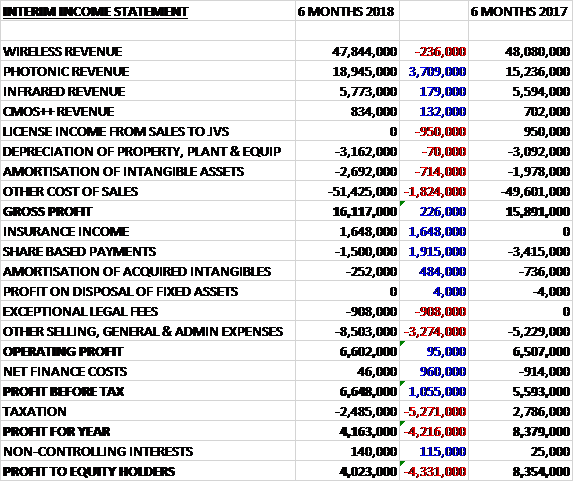

Revenues increased when compared to the first half of last year as a £236K reduction in wireless revenue was more than offset by a £3.7M growth in photonic revenue, a £179K increase in IR revenue and a £132K growth in CMOS++ revenue. License income from sales to joint ventures fell by £950K, however. Amortisation costs were up £714K and other cost of sales increased by £1.9M to give a gross profit £226K higher. The group received £1.6M in insurance income, share based payments fell by £1.9M and amortisation of admin expenses declined by £484K. Offsetting this was a £908K legal fee and a £3.3M increase in other general costs which meant that the operating profit was £95K higher. There was a £960K swing to a finance income but tax charges increased by £5.3M which gave a profit for the period of £4M, a decline of £4.3M year on year.

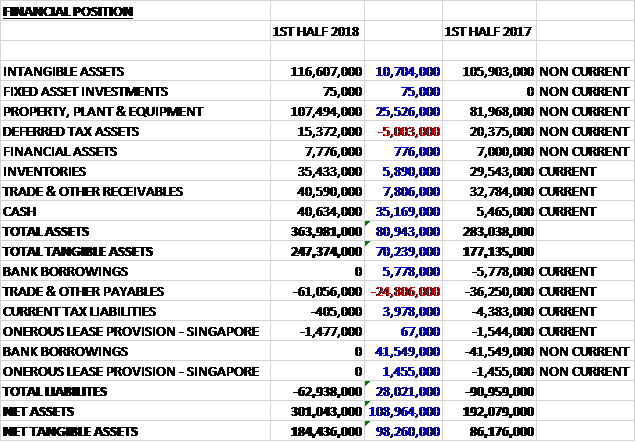

When compared to the end point of last year, total assets increased by £80.9M driven by a £25.5M growth in property, plant and equipment, a £35.2M increase in cash, a £10.7M growth in intangible assets, a £7.8M increase in receivables and a £5.9M growth in inventories, partially offset by a £5M decrease in deferred tax assets. Total liabilities declined during the period as a £24.8M growth in payables was more than offset by a £47.3M decline in bank borrowings and a £4M decrease in current tax liabilities. The end result was a net tangible asset level of £184.4M, a growth of £98.3M over the past six months.

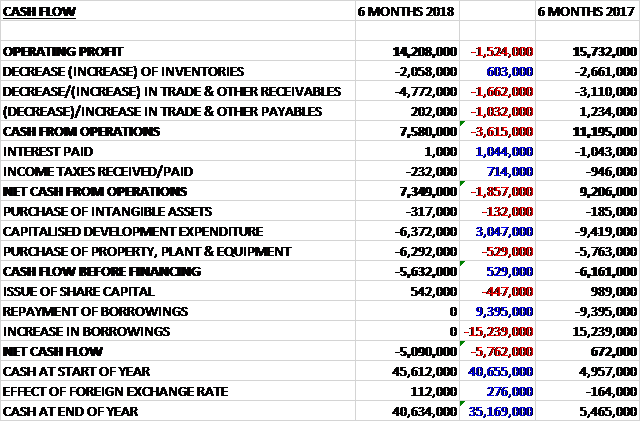

Before movements in working capital, cash profits declined by £1.5M to £14.2M. There was a cash outflow from working capital but interest payments fell by £1M and tax payments were down £714K to give a net cash from operations of £7.3M, a decline of £1.9M year on year. The group spent £6.4M on development expenditure, £6.3M on property, plant and equipment and £317K on other intangible assets to give a cash outflow of £5.6M before financing. The group brought in £542K from the issue of share capital to give a cash outflow of £5.1M and a cash level of £40.6M at the period-end.

Currency headwinds, accelerated customer qualification programmes and Newport foundry pre-production costs resulted in a drag on profits of around £3.5M.

The operating profit in the wireless business was £6.6M, a decline of £876K year on year. Inventory channels, depleted as a consequence of the rapid ramp of VCSELs in H2 2017 were partially replenished during the period and photonics capacity was directed to satisfy more than twenty VCSEL chip manufacturer engagements. Operating margins reduced as a consequence of reactor conversion costs related to switching reactors from photonics to wireless production.

Despite slower growth in smartphone sales in recent years the increase in data traffic continues to drive the need for more sophisticated wireless chip solutions in handsets. The group sees the roll out of 5G infrastructure as a significant upside potential. Current infrastructure applications such as base stations, radar and CATB are a small but fast growing part of the business. The fastest growing segment of the wireless chip market over the past few years has been for high performance Bulk Acoustic Wave filters.

The wireless segment continues to be a significant and stable business for the group and is expected to grow at a rate of up to 5% in the near term. The division has a number of developments which provide routes for a return to double digit growth such as innovation in smartphone hardware, adoption of GaN on silicon technology for base stations and the transition to 5G communications. The group have also announced that they had renegotiated a long term supply contract with a tier 1 wireless customer through to September, securing an extended range of products and increased share of their epiwafer requirements.

The operating profit in the photonics business was £4.9M, a decrease of £1.5M when compared to the first half of last year. Revenue from the largest photonics customer was flat as inventory from the first mass market ramp of VCSEL epiwafters in H2 2017 was consumed in the supply chain. Other photonics customers were up 40%. Gross profits were adversely impacted by the Newport foundry pre-production costs of £900K and low margin customer funded product development reducing margins by a further £600K. Margins should improve again in the second half as the production efficiencies of the ramp in output are realised.

Sensing technologies such as 3D sensing and gesture recognition will represent a growth area in the near term. The group is engaged in a number of programmes for tier 1 OEMs who are targeting mass market ramps in 3D sensing applications over the next year and a half. Alongside the growth in the VCSEL business, the InP business continues to perform well. This market is being driven by the need for higher speed, higher capacity fibre optic systems to address continuing growth in data traffic. The group are engaged in qualifications with several customers for this technology and received their first milestone production order for DFB lasers made using their NIL process.

The operating profit in the IR business was £1.4M, flat year on year. Beyond defence, the IR division has been successful in broadening its customer engagements into product development for mass market consumer applications. They are now engaged with major OEM and device companies in developing IR products for consumer applications including sensing.

In the solar business, the terrestrial market remains an opportunity but as a result of the shifting macroeconomics, focus has shifted to the space market where these advanced materials are used to power satellites and UAVs where the higher efficiency has a dramatic cost benefit on payload. Product qualifications are underway with leading UAV/satellite manufacturers, paving the way for commercial revenues.

The operating loss in the CMOS++ business was £791K, an improvement of £186K compared to the first half of 2017. The group is involved in multiple programmes across the globe which are developing the core technologies from which they expect significant revenue streams to emerge over the next three to five years.

The Newport foundry construction and fit out it proceeding well. Five reactors had been installed by the end of the period and a further two have been delivered in August with three more scheduled in H2 to bring the total to ten reactors during the second half. Commissioning and qualifications are ongoing and initial production is expected to start in the latter part of H2 2018

There have been a number of one-off costs during the period. There was insurance income of £1.7M relating to the accrued insurance income receivable following the death of the CFO in April. There were exceptional legal costs of £900K incurred in respect of a patent dispute defence.

During the period the group received no revenue and made purchases of £1.8M from its joint venture in Singapore; and made purchases of £3.8M and recharges other costs of £1.6M with its joint venture in the UK Compound Semiconductor Centre.

There are a total of nine Compound Semiconductor Centre projects underway with a value of £5.4M. The projects have resulted in formal product development partnerships with five multinationals, four mid-sized companies, four SMEs and three additional academic partners. Routes to commercial income streams are now maturing and the first commercial orders were delivered in the period. The percentage of non-IQE revenue received by the centre is increasing steadily and is expected to be in the range of 15-20% for the full year.

A second phase of capital expansion focused on the installation of a new cleanroom and a GaN MOCVD reactor designed for Cardiff Uni research activity was completed in April. The business looks forward to progressing several key areas in the second half of the year including delivery of further exploitable outcomes of the CRD programme, diversification of the research roadmap and wider industry engagement to develop the commercial revenue pipeline.

The Compound Semiconductor Development Centre in Singapore is engaged in a number of early stage qualifications for new customers in China. Twelve new customer engagements were initiated for fifteen separate product qualifications including five for wireless pHEMTs and seven for photonics products. Following the growing tensions in the US and China’s trade and economic relations, China is reported to have sought to accelerate its efforts to gain semiconductor self-sufficiency by increasing funding.

The VCSEL wafer ramp for existing 3D consumer applications started as expected at the end of the period and since the period-end, the first production for new 3D sensing customers has also started. At this time the group has customer forecast demand to meet consensus revenue with a 40:60 revenue split for H1/H2 2018.

The group will invest around £6M in expanding GaN capacity in the US which will start in H2 and be completed in H1 2019. This will enable the closure of the NJ plant as the transfer of business to Taunton is completed. This consolidation is expected to save around £1.5M in 2019 and around £3M per annum thereafter.

They will also invest £15M in additional wireless capacity in Taiwan. This project will start in September and will complete in the first half of 2019, increasing capacity there by 40%. With this investment they will be able to avoid the cost of converting and reconverting reactors from wireless and photonics and back again which have totalled around £3M over the last year and a half and provide additional capacity for the wireless business.

The board remain confident of achieving current market expectations as long as there are no major forex movements. Next year wireless revenue growth is expected to be 0-5%, photonics 40-60% and IR 5-15%. The adjusted operating margins for wireless is expected to remain the same at 15% with photonics increasing 5% to 40% and IR up 1% to 28%. Capex on intangibles is expected to be £10-£15M with capex on fixed assets being £20-£30M. Sales phasing is expected to be 42:58.

At the current share price the shares are trading on PE ratio of 39 which increases to 42 on the full year consensus forecast. At the period-end the group had a net cash position of £40.6M compared to a net debt position of £41.9M at the same period of last year as a result of the placing to raise £90M to repay debt and fund capacity expansion.

On the 13th November the group announced that a major chip company had received notice from one of their largest customers for 3D sensing laser diodes that they would materially reduce shipments for the current quarter. As a consequence of the change in market conditions the group now expected to deliver revenues of £160M for 2018.

Photonics demand was facing a later but steeper ramp for VCSELs for consumer products moving into Q4 and with the impact of this recent announcement coming at this critical time, Photonics wafer revenue growth for 2018 is now expected to be 11% compared to previous guidance of 35% to 50%, and based on initial indications, it is currently expected to return to 40% to 60% revenue growth in 2019.

Wireless wafer revenue growth is expected to be 8%, above the 0% to 5% guidance. Wireless demand, especially for GaN products, has been strong and capacity was retained through Q3 to continue to address demand following the replenishment of inventory channels depleted in H2 2017. IR revenues are expected to grow at or exceeding the top end of the current guidance of 5% to 15% this year and to remain at in this range for 2019.

As a result EBITDA for 2018 is now expected to be around £31M compared to £37.1M in 2017.

On the 25th January the group released a trading update covering the year as a whole. They expect to deliver revenues of at least £156M and EBITDA of £27.5M compared to £154.4M and £37M last year. Net cash at the year-end was £20.8M compared to £45.6M at the end of 2017.

They closed their facility in New Jersey in order to consolidate US-based GaN manufacturing capacity in the Massachusetts facility. The cost of the closure is estimated to be £3.4M, of which £1.2M will comprise the cash costs of severance and reactor decommissioning with £2.2M of non-cash impairments. These costs will be an exceptional charge on the 2018 accounts and the group expects to achieve annual operating cost savings of around £3M per annum.

They also expect to incur an additional exceptional charge of £4.5M relating to onerous lease accounting provision for the period through to the end of the lease Q2 2022 for the unused and unlet space in the Singapore facility. They reiterate their 2019 guidance.

By the end of the first half of 2019 they will have completed a significant two year investment programme across their global operations, commissioning their new mega-foundry in Newport which is dedicated to photonics, installing additional wireless capacity in Taiwan, expanding their GaN capacity in the US and IR capacity in Milton Keynes. They will bring additional capacity into production in Phase 1 in the Newport foundry during H1 with 12 companies already actively qualifying the new facility.

Overall then this has been a rather difficult period for the group. Profits were down due to an increased tax charge – the operating profit was broadly flat. Net assets increased but the operating cash flow declined with no free cash generated. The photonics business suffered due to the excess inventory in the supply chain and the pre-production costs at the Newport foundry and the wireless business also saw profits decline, seemingly due to having to switch reactors from the photonics business. The shares are expensive with a forward PE of 42 but there is promise of future exciting growth. The trouble is this has always been the case here. Success has always been just around the corner and I’m growing a bit weary of it. I don’t think these offer good value at this price.