James Halstead has now released its final results for the year ended 2015.

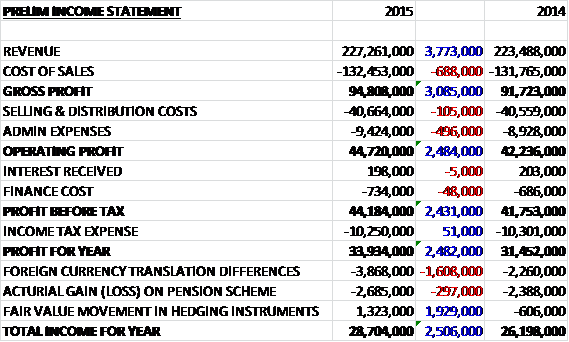

When compared to last year, revenues increased by £3.8M to £227.3M. The cost of sales also increased to give a gross profit some £3.1M ahead. Selling and distribution costs increased slightly but admin expenses grew by £496K so that operating profit came in £2.5M ahead of last year. Finance costs grew modestly but this was offset by a reduction in tax which meant that profit for the year came in at £33.9M, an increase of £2.5M year on year.

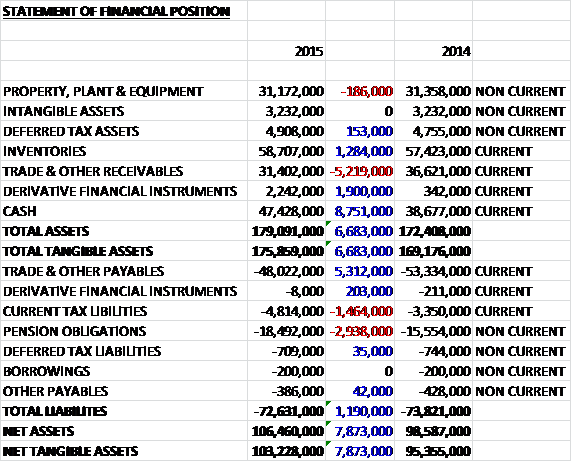

When compared to the end point of last year, total assets grew by £6.7M driven by an £8.8M increase in cash levels, a £1.9M growth in derivative financial assets and a £1.3M increase in inventories, partially offset by a £5.2M fall in receivables. Total liabilities fell during the year as a £2.9M increase in pension obligations and a £1.5M growth in current tax liabilities were more than offset by a £5.3M decline in payables. The end result is a net tangible asset level of £103.2M, an increase of £7.9M year on year.

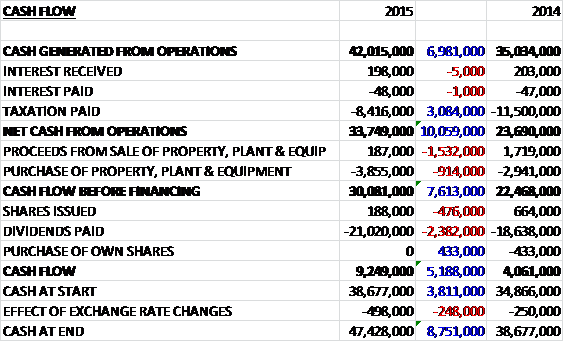

Annoyingly there is no split for changes in working capital so the cash generated from operations was £42M, an increase of £7M when compared to last year. This was further improved by a £3.1M decline in the amount of tax paid so that the net cash from operations was £33.7M, an increase of £10.1M year on year. The group only spent £3.9M on capital expenditure so there was an impressive free cash flow of £30.1M, of which £21M was spent on dividends with the rest becoming the cash inflow for the year of £9.2M to give a bulging cash pile of £47.4M at the year-end.

The group have consolidated their position as the UK market leader and UK growth of 10% has driven this year’s results as the factory in Teesside continues to be crucial to the growth. Europe continued to represent a sizeable portion of the business (about 40%) and this has grown by 5% in local currency. The Australian business has improved on the disappointing results of the last couple years, increasing turnover by 15% in local currencies. Manufacturing efficiencies, stable raw material prices and economies of scale as Teesside output grows have helped protect margins.

At Polyflor Nordic, turnover was broadly on a par with previous years. There has been good progress in the sale of manufactured product and in particular, with the introduction of product manufactured at the Teesside facility. During the year the group have installed the most northerly Polyflor in the world in Longyearbyen, a city well inside the Arctic Circle, on student’s apartments.

Objectflor has shown growth with sales 3.9% ahead of the priod year. During the year they launched Expona Flow at the BAU exhibition in Munich. It is a brand of luxury vinyl sheet and the market response was apparently excellent. Gross margin was under pressure due to extensive competition in the luxury vinyl tile sector and due to the weakness of the euro but this pressure was offset by favourable product mix and profit increased by 3.9%. The French business has continued to grow with a 5% sales increase. It still has a relatively low market share and with a broader range the group expect the business to expand again next year.

The Australian turnover was 15% ahead of last year and there has been an increase in gross margin, which was expected after the group undertook a large stock cleansing exercise in the prior year. This was partially offset by increased import costs due to the weakness of the Australian dollar. New Zealand turnover increased by 1.1% and the company continues to win projects to augment the refurbishment sector. The Housing New Zealand contract to supply social housing is adding to the solid position in the country. In Asia, the group faced a difficult year with sales dipping slightly below last year. The sales mix was towards the higher-end ranges, however, with profitability increasing. China continues to be the lead market in the region but it was lower this year as a result of the widely reported slow down, nevertheless the LVT and Expona Flow ranges fared well in retail and healthcare. In the rest of the region, Singapore, Thailand, the Philippines and South Korea all shared good growth.

It was a solid year for the UK manufacturing operations with turnover up 4.1%. The launch of Secura in June 2014, Expona Flow in February 2015 and Designatex in June 2015 are adding volume to the plants. In the UK, turnover was up 10% reflecting market growth and increased market share but there is competition from Euro-based rivals. Gross margins were maintained against the pressures of exchange rates due to the increased volume through the UK plants. Some projects completed included the refurbishment of Astra Zeneca’s Alderley Park R&D facility, the Rolls Royce Apprentice Academy in Derby, and the National Space Centre in Leicester.

It is third year as a distributor in Canada, the business continued to grow with turnover up 14%. A warehouse has been based in Ontario which has been a good asset and the introduction of the Expona ranges of LVT are building on the established Polyflor ranges. The board are positive on future growth in the country. Polyflor India was formed in the early part of the year and the initial focus has been on recruiting local sales reps. Sales have been encouraging but in its first year the business made a small loss. The group are working alongside their long standing distributor who is focused on the region around Delhi but the team is now winning sales in Gurgaon, Bangalore, Goa, Guwahati and Mumbai. The pace of growth in the country is significant and the strategy is aimed at new build in the healthcare and educational sectors rather than the refurbishment market.

Sales to South America showed growth with a 42% increase over the prior year. The Middle East, despite turmoil in several countries, has progressed some 9% with Kuwait, Oman, Qatar and the UAE showing year on year growth. In Africa, sales to Kenya, Nigeria and South Africa all significantly increased. The Russian market is depressed and given the state of the economy this is likely to remain the case but Poland, Latvia, Lithuania and Romania all continued to grow.

A number of new contracts won during the year include the Stade des Lumieres, built in Lyon for Euro 2016; Matru retail stores in Chennai; and Queenstown International Airport in New Zealand.

In many of the group’s markets confidence in growth has taken root but there is still some way to go in the global recovery which bodes well for new build projects. The board are encouraged that their launches of Designatex and Expona Flow towards the end of the year have been well received and there is an increasing amount of safety flooring that is manufactured in Teesside which is a trend that will continue to give economies of scale. In recent months, the group has been fighting against the strength of Sterling against the Euro which they expect to continue into the new year but there have been some offsetting factors such as cheaper input prices of raw materials and the board remains positive.

After a 12.3% increase in the final dividend the shares yield 2.7% which increases to 2.9% on next year’s consensus forecast. At the current share price the shares trade on a fairly hefty PE ratio of 25.3 falling to 24.9 on next year’s consensus forecast. There is no debt so the net cash position stands at £47.4M – I wonder what they will do with it all…

Overall then this has been another strong year for the group. Profits and net assets were both up and the operating cash flow also increased with the group producing loads of free cash which boosted the already sizeable cash levels. Trading was good in the UK, as it was in the EU and Australia but adverse currency issues affected these two markets. Things were harder in China and Russia due to the well-documented problems in these countries and considering China is the group’s largest Asian market, there is some exposure to risk here. On the cost side, the strong sterling has been offset by greater economies of scale in Teesside as more product in manufactured there and a relatively benign raw material price environment.

New ranges have been introduced towards the end of the period and with a dividend yield of 2.9% I am more than happy to keep holding what is one of my largest positions. The forward PE of 24.9 looks expensive but this is undoubtedly a quality outfit with a lot of net cash so it is perhaps warranted.

The chart also looks rather good here.

On the 27th November the group released a statement covering the first five months of the year. Trading in the year so far has been in line with budgets. Turnover on a constant currency basis is ahead of the same period last year but on a par on a reported basis due to the effects of exchange rate translation. Profits are ahead of last year and the board believe first half results will be in line with management expectations. They have also announced a special dividend equal to 7.858p (the same as the final dividend) so that is a nice bonus for shareholders!

On the 3rd December it was announced that Mr Wild, a non-executive director of the company, sold 33,000 shares with a value of £165K. He still owns 150,300 shares but this represents quite a hefty sale.

On the 1st February the group released a pre-close trading update covering the first half of the year. Turnover has increased in each of their major markets on a constant currency basis but currency translation to sterling had an adverse impact of 10-15%. Despite this, the profit for the first six months trading is ahead of last year and in line with the board’s expectations and confidence in the full year is unchanged and remains positive.