Martin & Co has now released its final results for the year ended 2015.

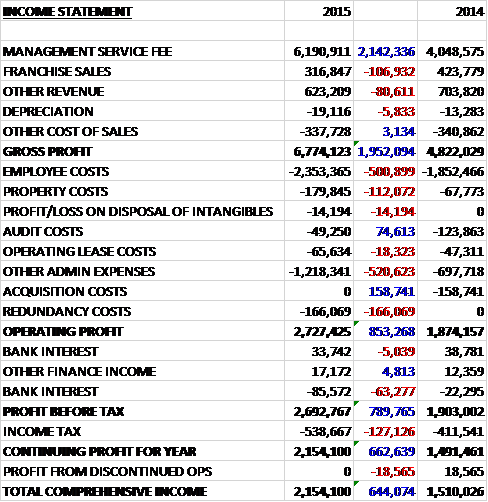

Revenues increased when compared to last year as a £2.1M growth in management service fee revenues, £1.7M of this due to the acquisition last year, was partially offset by a £107K decline in franchise sales and an £81K fall in other revenue after the Saltaire portfolio was sold in January. Cost of sales were flat which meant that gross profit increased by just under £2M. Audit costs fell by £75K but employee costs grew by £501K, property expenses were up £112K and other admin expenses grew by £521K which meant that after redundancy costs of £166K following last year’s acquisitions broadly offset the lack of acquisition costs that occurred last year, the operating profit was £853K ahead of 2014. Bank interest grew by £63K and tax expenses were up £127K to give a profit for the year of £2.2M, a growth of £663K year on year.

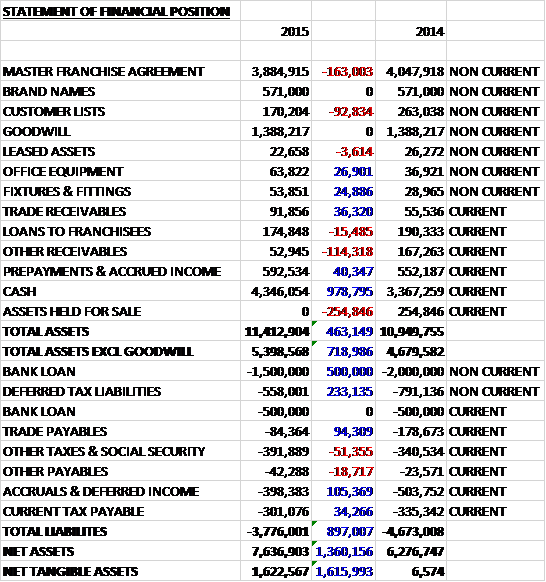

When compared to the end point of last year, total assets increased by £463K driven by a £979K growth in cash, partially offset by a £255K elimination of the assets held for sale, a £163K decline in the value of the master franchise agreement as it is amortised, a £114K fall in other receivables and a £93K decrease in the value of customer lists. Total liabilities fell during the year due to a £500K reduction in the bank loan, a £233K decrease in deferred tax liabilities due to an increase in share based payments, and a £105K reduction in accruals and deferred income. The end result is a net tangible asset level of £1.6M, a growth of £1.6K year on year.

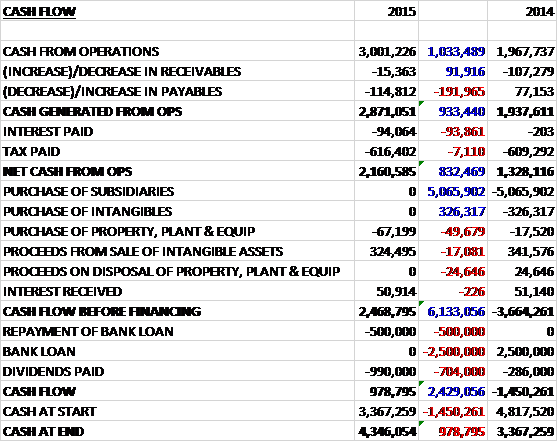

Before movements in working capital, cash profits increased by £1M to £3M. There was a modest outflow of cash through a decrease in payables and interest payments grew by £94K to give a net cash from operations of £2.2M, a growth of £832K year on year. The group only spent £67K on capex and received £51K in interest along with £324K from the disposal of intangible assets relating to the disposal of the Saltaire portfolio to give a strong free cash flow of £2.5M, of this £500K was used to repay the bank loan and £990K was paid out in dividends to give a cash flow for the year of £979K and a cash level of £4.3M at the year-end.

During the year the group opened thirteen offices, seven of which were in new territories for them. Cold start offices launched with new franchises in Kingston, Plymouth, Hull, Wokingham, Gloucester and Greenford and offices were opened by existing franchisees in Downend, Cirencester, Worcester, Chester, Longbridge, Ashford and Huyton.

The group ended the year manging over 45,000 tenanted homes which means collecting and accounting for £34M in rents every month. The first part of the year was substantially taken up with the integration of Xperience into the group. The business operated out of two headquarter buildings, one in Leeds and one in Theale. The group never occupied the Leeds building and disposed of the lease at Theale. All the costs of the re-organisation and assimilation of Xperience have been incurred and they enter 2016 with a lowered cost base.

The vast majority of the group’s franchisees have been franchisees for five years or more which means that their initial bank loans will have been paid down and these businesses should be well placed to raise new funds to acquire competitors with the group intending to put more energy into this activity during the coming year.

The group will rolling out a financial services strategy to all their offices during 2016. The proposition will be a “whole of market” selection of mortgages and fee-free advice. Life Assurance and General Insurance products will be tied to Legal and General and the benefits of this strategy will be increased income from financial services, which currently account for just 1% of fees, and greater understanding of customers.

Enquiries from potential franchisees have been on a steep rise during Q4 2015 and the group achieved their highest number of new recruits in three years and opened 13 new offices. The board remain very positive about prospects for the private rental sector and they aim to surpass this year by a substantial margin in 2016.

Having built up the lettings business, the group are now focusing on advancing the residential sales side of the business. The number of house sale transactions completed across the group increased from 2,201 to 7,689; offices offering an estate agency service increased from 243 to 256; and a financial services strategy has been agreed with business partner Legal and General and will roll-out during 2016.

The franchisees pay a management service fees which is 9% of all income for Martin & Co offices and 7.5% for the other brands, although this will be increased to 9% when franchises renew. In addition, franchisees contribute to a marketing promotions fund and the total contributed during the year was £694K. The franchisees decide on the use of this fund and this has included sponsorship of international rugby and cricket.

There are a number of drivers for growth. Pension reform has enabled the over-55s to access retirement funds which can be used as a deposit on a buy-to-let property and the record net migration into the UK drives further demand with the foreign-born UK population being three times as likely to be in the private rental sector. In addition, the government is increasing regulation on landlords. Deposits must be registered, new health and safety rules for rented homes, and checks on a tenant’s right to rent in the UK, all of which makes rental agents more appealing.

Regardless of minor regulatory or fiscal adjustments, the demand for property in the UK has never been greater and the board have confidence in the future for the group.

The group still have £3M undrawn from the Santander facility so they have plenty of headroom with their debt. At the current share price the shares are trading on a PE ratio of 15.5 which falls to 11.5 on next year’s consensus forecast. After a 47.5% increase in the total dividend, the shares are yielding 4% which rises to 4.5% on next year’s forecast.

Overall then this has been a good year for the group. Profits were up, net assets increased, and the operating cash flow grew with a good amount of free cash generated. The Xperience acquisition is now integrated so the full benefits of that should be seen in 2016, along with the introduction of the financial services offering. Enquiries in Q4 were up considerably, which also bodes well for the coming year. Of course there are always risks with these kind of businesses but with a forward PE of 11.5 and yield of 4.5%, these shares look good value. I have bought back in here.