Moss Bros has now released its prelim results for the year ended 2016.

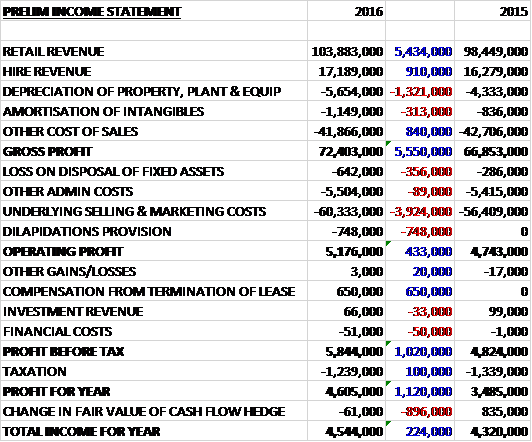

Revenues increased when compared to last year with a £5.4M growth in retail revenue and a £910K increase in hire revenue. Depreciation was up £1.3M and amortisation increased by £313K but other cost of sales fell by £840K to give a gross profit £5.6M above that of 2015. There was a £356K increase in the loss on disposal of fixed assets and selling and marketing costs were up £3.9M with a dilapidations provision of £748K which is being treated by the company as non-underlying. This means that the operating profit grew by £433K. We then see a £650K compensation from the termination of a lease and a £100K fall in tax charges, although finance costs did increase with investment revenue down. This all meant that the profit for the year came in at £4.6M, a growth of £1.1M year on year.

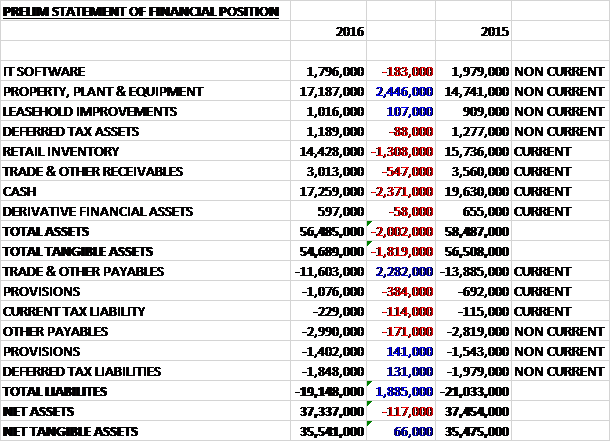

When compared to the end point of last year, total assets declined by £2M, driven by a £2.4M decrease in cash, a £1.3M fall in inventories and a £547K decline in receivables, partially offset by a £2.4M increase in property, plant and equipment. Total liabilities also declined during the year as a £2.3M fall in payables was partially offset by a £243K growth in provisions. The end result is a net tangible asset level of £35.5M, broadly flat year on year with a growth of just £66K.

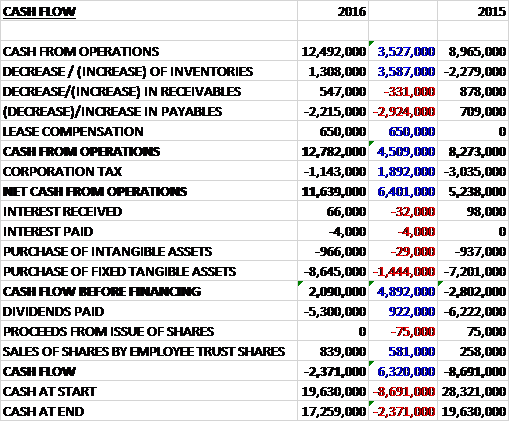

Before movements in working capital, cash profits increased by £3.5M to £12.5M. Working capital was broadly neutral, although compared to last year’s outflow, there was an improvement and we also see the £650K received in compensation for the end of a lease. After a £1.9M reduction in the tax paid, the net cash from operations came in at £11.6M, a growth of £6.4M year on year. The group spent £8.6M on property, plant and equipment which included the opening of four new stores, fore store relocations and the refit of 16 stores along with £966K on intangible assets to give a free cash flow of £2.1M which did not cover the £5.3M of dividends so there was a cash outflow of £2.4M for the year and a cash level of £17.3M at the year-end.

The planned acceleration of the store refit programme means that 81 of the 124 stores are now trading in the new format at the year-end. As planned, this increased investment has impacted cash in the short term but the three year payback means the group will quickly recoup the funds invested.

The gross profit in the retail business was £58.6, an increase of £5.2M year on year as the accelerated refit programme led to like for like sales increasing by 7.6%. Retail gross margins also improved, increasing by 2.2 percentage points as a result of more focused promotional activity. The promotional activity around Black Friday, again generated significant customer interest but this year the group were able to manage their exposure to discounting more effectively through a carefully targeted campaign.

As planned they opened four new store and closed ten during the year and a further four stores were relocated into larger sites in better locations. The board are considering further new store opening opportunities over the next year and currently have three confirmed openings. They now trade from 124 stores compared to 130 at the end of 2015. The average lease length across the store portfolio is 59 months and they are targeting improved lease terms on renewal of a ten year term with a tenant only break clause half way through.

The gross profit in the hire business was £13.8M, a growth of £305K when compared to last year with like for like sales increasing by 11.7% reflecting the recovery in wedding hire in the year. The broadening of the range to include lounge suits has proved successful and has received positive customer feedback. Weddings, evening wear, Royal Ascot and school proms all showed good levels of growth. The group have invested further in new hire stock, supplementing the lounge suit offer with two new styles and adding to their branded ranges which have proved popular.

E-commerce sales performed strongly, increasing 36.3% on the prior year and now represent 10% of total sales. Expansion into international markets has been refocused to concentrate on dedicated, local currency sites for Ireland, Australia and the US. The hire website continues to gain traction and it is believed that it is capable of further growth. Results are encouraging and the incidence of wedding hire customers beginning their journey online before buying from stores is becoming more prevalent. There are a number of enhancements planned for the year ahead to improve the customer experience and conversion rates.

Actions to develop their product offer have included the launch of “Tailor Me”, a more accessible form of bespokng which will allow a significant proportion of the group’s suit range to be personalised. Following a pilot, this is now available in 25 stores and will be rolled out across the entire estate by September.

There are a couple of exceptional items this year. An exceptional credit was received following the renegotiated exit from a retail location where the landlord paid compensation for the release of certain lease obligations of £650K. An exceptional charge of £748K was incurred in respect of property dilapidations. As a result of the stores increasingly moving away from the high street and towards shipping centres and retail parks, the group have refined their estimation technique for calculating dilapidation provisions.

Given the change in estimate and the unusually high number of dilapidation claims received in the period there has been a large dilapidations charge to the income state. The size of the charge in the current year means that this meets the board’s definition of an exceptional item. Last year a charge of £100K was incurred which was treated as an underlying item. It is not clear whether the whole amount of the dilapidation charge has been taken as an exceptional item or just the amount above the £100K norm. If the former, then the group is surely overstating underlying profits by £100K.

It is also notable that the group overstated their profits last year by £403K because they included the benefit of corporation tax deductions arising from the exercise of share options in the income statement when apparently tax benefits above the designated IFRS2 charge should be recognised directly in the statement of changes in equity rather than the income statement. Last year’s accounts have been amended accordingly.

The group recruited Sara Gomez as People Director during the year, and this was followed by the appointment of Paula Minowa as COO to accelerate the development of their multi-channel and international aspirations. In September, Finance Director Robin Piggott announced this intention to retire following the AGM and he will be replaced by Tony Bennett who will join in August from Charles Tyrwhitt, a menswear retailer.

Having invested £2.4M in new hire stock during the year, the group are intending to invest a further £2M during the coming year. They anticipate central costs will increase in line with turnover as investment in the multi-channel capability continues and including the £2M of hire stock investment, the overall capex for 2017 is expected to be around £9M with £3.3M of that as a result of 20 store refits.

Like for like sales in the first nine weeks of the new financial year are up 5.2% with growth seen across in-store retail, e-commerce and hire with the broadening of the hire offer to include lounge suits underpinning a positive start to the 2016 hire season and overall trading is in line with the board’s expectations despite the continuation of competitive market conditions.

The group had a net cash position at the year-end with cash levels at £17.3M compared to £19.6M at the same point of last year. At the current share price the shares are trading on a PE ratio of 22.6 which reduces to 19.5 on next year’s consensus forecast, which looks rather expensive. After a 6% increase in the total dividend, the shares are yielding 5.5% which is expected to remain the same next year.

Overall then, this has been a fairly good year for the group. Profits were up, net tangible assets remained flat and the operating cash flow increased with some free cash generated, albeit not enough to cover the dividends. The retail business increased profits as the refitted stores increased their contribution and the group made more focused marketing efforts, particularly around black Friday. The hire business also increased its profit, mainly as a result of a recovery in wedding hire.

There are just over 43 stores still to refit which should continue to deliver increased profits, albeit at the expense of increased investment, and like for like sales so far this year are up. For me, this has probably been priced in already, however, with a forward PE of 19.5 and an uncovered yield of about 5.5%. The shares are a little pricey for me.