National Grid has now released its interim results for the first half of 2012.

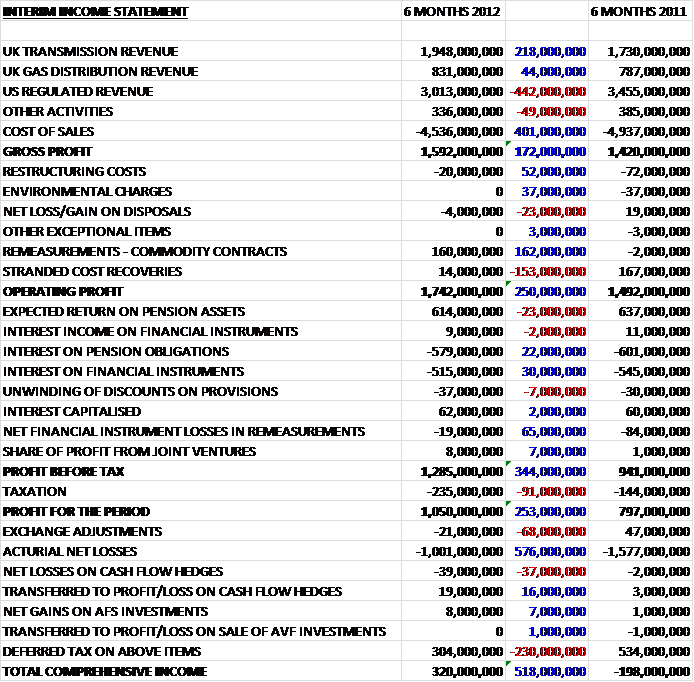

A bit of a mixed bag here. We can see that revenue from the UK business is doing well, up by £262M but this was counteracted by a £442M fall in US revenues and a £49M fall in other activities (all main sectors increased profits). The cost of sales was down too, however, so gross profit managed to increase by £172M. There were less restructuring costs and a lack of environmental charges, which helped, We can also see that remeasurements on commodity contracts gained an extra £162M on last year, this was offset by a £153M reduction in the stranded cost recoveries, which look like they have worked their way through the system now. This means that operating profit was £250M better off than in the same period of last year. The profit from Joint Ventures related to dividends from Iroquois Gas Transmission System and Millennium Pipeline Co (both for £4M). The share of profit from joint ventures increased mainly due to the larger contribution from the BritNed interconnector.

After interest and taxation has worked its way through, the profit for the year was £253M up at just over £1B. Looking at total comprehensive income, however, we can see this was wiped out by a £1B actuarial loss (presumably on the pension scheme).

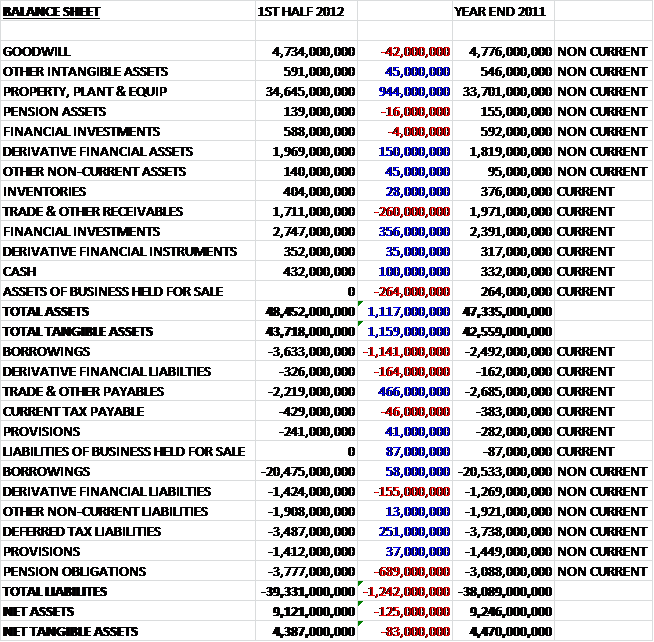

The total assets for the group increased by £1.117B during the half year. The bulk of this increase, as usual, comes from the capital invested in property, plant and equipment which now stands at a staggering £34.7B. Other large increases came from financial investments and derivative financial assets. The only significant decreases were trade and receivables, down £260M and the sale of the business held for sale meant a reduction in value of £264M as far as that was concerned.

Liabilities also increased (up £1.242B), driven mainly by an increase in borrowings of over £1B. The other big increase comes from pension obligations which were up a worrying £689M to £3.777B. Not all liabilities were up, however. There was a £466M reduction in trade and payables and a £251M reduction in deferred tax liabilities. Overall, liabilities increased at a faster rate than assets so net tangible assets were £83M down to £4.387B. Considering the business strategy for National Grid, it is quite important for them to increase value so this is a bit of a disappointment. It could be argued that were it not for such a large hike in pension obligation, however, this would have been achieved.

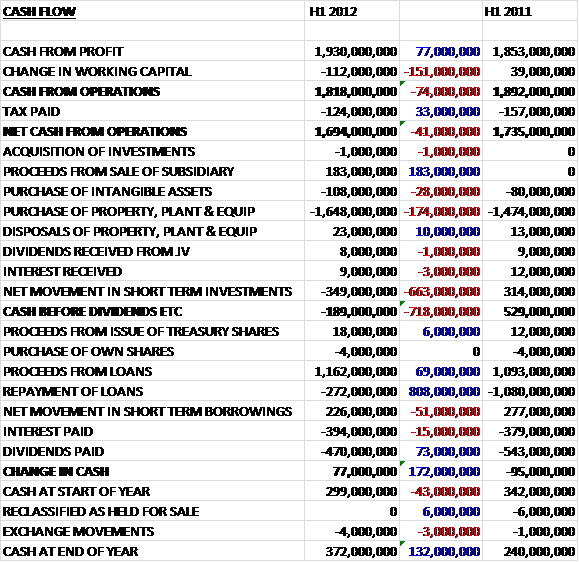

We can see here that after adverse changes in working capital, brought about by weather and commodity costs in the US, and a smaller tax payment, the net cash from operations was £41M lower than the same period of last year at £1.694B. This was almost entirely swallowed up by capital investment in property, plant and equipment (£1.648B, up by £174M). The increase in capital investment for this half year was due to investment in the UK transmission business and an increase in the gas transmission equipment investment in the US. Another large destination for the cash was movements in short term investments. Before we even consider the interest paid (394M) and the dividends (£470M), we were in a position of negative cash flow so a net £1116M of new loans was required to keep things on an even keel. At the end of this, there was a positive cash flow of £77M but this seems pretty much academic as National Grid just borrows more money to cover any shortfalls.

The dismissal of the anti-trust claims relating to the KeySpan class action was confirmed on appeal, which leaves the only course of action available to the claimants is to petition the supreme court to overturn the decision so the slight cloud hanging over the group with regards to that seems to be gradually lifting.

In October superstorm Sandy hit the NE US, affecting the power supply to National Grid customers. The group are expecting the financial impact of this to be about £100M. It does seem that lessons have been learnt from past storms, however, and restoration targets were met in New York, Rhode Island and Massachusetts. Long Island was more severely affected, however, and it is unclear whether any fines will be levied here due to not meeting targets.

New UK guidelines for future tariffs are expected to be outlined by the government later in the year and will determine the framework for investment into the infrastructure of the system for the next decade or so. This is a very important framework and National Grid will align their business accordingly. Negotiated settlement recommendations for new rates in the Long Island Generation, Rhode Island (a 9.5% RoE) and New York (9.3% RoE) businesses have been agreed in principle and if agreed will enhance takings in those markets.

In the first half of the year, there was a £28M over-receipt which will have to be given back. Operating profit was £185M up on last year but that included £71M of costs relating to Hurricane Irene. The rest of the increase was predominantly down to the impact of inflation linked returns from the UK businesses.

For UK operations, UK inflation is expected to contribute £75M to the allowed gas distribution fees this year and the one year transmission review increased the amount of allowed revenues by £200M. UK controllable costs and depreciation are expected to increase, reflecting inflation, staff recruitment and high levels of capital investment. For the US, reductions in controllable operating costs are likely to be offset by inflation and other cost increases. The effect of Superstorm Sandy is likely to be about £100M. Additional costs associated with the US financial system and process implementation are expected to impact the results of other activities.

Operating profit for UK Transmission operations was 18% up to £712M and there was a £10M balance of under-recovered fees at the end of the half year. The increase was due to the rollover of the transmission price control agreement and included an increase for RPI. Costs increased somewhat, mainly due to ongoing recruitment and development of the UK operating model. The system reliability was excellent during this period. For the rest of the year, costs are expected to increase, offset by an increase in income and the continued recovery of under-recovered revenues.

Operating profit for UK Gas Distribution was 7% up to £408M. The increase was due to higher regulated income due to the RPI linked tariffs. Costs were up a small amount too, mainly due to increased emergency workforce costs. The five year price plan for Gas Distribution in the UK is shortly coming to an end so it will be interesting to see what is achieved in the next price plan. Capital investment in the gas distribution business is at a broadly steady rate and involves work on mains replacement.

Operating profit for the US regulated business was up 27% to £404M, which includes an over-recovery balance of £39M which will have to be paid back to customers. The increase in profit is also due to the fact that this period of last year included £71M in respect of hurricane Irene and recovery of deferred costs from the New York electricity business. Reliability was fairly strong, with 14 out of 15 targets met. The sale of the New Hampshire electric and gas distribution business, Granite State Electric Co was completed to Algonquin Power & Utilities Group in July. The main areas of new investment were increased spend on transmission and mains replacement in the Massachusetts gas business. The clean up after Superstorm Sandy has involved over 15,000 crews and took significantly longer than Hurricane Irene last year.

Operating profit for other activities fell by 48% to £68M. This fall was due to an increase in costs related to US systems and finance restructuring and the sale OnStream metering services in October 2011 (OnStream contributed £12M in the first half of last year). LNG storage profits remained similar to that of the same period of 2011.

After the increase on contribution from the BritNed interconnector, the group is looking at other similar joint ventures such as interconnectors between the UK and Norway, Ireland, Belgium and France.

All in all, not too bad I guess. US revenues are down, counteracted in increases in UK revenues but costs were also reduced and the group recorded a decent increase in profits. Net assets sadly fell as a huge increase in pension obligations seemed to take its toll. All of the cash generated is used in capital expenditure and the group just borrows more and more money to pay for everything else. Net Debt Now £20.358B, up £761M on the end of last year as the group issued new bonds, including the largest Canadian Dollar bond yet, in order to diversify sources of liquidity. By the end of the year, net debt is expected to reach £21B. I am not sure why OnStream was sold as this seemed to generate profit and diversified the group away from regulated income so I was a little sad to see that go. Also, the costs of the cleanup following Superstorm Sandy will be included in the second half results and that will be significant. The dividend is up slightly to 5.1% and a new policy will be announced by May 2013 following the outcomes of regulatory developments.

In conclusion then, I am still not sure what to make of National Grid. The business model just can’t be sustainable long term but the 5.1% return with the dividends is considered safe. So I suppose I will continue to hold and maybe sell out if something more interesting comes along.

On 17th December, Ofgem announced the plans for future investment into the UK gas and electricity grid. £24.2N was earmarked to upgrade the structure, some £7B less than was requested. £4.5B of this will be made available only if companies can justify the expenditure. £15.5B of this money is to upgrade the high voltage electricity transmission network in England and Wales and the high pressure Gas network across the whole of Britain. A major project includes the building of a sub sea link to connect Scotland with England and Wales. The other £8.7B is to ensure Britain’s low pressure gas networks remain safe and reliable and include strict targets for network companies to carry out Carbon Monoxide awareness initiatives. It is good to have this set out, it is a shame that there is a £7B difference but I am not sure if this was predicted or not.

On 21st December, the group announced that the rate submission for Rhode Island has been agreed. The plan includes a 9.5% RoE, pension trackers and increased operating cost allowances. The rate plans provide a revenue increase of $21.5M for electricity operations and $11.3M for gas ops. There is also an annual property tax recovery mechanism that more closely aligns rate recovery and costs related to property tax expenses. This seems like a decent outcome.

On 17th January 2013, National Grid announced that a rate extension for the New York gas business had been agreed. The proposal includes a 9.4% RoE and includes a clause whereby 20% of earnings above this amount can also be retained by the group. The proposed agreement also includes an increase of capital expenditure allowances and updates to customer service and performance metrics. This agreement will run for two years and is financially very similar to the one which it replaces.

On 29th January 2013, the group issued an interim management statement which went over some of the previous announcements and went into more detail about other issues. It was stated that capital investment during this year would be around £3.6B. It was also mentioned that the group had not finished going through the Ofgem proposals to check for the acceptability of the plans, that process is due to be completed by Match. Another development was the fact that the NYPSC has granted an order so that thew current recovery surcharges of about $65M per annum be extended to recover past expenditures of around $200M.

In Massachusetts an order detailing $19M of penalties relating to the response to Tropical storm Irene and the October Snowstorm was issued. National Grid are appealing this amount. The update went into a bit more detail on the Rhode Island rate that was agreed in December. The effect of this rate change will increase annual revenue allowances for electric operations by $21.5M and for gas operations by $11.3M, which sounds fairly promising.

During the period, the group updated a number of IT systems and this caused problems in payroll processing. Hopefully this will not be a big issue and staff members will be paid appropriate amounts – not sure how a company with the resources of National Grid can suffer these kind of IT problems, though. There has been no material changes in the financial position of the company and the group was able to obtain £1B more of long term debt to add to the debt they currently have.

Going forward, as the group continues to digest Ofgem’s proposals, more clarity is being given to operations and the plans are likely to control the direction in which National Grid goes in future.

On 28th February, National Grid announced that it had accepted the price control arrangements proposed by Ofgem as the board believes that the combination of revenue allowances and incentive mechanisms provide a good opportunity to earn appropriate returns for investors. It also offers the longest ever period of regulatory clarity – this seems like good news to me.

On 15th March, the group announced an agreement for the New York set rates. The three year rate period allows a 9.3% RoE and increased operating cost allowances. There is a cumulative revenue increase of $123M for electric operations and a $9M increase for gas operations by the end of the third year. The rates include a capital expenditure program of $1.6B. Sounds good for electric operation, but I guess there is a revenue decrease for the electric operation in the first year or two.

On 28th March, National Grid announced their new dividend policy. It is intended that the dividend will grow at least in line with the rate of RPI inflation each year. Funding going forward will be sources from retained equity and increases in net debt. Trading towards the end of the year has progressed well and earnings are likely to be slightly ahead of previous expectations where stronger trading in the UK transmission business and lower net finance costs should counteract the effect of the storm restoration work.