Omega Diagnostics has now released their interim results for the year ending 2020.

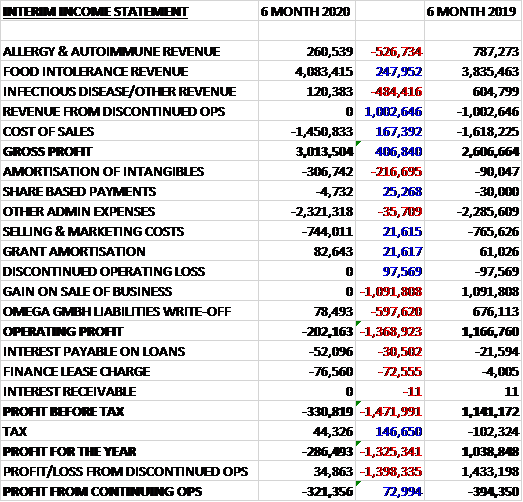

Revenues declined when compared to last time as a £248K growth in food intolerance revenue was more than offset by a £527K decline in allergy revenue and a £484K decrease in infectious disease revenue. Excluding the £1M revenue from discontinued operations, the gross profit increased by £407K. Amortisation was up £217K, there was no £1.1M gain on the sale of a business and Omega liabilities written off decreased by £598K to give an operating loss £1.4M worse that the first half of last year. Finance charges were up slightly but tax charges decreased by £147K which meant that the loss for the year was £321K, an improvement of £73K year on year.

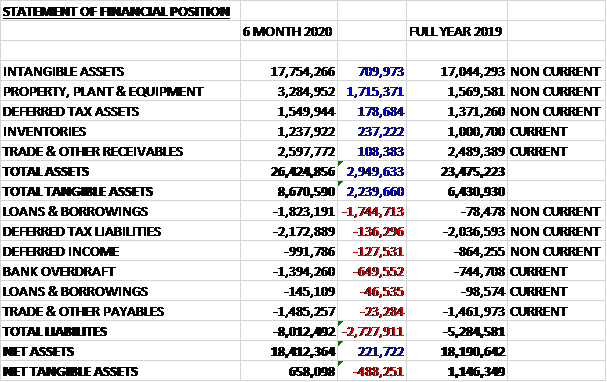

When compared to the end point of last year, total assets increased by £2.9M, driven by a £1.7M growth in property, plant and equipment, a £710K increase in intangible assets and a £237K growth in inventories. Total liabilities also increased during the period due to a £1.8M increase in borrowings and a £650K growth in the bank overdraft. The end result was a net tangible asset level of £658K, a decline of £488K over the period.

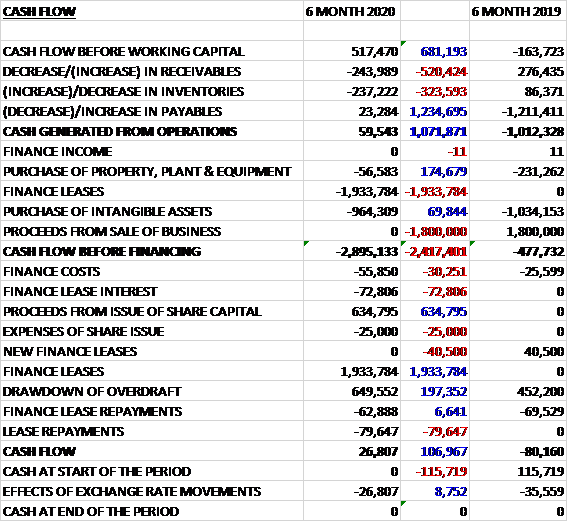

Before movements in working capital, cash profits improved by £681K to £517K. There was a cash outflow from working capital but this was less than last time and the group generated £60K of cash from operations, an improvement of £1.1M year on year. This didn’t come close to covering the leases, however, which were £1.9M. The group also spent £964K on intangible assets and £57K on fixed assets so that before financing there was a cash outflow of £2.9M. The group made £635K from new share issues, £1.9M from finance leases and £650K from the overdraft which gage a cash flow of £27K and no cash left at the period-end.

The pre-tax loss for the Allergy and Autoimmune business was £139K, a deterioration of £77K year on year.

The pre-tax profit for the Food Intolerance business was £1.7M, an increase of £228K when compared to the first half of last year with revenues up 6%. Two customer orders amounting to £200K were ready to be shipped by the period-end but were not picked up in time to be included in the results. Sales of Food Print lab reagents increased by 12% with growth in the top five markets. Sales of Food Detective were flat with an uplift of £290K of sales to the new Chinese partners offsetting £120K of sales shipped late.

The pre-tax loss for the Infectious Disease business was £1.3M, a deterioration of £552K when compared to the first half of 2019. For the CD4 350 test they have made progress in signing distribution agreements and now have distributors in 19 countries with the advanced disease test being added to nine of those. There are a further three countries for which distribution discussions are continuing. They are still awaiting the outcome from the Nigerian Ministry of Health and they continue to remain confident about the prospects for the country being the largest market for the test.

For the advanced disease test, they have received an order from Zimbabwe and expect to receive further seeding orders from other countries this year. Following receipt of ERPD approval in September, they are in discussions with the Clinton Health Access Initiative to implement their Advanced disease initiative. They have identified four countries to act as early adopters of the test. They are making good progress with the WHO Prequalification process with the tests finished in early 2020.

Admin overheads increased by £220K. The majority of this increase relates to amortisation of the allergy and CD4 intangible assets. The allergy assets started amortisation in April and CD4 in August in line with the commercial launches of these products.

Going forward, the food intolerance division continues to grow and the board remain confident that this unit will deliver double digit revenue growth this year, helped by the new Chinese partner having placed stocking orders for 50,000 units in preparation for their expected regulatory approval in China. The partner in Nigeria has ordered 200,000 CF4 350 tests, deliverable in January to March which is conditional on receiving approval from the Ministry of Health.

The group made a loss last year and is predicted to make one this year too so PE ratios are pretty redundant. There is no dividend on offer.

On the 17th January the group announced that they had received approval from the Nigerian Ministry of Health for the 350 test to be deployed in the country. They have received initial orders from their distribution partner in Nigeria for 250,000 tests and they will now look to firm up a delivery schedule to determine what proportion of this demand can be shipped prior to the year-end.

Overall then this has been a difficult year for the group. Losses from continued operations did improve somewhat but the net tangible asset level deteriorated and the operating cash outflow also got worse, with no cash being generated. The Food Intolerance business seems to be doing well but the infectious disease business is using up a lot of resources. Hopefully this will reverse at some point with the Nigerian approval but it is hard to quantify. The Allergy business seems to be on its last legs. Overall I think this looks too risky at the moment but could be become interesting at some point in the future.