Orosur Mining has now released its results for Q3 2016.

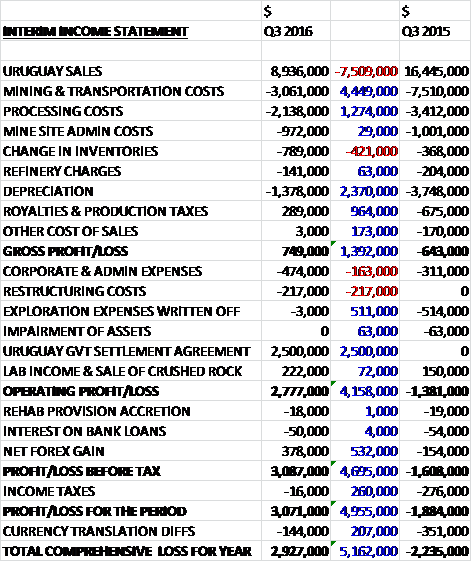

Sales reduced by $7.5M when compared to Q3 last year but cost of sales also declined with a $4.4M reduction in mining and transportation costs, a $1.3M fall in processing costs, a $2.4M decrease in depreciation and a $964M positive swing in production taxes as the group enjoyed an exemption from royalty payments, which meant that the group showed a gross profit of $749K, a $1.4M positive swing. Admin costs increased by $163K, however, and there were $217K of restructuring costs but there was a $511K reduction in exploration costs written off and the lack of $63K of asset impairments that occurred last time. We then see a $2.5M settlement agreement with the Uruguay government which drove a $4.2M improvement in the operating profit to $2.8M. There was then a $532K positive swing in forex movement and income taxes were down $260K which meant that the profit for the period came in at $3.1M, a positive movement of $5M year on year.

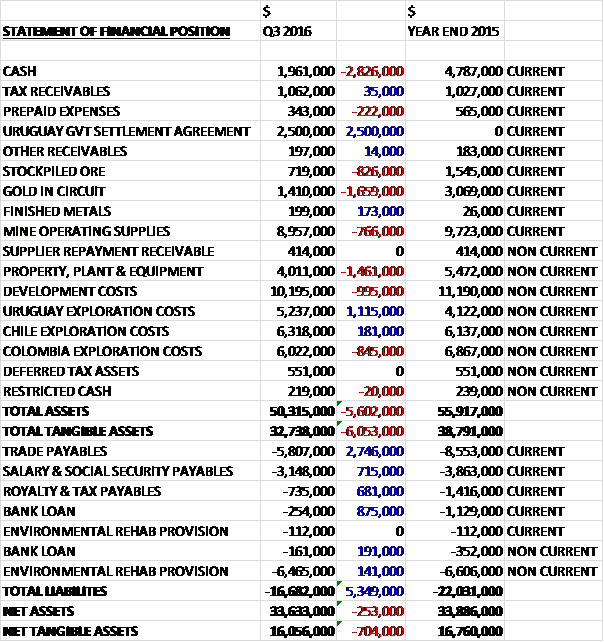

When compared to the end point of last year, total assets declined by $5.6M driven by a $2.9M decrease in cash, a $1.7M fall in gold in circuit, a $1.5M decline in property, plant and equipment, a $995K decrease in development costs and an $845K fall in Colombian exploration costs, partially offset by a $1.1M growth in Uruguay exploration costs and a $2.5M Uruguay government settlement agreement. Total liabilities also decreased during the period, mainly as a result of a $2.7M fall in trade payables and a $1.1M decline in the bank loan. The end result was a net tangible asset level of $16.1M, a decline of $704K over the past nine months.

When compared to Q3 last year, cash profits increased by $1.8M to $4.8M. There was a cash outflow through working capital, however, particularly due to an increase in receivables (probably the receivable from the government) and the cash from operations came in at $1.2M, a decline of $1.9M year on year. The group then spent $389K on property, plant and equipment, $491K on mine development and $618K on exploration expenditure to give a cash outflow of $316K before financing and after a $356K loan repayment the cash outflow was $672K and the cash level at the period-end was $2M.

During the quarter the group produced 7,274 ounces of gold, a decline of 6,486 ounces year on year and less than the 8,172 ounces produced in Q2 which means that year to date production of 27,917 was ahead of the company’s 30,000 to 35,000 ounce guidance for the full year. The average price received was $1,143, a decline of $77 per ounce, and the all in sustaining cost was $978 per ounce, a fall of $154 per ounce which was in line with expectations. The company is guiding towards costs below $1,000 per ounce for the rest of the year and between $1,000 and $1,100 for the full year.

In total, 194,197 tonnes of ore was processed at a grade of 1.25g per tonne with recoveries averaging at just under 94%. This compares to 305,609 tonnes at 1.47g/t for Q3 last year and 199,352 tonnes at a grade of 1.36g/t in Q2.

Permits for the San Gregorio Deeps were granted by the Uruguayan mining authority in February. The de-watering of the main pit of San Gregorio during the previous quarter allowed the company to mine about 1,500 ounces of gold from the pit during January and February, including some higher grade material from a north wall structure and some lower grade material located at the bottom of the pit.

During the quarter, an initial infill reverse circulation drilling campaign of 500m was undertaken from the main ramp of the open pit mine with the intention of further defining reserves and optimising mine design. The weighted average grade of the intercepts was 2.35g/t of gold over widths of about 4 to 14 metres. The company plans to complete a further infill drilling campaign of 5,000 metres from underground drilling stations as development progresses, in order to reduce costs, compared to drilling from the surface.

Following the implementation of the strategic plan to reduce costs in line with the gold price environment, a significant restructuring has been achieved and the economics of the San Gregorio Deeps have been updated, also assuming a reduced initial investment as the company plans to use the equipment from Arenal Deeps instead of purchasing new underground mining equipment. The company intends to dovetail the beginning of production in San Gregorio Deeps with the conclusion of operations at Arenal to facilitate these anticipated savings and plans for this to take place in 2017. To me it sounds likely that there might be a period of lower production while the transfer takes place – it seems a bit risky actually. Development work at San Gregorio is scheduled to start during the final quarter of this year.

An additional expected benefit of the revised plan is that San Gregorio will require no further external financing and is to be developed using cash from operations. At the end of the quarter the company started pre-stripping the relatively small Veta Rey open pit. The mine plan for this pit targets about 8,000 ounces of gold to me mined over the next six months. About 70% of waste rock will be allocated to the new tailings dam, decreasing costs of loading and hauling.

The group is currently focusing its brownfield exploration effort in Veta Rey and in Don Tito. Gold mineralisation in Don Tito is hosted in a hydro thermally altered granite and associated with quartz veining. Exploration work completed to date consists of six trenches, twelve drill holes and 65 pantera drill holes. Concurrently the group is advancing known target zones in Don Tito with the geophysics programme being ongoing during March and April with results expected during Q4. At Arenal Deeps, the group is testing a down-plunge extension of the Arenal mineralised structure. A 1,100m drilling campaign started in December and is expected to conclude during Q4.

In Chile, gold was encountered in the south and west sectors, opening up further exploration targets. The south and north gold-silver intersects are located in a north-south structural corridor, which appears to be the natural orientation for the mineralised veins in the district. Consistent anomalous silver values at the central north sector point to the possibility of an envelope of a potentially mineralised northwest structure. All the gold and silver encountered during drilling were intersects in silica/quartz-rich structures. As previously announced, the process of returning the Pantanillo properties to Anglo American continues.

In Anillo in Chile the phase 1 exploration was completed in December and included a geophysics campaign and an approximately 3,600 metres of reverse circulation drilling which took place over six months. Phase 2, if exercised, would include an additional geophysics campaign and a minimum of 5,500 metres of RC drilling and has an estimated duration of up to a year and a half.

On November, Minerales Cala gave notice to the company of the completion of its expenditures and reporting obligation with respect to phase 2 of the option agreement, thereby earning an additional 29% interest in the project for a total of 80% with Orosur retaining a 20% interest. Phase 3 of the option agreement has commenced and Minerales Cala is obliged to submit a detailed work programme and budget to the company.

As can be seen the group reached a settlement agreement with the government of Uruguay for $2.5M achieved through an administrative petition for repayment due to a custom benefit relating to the export of industrial goods which had been eliminated through a national decree in 2009. The company expects to receive the settlement proceeds during April this year which should come in handy.

The group has hedged a portion of their gold sales. They are committed to a forward contract of 3,500 ounces of their forecasted production in Q4, 1,400 ounces at $1,254 per ounce and 2,100 ounces at $1,260 per ounce in order to reduce their exposure to gold price fluctuations.

In January the group issued 2,103,894 shares to Pablo Marcet as termination consideration in connection with his resignation as their exploration and development director – he remains on the board so this seems a very good deal for him! The group also granted 2,920,000 options incurred $16K of compensation expense. Alejandra Lopez, current controller of Oroshur, has been promoted to interim CFO.

During the period the group has enjoyed an exemption on the royalty payment to the government (3% of sales) but this ended in March.

At the end of the period, the group had a net cash position of $1.5M compared to $3.3M at the end of last year. They have $3M of committed but undrawn lines of credit at the moment and an actual cash balance of $2M and should hopefully receive $2.5M from the Uruguay government imminently (although until they actually have this in their hands I’m not sure it can be counted on).

Overall then the group seems to be making progress. They made a profit this quarter, even when the tax settlement is excluded, as they focused on cost cutting. Net assets and the operating cash flow both declined, however, and there was no free cash generated. Less gold was produced during the period but it was ahead of the revised lower. The $1,143 per ounce received is not too bad and good progress has been made on costs, falling to $978 per ounce during the period.

It is worth noting that the price of gold is hovering around $1,245 at the moment and the group has hedged some production marginally above this price although it should also be noted that the royalty payment exemption has now ended so that will probably bring costs up towards $1,000 all else being equal.

Permits have been granted for SGD and some preliminary mining has begun with the grades looking OK. I am a little concerned about the transition from Arenal Deeps and the lack of any margin for error there. The group has $2M in cash and should be receiving $2.5M from the government any time now so there seems to be no immediate need for a cash call, and the board have stated no dilution will be necessary to get SGD into production.

It is an interesting situation here. The shares still no not look expensive and the fact that no share placings are expected is helpful. There are still risks here though, not least the transfer of production to SGD and the fact that they don’t really seem to have much in the way of actual reserves. Tricky. I am tempted to go for a little (risky) punt.