Plastics Capital is a UK based consolidator of plastics products manufacturers. They have five factories in the UK, one in Thailand, two in China and sales offices in the USA, Japan, India and China. The group has two divisions – industrial products and packaging products. Within industrial products there are two businesses. Bell Plastics manufactures hydraulic hose mandrels which are long, high-spec rods used by the manufacturers of industrial hoses; and high performance hose film with applications in construction, mining equipment and automotive. BNL designs and manufactures plastic bearings, assemblies and technical mouldings with applications in automotive, office machines, ATMs, security cameras and conveyors.

In the packaging division, C&T Matrix manufactures creasing matrixes, which is a consumable product used in the manufacture of cardboard boxes to facilitate accurate creasing prior to folding. Their products also include rubbers and printing accessories with applications for cardboard box manufacturers and point of sale products. Palagan is a manufacturer of high strength film packaging such as brown polyethylene films used in industrial packaging where high strength, tear and puncture resistance are requirements with applications in courier bags, asbestos bags, animal bedding bags and food packaging. The recently acquired Flexipol Packaging produces similar films to Palagan used in high strength specialist sacks, bags, liners and films with applications in food packaging and animal feed bags.

The company has now released its final results for the year ended 2015.

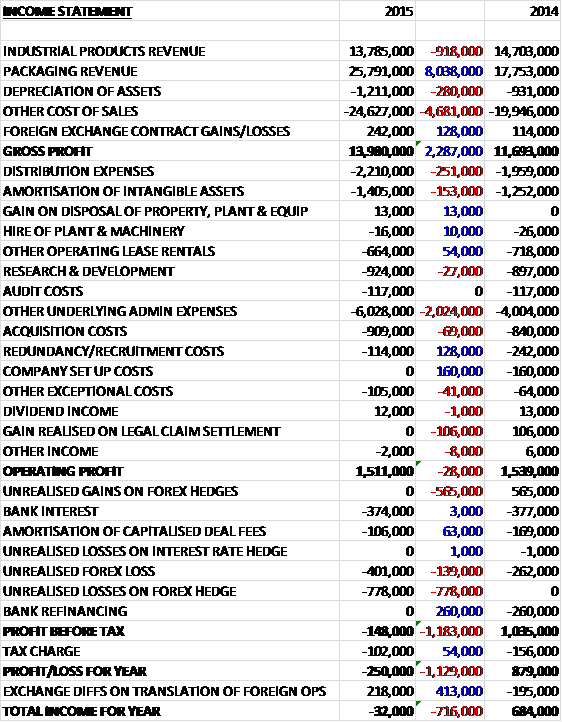

Revenues increased when compared to last year due to the Flexipol acquisition as a £918K fall in industrial product revenues was more than offset by an £8M growth in packaging revenue. Cost of sales also increased during the year and gross profit was £2.3M above that of last time. Distribution expenses were up slightly but admin costs grew by £2M which along with a few other costs meant that operating profit was broadly flat when compared to 2014, declining by £28K. We then see a £1.3M detrimental swing on the forex hedge which meant that, after the lack of the bank refinancing charge that occurred last year and a slightly lower tax charge, the loss for the year was £251K, a detrimental movement of £1.1M year on year.

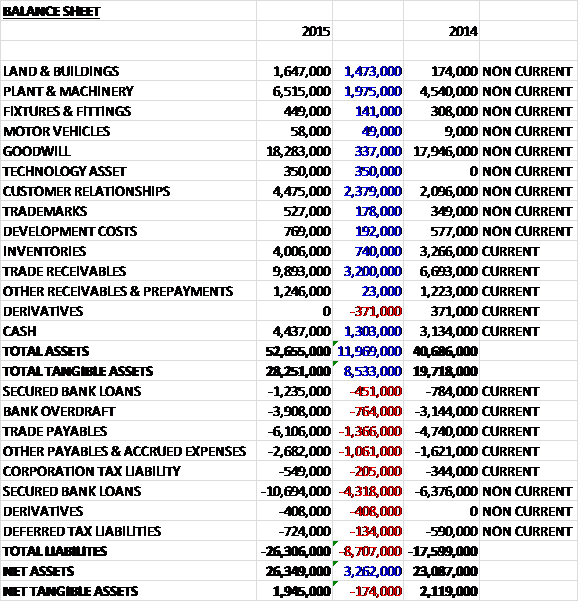

When compared to the end point of last year, total assets increased by £12M driven by a £3.2M growth in trade receivables, a £2.4M increase in customer relationships, a £2M growth in plant and machinery, a £1.5M increase in land and buildings, and a £1.3M growth in cash. Total liabilities also increased during the year due to a £4.8M growth on bank loans, a £1.4M increase in trade payables and a £1M increase in other payables. The end result is a net tangible asset level of £1.9M, a decline of £174K year on year.

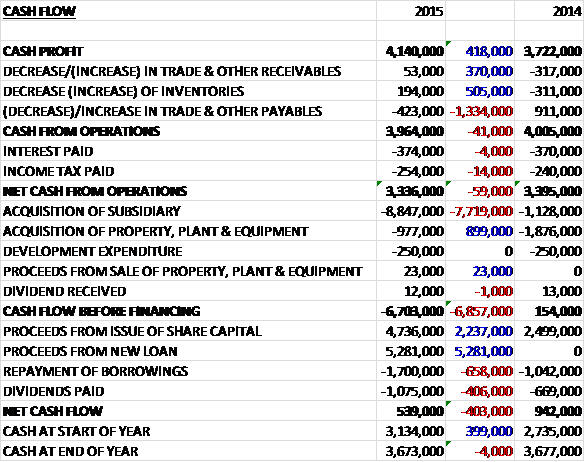

Before movements in working capital, cash profits increased by £418K to £4.1M. There was a small outflow from working capital due to a fall in payables and a modest increase in tax so that the net cash from operations was £3.3M, a decline of £59K year on year. This covered the £977K paid on fixed assets and £250K of development expenditure (capital expenditure is expected to increase somewhat going forward) but not the £8.8M spent on the acquisition so before financing there was a cash outflow of £6.7M. There was a net £3.6M of new loans to pay for this, along with £4.7M from the issue of new shares so that after a £1.1M spend on dividends, which the group can’t really afford, the cash flow for the year was £539K to give a cash level of £3.7M at the year-end. I am not sure what the logic is in conducting a new share placing and paying out dividends at the same time.

The recent acquisitions enabled turnover to grow by 22% for the year but although organic growth has improved significantly, overall it has been disappointing. The mandrel business was unable to sustain the 39% increase in sales that it had achieved in the prior year and sales fell back by 21% year on year. In bearings, H2 saw a significant improvement over H1 as projects which had been delayed went into production and they finished slightly ahead for the year after adjusting for foreign exchange movements. In the Packaging division, creasing matrix volumes increased 7% and retained sales in industrial packaging films were flat. On a pro-forma basis including a full year of Flexipol, organic growth of industrial packaging film sales was up 3.4%.

The pre-tax loss in the Industrial Products division was £528K, a detrimental movement of £835K year on year. Bell Plastics, who manufacture hose mandrels and films had a weak year after an exceptional prior year with sales falling by 21%. Demand was adversely affected by lower demand in the oil, gas and mining sectors with new business won in the last year slow to turn into re-orders and ongoing demand being generally weak. Operationally, capacity expanded by 30% as faster line speeds were phased in through the year and all lines were fully automated. In addition, new materials were added to widen the range of products available such as the introduction of standard and flexible grades of polypropylene using faster line speeds which has enabled the business to target new segments of the hose market.

The board believe that pipeline prospects for the business are excellent and they have started to see conversion of the pipeline during the first quarter of the current year despite the fact that the market generally remains subdued. Whilst the volatility of this business is inherent to the markets it serves, they believe that over the long term they will achieve the 10% annual growth that has been evident over the last five years.

BNL, which manufactures plastic bearings and other rotating parts, saw sales improve significantly during the year as new projects and some recurring businesses came through in the second half of the year. Some excellent new project wins were also secured with important new key accounts such as bearings for two tier one steering column manufacturers, four projects for different CCTV manufacturers in China and the first project with a major Japanese document management company.

Operational performance has been good. The Thailand factory has continued to increase in importance and standards there have improved. All major customer audits during the year were passed and new tooling designs have been progressed so they no longer represent a major bottleneck in the conversion process. The new business pipeline at BNL remains at £3.5M and this business is expected to flow through over the next three years. Meanwhile the list of projects which have not yet been converted but for which prototypes have been produced and are under test is substantial and would produce another £3.8M annual sales if it all converted – historically though there has been a 55% conversion rate.

The pre-tax profit in the Packaging division was £1.6M, about double that of last year. C&T Matrix, which manufactures creasing matrix, a consumable used by packaging manufacturers to crease cardboard, increased sales by 2% which included a 7% increase in high margin matrix volumes, a 24% increase in ejection rubber and a decrease in low margin traded accessories. The growth in matrix was driven by new product introduction and through growth in key developing markets like Brazil, Mexico and India. The growth in volumes but some strain on the business’ operations in the first part of the year. Management then made some progress on fully implementing a new planning system and on improving machine speeds and efficiencies without compromising quality and gradually, over the course of the year, performance improved and overtime costs were nearly eliminated.

The integration of Shengli into the business has proceeded well and the group are now harmonising product ranges and consolidating sales activity where it makes sense. Shengli products are now represented by the C&T sales team outside China with the reverse applying within the country. The run rate of production and commercial synergies is about £100K per annum which is expected to increase over the next year. C&T’s future growth will be based on organic development in emerging markets and potentially through bolt on acquisitions in developed countries, which may broaden the range of die-making and die-cutting consumables made available to end users.

Palagan, the industrial film packaging business, had a mixed year with flat volumes but significant margin growth, mainly as a result of the fall in raw material prices during the second half. Operational performance was good with improvements on the prior year in terms of scrap rates, returns and operating efficiencies.

The recently acquired Flexipol packaging business has provided a number of opportunities for growth and profit improvement and serves the same broad industrial packaging markets as Palagan but with different product ranges. Cost saving opportunities include raw material purchases, energy and transportation. In terms of cross-selling, both businesses can now offer a fuller range of products to their customers and annual run-rate margin improvements to date are about £300K. The board see excellent opportunities to grow organically in this division. Capacity expansion is planned at Flexipol to enable the business to develop the sales of its specialist products to new accounts and to manufacture some new high strength products and further sales resources are being added. In addition there are opportunities for complementary acquisitions in this area which the board have started to explore.

The group has been targeting key account wins in the Industrial division. In the second half of the year the projects pipeline in the bearings business has started to convert and the board hope to see this increase over the next two years. Tool orders for steering column bearings have been won from two new important tier one automotive customers and they now have tool orders from four CCTV camera manufacturers in China. In mandrels, the slump in the oil and gas and mining sectors affected demand and no new accounts were converted during the year. After the period end, however, they achieved the conversion of three important mandrel accounts. Another 15 active prospects remain in the pipeline and management are optimistic about this business returning to growth in the new year.

Commodity raw material prices edged downwards during the first half of the year and then declined by 20-25% during the second half. These polymer prices are somewhat linked to oil prices which had then declined sharply. This has the effect of temporarily improving margins in the industrial firms division during Q4 and contributed 3-4% of EBITDA for the year. Raw materials have increased sharply since the year-end, however, as polymer manufacturers have reduced capacity largely because of unplanned plant shutdowns. It is anticipated that greater that greater stability will return to raw material prices during Q2 2016. Engineering plastic prices have been largely unaffected but the group are aware of some shortages in certain types of material.

The group’s strategy is to achieve greater than 5% annual turnover growth by organic means and to augment this with acquisitions. This organic growth target has eluded them over recent years, however, and they have spent some time assessing the reasons for this. The board remain convinced that this level of growth is achievable in their businesses provided they focus on key customers, technical service and incremental product innovation. They have identified the need to be more disciplined in resource allocation, implementation follow through and project management of key initiatives and consequently have put in place a number of actions across the group to address these issues.

Capital expenditure fell somewhat this year as the prior year saw significant investment which included additional capacity to the industrial films business through the installation of a new extrusion line and tool room investment at the bearing business which was completely upgraded as part of an initiative to improve conversion speed of projects.

The group are somewhat susceptible to interest rate hikes. If they were to increase to 4% from the current 0.5%, the interest charge would increase by £447K. The group’s policy is to hedge 100% of its anticipated net cash flows in US dollars for the subsequent year and a half but a 10% strengthening of Sterling against the dollar wold have an adverse effect of £589K while a similar change against the Euro would reduce profits by £267K.

In November 2014 the group acquired Flexipol Packaging, a manufacturer of films and industrial bags primarily for the food and animal feed sectors, for a total consideration of £10.2M consisting of £9.8M in cash and £410K in contingent consideration. The acquisition generated goodwill of just £337K with a further £4.1M of intangible assets. In the four or so months since the acquisition the business generated a profit of £682K which is a remarkable return really and this looks to be a very useful acquisition indeed to me. Since the acquisition, the business has performed very well with all key accounts being retained and additional business being secured in a number of areas.

Flexipol more than doubles the size of the group’s films business and means that 55% of sales now come from this area. Last year the group acquired Shengli in China which has enabled them to develop their bearings and mandrels business there and to achieve a leadership position in creasing matrix. Integration has gone according to plan with a number of product synergies achieved and consolidation of sales and distribution activities are in progress.

As far as further acquisitions are concerned, the group have a good list of target companies with whom they have ongoing discussions. Most would fit alongside their existing businesses and be complementary, or would be integrated into their current businesses to create a stronger global player.

Following the year-end, the group undertook a sale and leaseback of the Flexipol property which realised cash of £1.4M. Unless they are desperate for cash, I would rather not see sale and leasebacks as I think owning their own property would mean the company has extra asset backing and flexibility going forward, not to mention the operating lease payments that they will have to make now they no longer own it.

Trading in the current year is in line with management’s expectations. Compared to the prior year, trading is weaker in the packaging division but stronger in the industrial division where the operational gearing is greater. The pipeline of new business remains strong and the board are aware that converting it into sales is key to performance this year. Although they are optimistic about this, they apparently have to recognise that the outlook for new business wins is always uncertain (covering themselves somewhat here I think). In contrast, customer retention remains very good.

At the current share price the shares are yielding 3.7% which increases to 4.3% on next year’s consensus forecast. As the group made a loss this year, we cannot determine a PE ratio but on next year’s forecast it currently stands at 9.5 which looks rather cheap. The net debt at the year-end of £11.4M increased by £4.2M over the year.

Overall then this has been a mixed year for the group. Profits fell, seemingly due to the forex revaluations (presumably offset by helpful movements elsewhere) but operating profit was flat. Net tangible assets declined and the balance sheet does not look that great, and operating cash flow was flat due to a fall in payables – cash profits increased year on year but there is little free cash generated and the group had to issue more shares to make the acquisition, which is not great to see. Operationally, the Industrial sector is loss making, mainly as a result of a collapse in Mandrel sales due to the oil and gas end markets being very weak. Packaging profits increased, mainly as a result of the Flexipol acquisition but the lower raw material prices improved profits at Palagon too.

The Flexipol acquisition does look like a very good one but the company can’t really afford it, I would much rather see company’s make acquisitions out of their own reserves and perhaps a bit of extra debt but debt here is already very high, hence the share issue I guess. It is a little concerning to see the board seem intent on making further acquisitions. Unfortunately, since the year-end, polymer raw material prices have increased which will put a pinch on margins and the group remains susceptible to interest rate increases and forex movements. They readily admit that they find organic growth difficult, and this really has to change before these shares become in demand I think.

The new year has been mixed with an improvement in industrial products but a less successful start in packaging. With a forward PE of 9.5 and a dividend yield of 4.3% these shares look cheap but there is a lot of debt to take into account and before some of the other problems are sorted out, I would expect the shares to remain cheap. Not for me at the moment.

On the 2nd October the group released the details of the new LTIP to run from 2015 to 2020. The plan involves the issue of special classes of shares known as “growth shares” in an intermediate holding company. They will be exchanged for a certain number of new ordinary shares in the company at the end of the LTIP five year period, based on the share price at the end of this period subject to financial performance and vesting criteria being met.

For any of the growth shares to be exchanged for normal shares, the share price at the end of the period must be about £1.50 per share, representing a 40% uplift to the current share price. The total value of the growth shares at the end of the five year performance period will equate to 20% of the increase in share price above this £1.50 hurdle, multiplied by the number of ordinary shares in issue at the start of the scheme (35,344,573). The value of will be capped, however, so that shareholders cannot be diluted by more than 10%.

I have mixed feelings over this. The hurdle (if it remains in place) does offer some decent upside to the shares but it is not all that ambitious and giving away 10% of the company to directors for doing their job leaves me with a rather sour feeling about all of this – it does appear rather greedy to me.