Following the acquisition of Flexipol, the board have now reclassified the group into two operating divisions: Films, which includes Palagan and Flexipol; and Industrial which includes BNL, Bell and C&T Matrix. The films businesses operate substantially in the UK market for high strength film packaging whereas BNL, Bell and C&T Matrix each make and sell engineered plastics products on a global basis. Plastics Capital has now released its interim results for the year ending 2016.

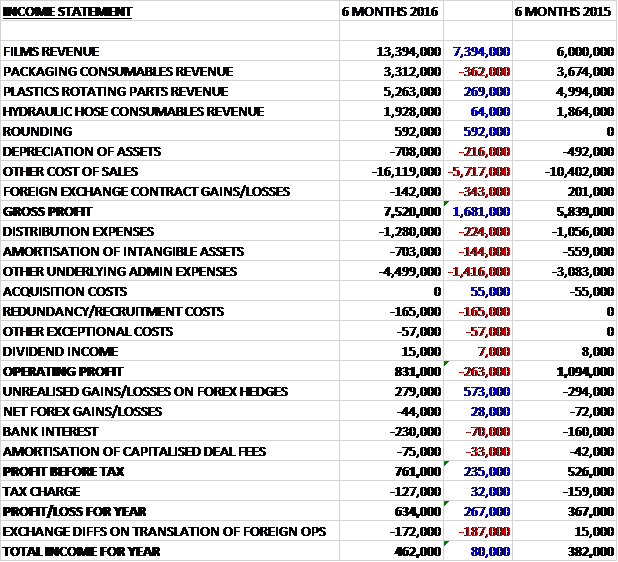

Revenues increased when compared to last year as a £362K fall in packaging consumable revenue was more than offset by a £7.4M growth in films revenue, a £269K increase in plastics rotating parts revenue and a £64K growth in hydraulic hose consumable revenues. Depreciation was up slightly, and there was a £343K adverse movement in foreign exchange contracts, along with a growth in other cost of sales which meant that gross profit was some £1.7M higher than last year. Distribution expenses were up £224K, amortisation increased by £144K and other admin costs grew by £1.4M and we also see £165K of redundancy costs and £57K of other exceptional costs which gave an operating profit which was £263K below that of the first half of last year. We then see a £573K positive swing in unrealised gains in forex hedges which meant that the profit for the half year came in at £634K, a growth of £267K year on year.

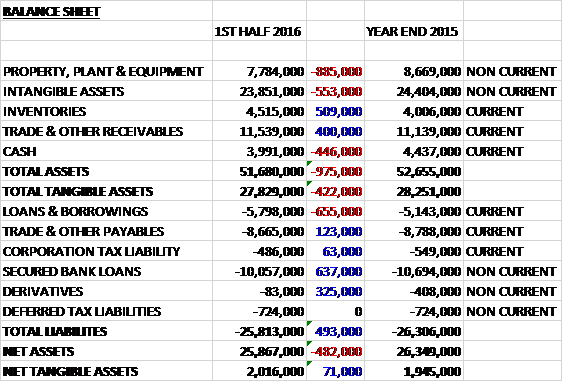

When compared to the end point of last year, total assets fell by £975K driven by an £885K decline in property, plant & equipment, a £553K fall in intangible assets and a £446K decrease in cash, partially offset by a £509K growth in inventories and a £400K increase in receivables. Total liabilities also declined during the six month period due to a £325K fall in derivative liabilities and a £123K decrease in payables. The end result is a net tangible asset level of £2M, an increase of just £71K over the half year period.

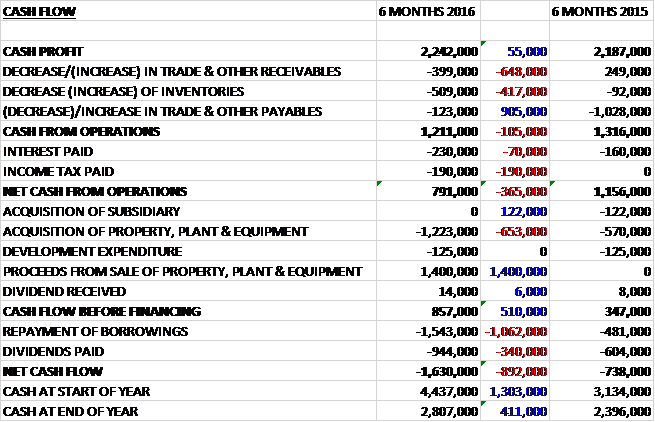

Before movements in working capital, cash profits were broadly flat, increasing by just £55K. An increase in both receivables and inventories, plus a £70K increase in interest payments and a £190K tax payment meant that the net cash from operations for the six month period was £791K, a decline of £365K year on year. This did not cover capital expenditure of £1.2M property, plant & equipment along with £125K of development expenditure but the £1.4M of proceeds from the sale and lease back meant that before financing there was an £857K cash inflow. This did not cover the £944K of dividends and there was also a £1.5M repayment of borrowings to give a cash flow of £1.6M and a cash level of £2.8M at the period-end.

I notice the group is now stating an EBTDA figure at constant exchange rates and polymer prices! I have heard it all now, it seems fairly common for companies to quote earnings at constant currency rates, particularly if there has been a detrimental movement, but I think it is a bit much to assume a constant raw material price! Why not just have done with it and quote a constant sales price and volume too?

The pre-tax loss in the Industrial division was £124K, a detrimental movement of £347K year on year with the decline being blamed on foreign exchange movements as profits on a constant currency basis were broadly flat. Sales have improved in the bearings business, increasing by 5% year on year, partly due to prior period new project wins flowing through into increased production as well as the development of important key accounts in the swimming pool cleaner and poultry processing industries. The mandrel business has seen sales that were flat year on year as new business wins offset softer end markets.

The pre-tax profit in the films division was £223K, an increase of £51K when compared to the first half of last year. These results include the first full half-year contribution from Flexipol, which has performed ahead of original expectations so organic profits seem to have fallen. The board have also started the process of identifying and implementing synergies between Palagan and Flexipol and anticipate that this will deliver over £500K of incremental annual operating profit over the next year and a half as both cost savings and additional sales flow through. Profitability in the period was negatively affected by the increase in raw material prices following the substantial fall in polymer prices in Q4 2015 but raw material prices have now stabilised.

There are a number of initiatives that the board believe will help with their target of doubling EBITDA over the next five years. In the films division, these include expanding the sales of specialist patented products which has involved the addition of 850 tonnes of additional capacity installed during the period and the appointment of a new sales person – the expected additional sales are apparently already coming through; the introduction of a new ultra-high strength wide width range of films with a new conversion line being installed in the second half of the year; and cross selling between the two businesses.

In the industrial division, these initiatives include: bringing already won bearings business successfully into production with the current pipeline that has been won but not yet being produced standing at £4.3M per annum which should come through over the next five years; building on the investment made so far in China where the sales teams have identified a number of bearings and mandrels opportunities with extra products expected to hit the market next year; increasing the mandrel business development resource with additional sales and R&D resources being recruited; and forward integration in matrix where there is an opportunity to increase profits by getting closer to box makers through investment in distributors.

As the board have pointed out, there are risks involved with some of these initiatives with the possibility of customer delays and unforeseen technical issues. Customer loses is also a factor that they have made allowances for and they continue to run the risk of a downturn in the global economy as this new investment comes on stream.

The board have stated that a number of good acquisition opportunities have presented themselves over the past six months and they remain enthusiastic to add businesses to the group and are hopeful to bring at least one to fruition over the next year or so – I am not sure where they are going to find the cash to do that, but I suspect this is the only way they are going to increase EBITDA by the amount they are looking for.

Apparently the order books in both businesses are strong and the board anticipate a significantly improved performance in the second half of the year which means that they expect to trade in line with expectations for the year as a whole. Unfortunately most of the analysts do not agree and have cut their targets for earnings and dividends.

At the end of the period, net debt stood at £11.9M, an increase of 48% year on year. After a 9.8% increase in the interim dividend, the shares now yield 3.8%, increasing to 4% on the full year forecast – but these are shareholder returns that the group can’t really afford in my view. The forward PE now stands at 9.8 after some reductions in the consensus forecast for the year as a whole.

Overall then, this has been another half year where the group doesn’t seem to have made much progress. Profits were up due to unrealised gains on the forex hedges – operating profit fell. Net tangible assets were broadly flat and fairly low and cash profits were equally flat with a reduction in operating cash flows due to a cash outflow from working capital and a higher tax payment. There was a swing to losses in the industrial division which is being blamed entirely on foreign exchange losses and the films profits increased due to the previous Flexipol acquisition – organic growth seems to have been non-existent (as usual).

There are some investment initiatives to remedy the ongoing situation here where the group never seem to be able to make any organic growth and the board expect a better performance in the second half of the year. With a forward PE ratio of 9.8 and dividend yield of 4%, the shares do look cheap but debt is still rather high and I am not sure whether I believe that a recovery really will occur in H2. This is one I am not interested in at the moment.

On the 15th February the group released a trading update where they stated that they were trading “broadly” in line with market expectations, which in proper English I assume means trading slightly below. Revenues showed a significant improvement over H1 with strong trading in the Films division being offset by poorer trading conditions in the Industrial division. Product gross margins have been mostly unaffected by these poor conditions, however, with the group’s operating profit margin continuing to improve as the year progresses.

The Films division has made good progress on its key initiatives over the year. The group have added about 1,000 tonnes of new capacity, representing about 8% of annualised installed capacity, and this has now been fully utilised through new business growth in specialist sacks for food manufacturing and distribution customers. Three significant new product initiatives are in the process of final development for introduction during the next year, including one for which a patent has been registered. Synergies across Flexipol and Palagan are progressing in line with expectations and should lead to reduced costs in a number of areas which should become increasingly noticeable over the next year.

In the Industrials division, the bearings business is trading as expected, reflecting gradual improvement over the prior year. Conversion of won projects into sales continues to advance but this remains a little slower than anticipated. New product activity is strong and they have some substantial potential projects in the automotive and home appliance sectors that are progressing well and the board hope to sign these in the near future.

Matrix activities continue to be affected by the downturn in emerging markets, although there is some evidence that destocking in the distributor network, evident over the past year, is coming to an end. More encouragingly, the business is making good progress in markets where they have direct control over sales such as the UK and India, and where they work closely with distributors in providing value added technical services to end users.

Demand weakness in mandrels has been somewhat more significant than expected, but they continue to win new business in the area. This new business is not fully compensating for the underlying weak trading conditions. Most significantly, they have converted their first local key account in China, which has a substantial industry manufacturing hydraulic, automotive and industrial rubber hose, most of which is supplied by local Chinese manufacturers using inferior mandrel types. Over the past two years the group has established sales and technical services for mandrels in Shanghai and have a large list of target accounts who are testing their products. This first conversion is with a leading rubber hose manufacturer and is one which they believe will lead to further conversions in due course.

Trading conditions remain somewhat variable reflecting global economic conditions, but financial performance in improving and overall the board anticipate that performance over the second half of the financial year will be broadly in line with market expectations. Despite this, however, I am trying to rationalise the number of companies I cover and this one, given the debt levels and variable trading doesn’t make the cut at the moment – I might revisit if debt is paid down a bit.

On the 28th September the group released a trading update where they stated that they traded in line with market expectations. Trading in the past six month period saw an improvement on the prior year, primarily due to organic sales growth in the industrial division and the initial contribution from Synpac in the Films Division, which was acquired in July 2016.

In the industrial division, sales at the bearings business continued to improve due to previously won projects that are now starting to ramp-up after some initial delays. The pipeline of business won but still to go into production remains strong, as does the pipeline of projects in prototype development and testing. In addition, this business is being assisted by the weakness of sterling against the US dollar, although the benefit of this is not expected to be seen materially until 2018.

Demand at the matrix business is also improving relative to last year. This is partially as a result of stock depletion during the prior year by some distributors in emerging markets but also the result of strong sales of C&T Matrix’s broadening range of matrix products and other consumables. Mandrel sales have also grown relative to the prior year, the order book is strong and the list of customers undergoing trials is extensive which suggests that sales should progress well in the second half of the year.

Sales have also increased across the films division. Flexipol continues to trade well and has a healthy order book as it moves into the busy time of its year. The project to install a new extruder to provide an additional 2,500 tonnes of capacity over the next three years is on track for completion by the year-end. Palagan’s performance has suffered a little while it makes changes to shift patterns, account management and product development whilst Synpac which joined the group in mid-July is trading in line with expectations.

Overall then this seems like a positive update so the half year results should make interesting reading, hopefully some progress has been made on their debt situation.