Solid State has now released their interim results for the year ending 2020.

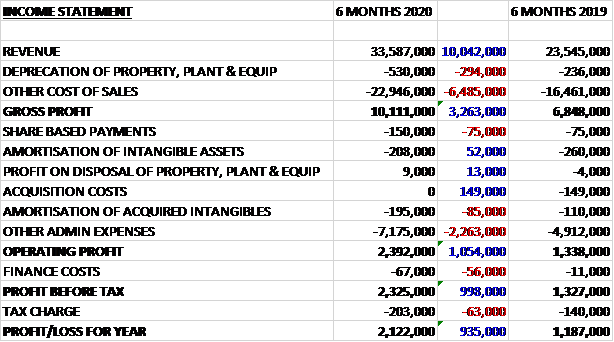

Revenues increased by £10M when compared to the first half of last year and after cost of sales also increased, the gross profit was £3.3M higher. Amortisation fell by £52K and acquisition costs were down £149K but share based payments were up £75K, amortisation of acquired intangibles increased by £85K and other admin expenses grew by £2.3M to give an operating profit £1.1M higher. Finance costs increased by £56K and tax charges were up £63K which meant that the profit for the period was £2.1M, a growth of £935K year on year.

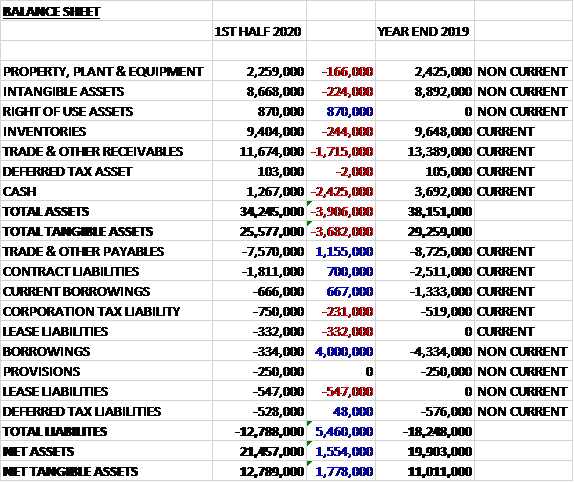

When compared to the end point of last year, total assets declined by £3.7M, driven by a £2.4M fall in cash, and a £1.7M decrease in receivables, partially offset by an £870K right of use asset. Total liabilities also declined during the period due to a £4.7M fall in borrowings, a £1.2M decrease in payables, and a £700K fall in contract liabilities. The end result was a net tangible asset level of £12.8M, a growth of £1.8M over the past six months.

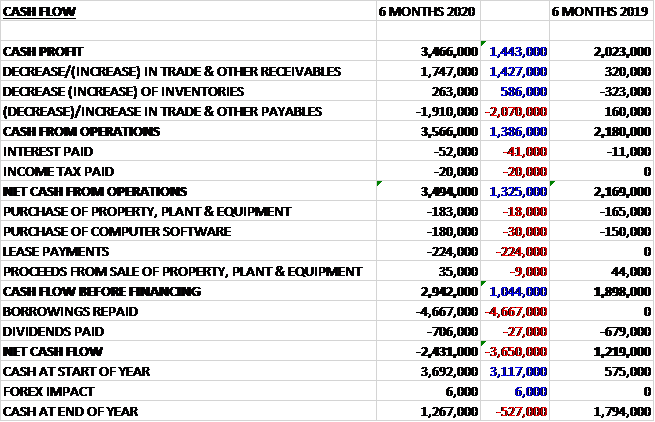

Before movements in working capital, cash profits increased by £1.4M to £3.5M. There was a modest cash inflow from working capital and interest payments increased slightly to give a net cash from operations of £4M, an increase of £1.3M. The group spent £183K on property, plant and equipment, £180K on computer software and £224K on lease payments to give a free cash flow of £2.9M. They then spent £706K on dividends and repaid £4.7M of debt which gave a cash outflow of £2.4M and a cash level of £1.3M.

Trading in the period benefitted from favourable currency movements and the acceleration of certain strong margin project work that had been expected in the second half so the full year results are expected to be first half weighted. Although the macro-economic environment remains very challenging, current trading since the period-end has continued in line with management expectations. Prospects for the rest of the year are underpinned by the solid open order book and the resilience and diversity of the group.

The manufacturing division saw organic revenue growth of 22% with first half billings particularly strong in the Power business unit. The continued focus on delivering high value solutions has resulted in a favourable mix of sales. The focus on marketing is delivering an increase in quality lead generation to support the focused sales activities and the improved utilisation of their facilities leverages the operational gearing which has delivered an improvement in profitability. They completed the commissioning of the environmental test equipment at the Leominster facility allowing the pre compliance testing of products from across the group. They are now looking to strengthen their attenuation and electromagnetic compatibility testing capability at the Redditch facility.

The Distribution division traded well with revenues increasing by £7.5M, mainly as a result of the contribution from the Pacer acquisition. Like for like revenues were up 4% with the electronics business flat and the opto-electronics business growing by 11%. This significantly expanded their services which now includes a sub module optical assembly alongside class 7 clean room facilities in Weymouth. In July it was announced that they secured the enlarged Microship franchise. They have already seen their first billings of Microchip product and this is expected to impact order intake in the second half.

At the current share price the shares are trading on a PE ratio of 21 which falls to 15.5 on the full year forecast. After a 25% increase in the interim dividend the shares are yielding 2.1% which increases to 2.4% on the full year forecast. At the period-end the group had a net cash position of £300K compared to £1.9M at the year-end.

Overall then this has been a strong period for the group. Profits were up, net assets increased and the operating cash flow grew with a good amount of free cash being generated. The group has benefited from favourable currency movements and the pull forward of some orders, however, and the second half is not expected to be as strong. That being said, trading seems to be OK, although the forward PE of 15.5 and yield of 2.4% isn’t entirely that cheap.

On the 16th January the group announced that CEO Gary Marsh sold 16,000 shares at a value of just over £100K. He still owns 280,795 shares.