The Property Franchise Group has now released their final results for the year ended 2016.

Revenues increased when compared to last year with a £684K growth in management service fees, a £96K increase in franchise sales and a £391K growth in other revenue. Cost of sales was also up to give a gross profit £956K above last time. Property costs declined by £69K but employee costs were up £39K, amortisation increased by £86K, audit costs grew by £85K and other admin expenses increased by £204K. We also see a £150K increase in acquisition costs partially offset by a £61K decline in redundancy costs to give an operating profit £531K above last time. We also see a £30K unwinding of the discount on deferred income and a £341K decrease in tax charges due to tax relief on share based payments and the effect of a change in the rate used for deferred tax, to give a profit for the year of £3M, a growth of £840K year on year.

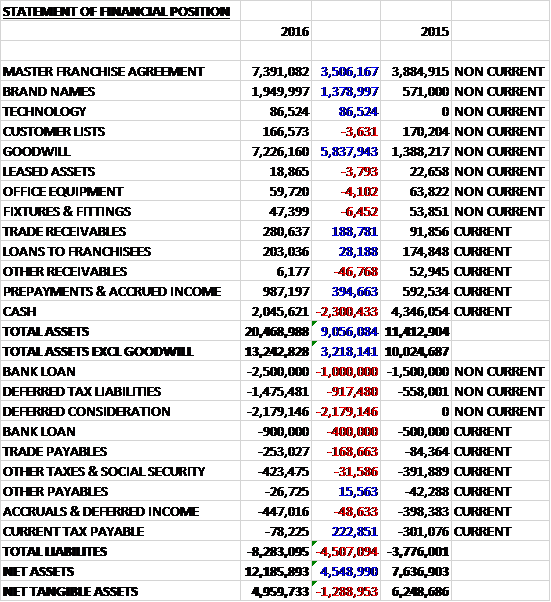

When compared to the end point of last year, total assets increased by £9.1M driven by a £5.8M growth in goodwill, a £3.5M increase in the value of the master franchise agreement and a £1.4M growth in the value of brand names. Total liabilities also increased during the year due to a £2.2M growth in deferred consideration, a £1.4M increase in the bank loan and a £917K growth in deferred tax liabilities. If we exclude goodwill (I am attributing face value to the master franchise agreement which I am slightly torn over) the net tangible asset level is £5M, a decline of £1.3M year on year.

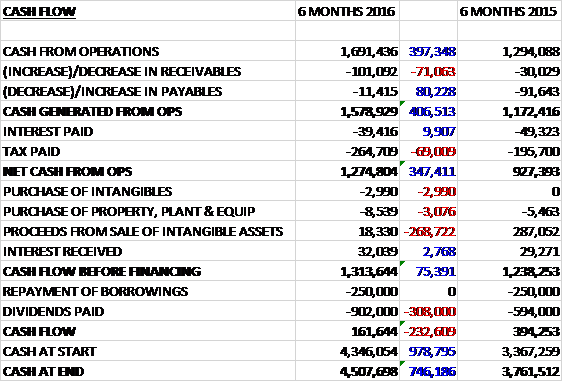

Before movements in working capital, cash profits increased by £619K. There was a cash outflow from working capital movements but tax and interest both saw modest declines to give a net cash from operations of £2.4M, a growth of £211K year on year. The group spent £92K on intangibles along with just £14K on fixed tangible assets but also spent £4.8M on acquisitions so there was a cash outflow of £2.5M before financing. They took out a net £1.4M of new loans which paid for the £1.4M of dividends and the cash outflow for the year was £2.3M and the cash level at the year-end was £2M.

There were a number of headwinds for the housing market this year from tax changes and uncertainty surrounding Brexit. The additional rate of stamp duty on second homes and buy to let purchases for individuals had the effect of a rush to complete transactions before April 2016 which resulted in a surge in group sales in March followed by a comparatively quieter period. Summer uncertainty around the Brexit vote appeared to undermine consumer confidence and instruction levels fell for both sales and lettings before recovering in Q4.

In the autumn the government announced its intention to limit or ban tenant fees in England. At the time of writing the timetable and extent of any ban remains unclear. In Scotland, where a ban has existed since 2012, the experience has been that the impact on revenues were mitigated in just over a year.

Management service fees increased by 11% with lettings fees up 9% and sales fees increasing by 19%. The Xperience business delivered £1M of earnings. The brands were tilted 54% to 46% estate agency over lettings revenue and the group looked to increase its lettings income stream which now stands at 46% 54% respectively. Lettings revenue grew by 12% compared to 4% in the traditional Martin and Co business.

The group rolled out financial services to 2/3 of their traditional brand offices during the year. The proposition is a selection of mortgages and fee-free advice from partner London and Coventry whilst general insurance products will be tied to Legal and General which should add another revenue stream.

In September the group acquired Ewemove Sales and Lettings for a consideration of £5M in cash and £3M in shares. A further amount of up to £7M is due in 2018 subject to various targets. The acquisition generated goodwill of £5.8M. The board had observed a shift in the estate agency sector with the growth of online agents which don’t have physical premises and adopt pricing models based on listing fees rather than completions. They decided to acquire an operator rather than build their own. Following the acquisition the business contributed a profit of £100K. After the year-end the group announced that the deferred consideration payable to the founders of ESLL had been renegotiated to two cash payments of £500K in 2017.

The group have a clear brand strategy. Martin and Co is the national lettings brand; Ellis & Co, Parkers, CJ Hole and Whitegates are regional brands with a particular expertise in estate agency services and EweMove is the challenger brand.

At the current share price the shares trade on a PE ratio of 12 which falls to 10.3 on next year’s consensus forecast. After a 10% increase in the dividend the shares are yielding 4.2% which increases to 5.3% on next year’s forecast.

Overall then this has been a pretty decent year for the group. Profits and the operating cash flow both grew, although after the acquisition there was no free cash and the net tangible asset level declined due to the acquisition. There are various headwinds affecting the sector and the potential ban on tenant fees could affect income quite a bit. The Ewemove acquisition looks quite expensive but it is probably a good move to acquire a challenger brand with the way the market is going and I think the forward PE of 10.3 and yield of 5.3% adequately cover the risk. I am a holder.

On the 9th May the group released a trading update for Q1. The trading performance has been robust with like for like revenue increasing 4%. Management Service fees were unchanged with a growth in lettings of 7% offset by a 19% fall in sales due to a rush to complete transactions ahead of stamp duty changes in Q1 2016. EweMove has grown its revenue by 14% and its total number of franchise stands at 108.

The board have not seen any evidence that landlords are disposing of stock in increasing numbers. Their traditional brands have more than 400 more properties to let than at this point of 2016 and the tenanted managed portfolio across the whole group is up from 48,000 at the year-end to 49,000 at the end of the quarter. Against this backdrop, they are confident of delivering a performance in line with market expectations.