The Property Franchise group have now released their final results for the year ended 2017.

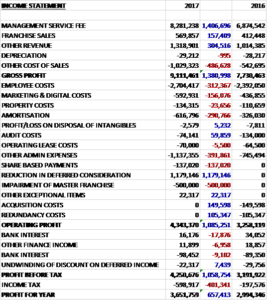

Revenues increased when compared to last year due to a £1.4M growth in management service fees, a £157K increase in franchise sales and a £305K growth in other revenue. Costs of sales increased by £487K so gross profit was £1.4m higher. Employee costs were up £312K, marketing and digital costs increased by £156K, and amortisation grew by £290K. There was £60K less spent on audit services this year but other admin expenses were up £392K. Share based payments were up £137K and there was a £500K impairment of the master franchise agreement but also a £1.2M reduction in deferred consideration, a £150K fall in acquisition costs and a £105K decrease in redundancy costs to give an operating profit £1.1M higher. We see a modest increase in interest costs and a £401K growth in tax charges which gives a profit for the year of £3.7M, an increase of £657K year on year.

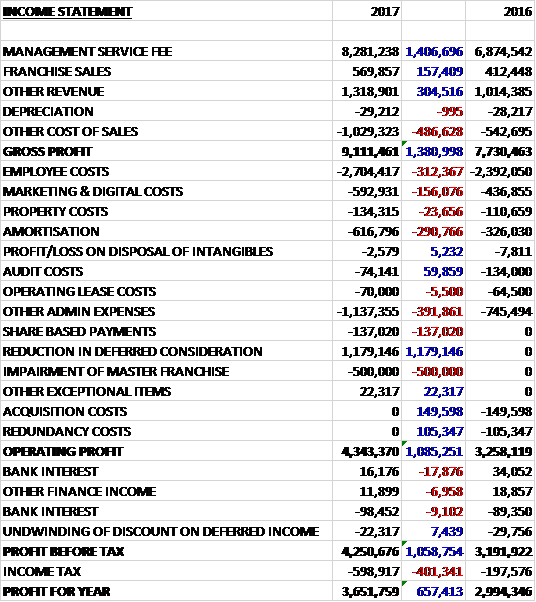

When compared to the end point of last year, total assets declined by £433K, driven by a £913K impairment of the master franchise agreement, a £164K fall in loans to franchisees and a £143K decrease in trade receivables, partially offset by a £549K increase in cash, a £196K growth in the value of customer lists and a £169K increase in technology relating to new websites. Total liabilities also decreased during the period as a £149K increase in other taxes and social security and a £414K growth in current tax payables were more than offset by a £2.2M decrease in deferred consideration and a £900K fall in the bank loan. The end result was a net tangible asset level of £7M, an increase of £2.1M year on year.

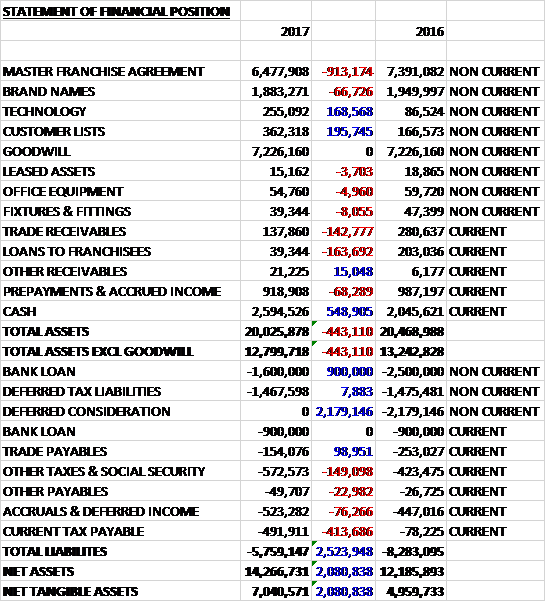

Before movements in working capital, cash profits increased by £807K to £4.4M. There was a cash inflow from working capital and after tax payments fell by £306K the net cash from operations was £4.4M, an increase of £2.1M year on year. The group spent £1M on acquisitions and £402K on intangible assets to give a free cash flow of £3.1M. Of this, £900K was used to pay off some of the loan and £1.7M was paid out in dividends which gave a cash flow of £549K and a cash level of £2.6M at the year-end.

The acquisition of EweMove delivered significant revenue growth and provided them with the digital marketing insight to leverage better performance in the traditional high street brands with all brands increasing revenues year on year. EweMove itself incurred losses in the first half of the year but with the departure of the founders at the end of June, and the arrival of a new MD, the business returned to profit in the second half.

Whitegates increased revenues by 14%, CJ Cole was up 9%, Parkers 6%, Martin & Co 5% and Ellis & Co 3%. The overall pattern was of revenue growth in a marketplace where many competitors were reported in reverse gear. The housing market was flat but the group concentrated on winning more sales instructions (up 23%) and growing their managed properties portfolio (up 8%).

The government has offered some clarity on its intention to ban tenant fees. The timing of the implementation of the ban appears to be Q1 2019 which means that trading in 2018 would be unaffected. They are already taking action to mitigate the effects of the ban which is expected to put at risk 16% of the franchisees lettings revenue and 9% at the group level. Mitigation factors include accelerating the size of the tenanted managed portfolio, developing income from financial services and conveyancing referrals.

During the year the group re-developed each of their five traditional brand websites, starting with Whitegates. Overall the website project generated 17,000 new business leads at an average cost to the franchisees of £24 per lead. The board believes that the new websites delivered a competitive advantage in the second half of the year.

There was a net exceptional income of £701K during the year, all relating to the EweMove acquisition. It consists of as reduction in deferred consideration of £1.2M and an impairment charge of £500K against the master franchise agreement following a revaluation due to evidence suggesting that the business’ value may have been impaired. A further amount of up to £7M in deferred consideration was due subject to various targets being met but a renegotiation took place and it was reduced to £1M which was paid during the year. No further payment is due.

At the current share price the shares are trading on a PE ratio of 13.2 which falls to 11.8 on next year’s consensus forecast. After a 15% increase in the dividend the shares are yielding 4.3% which increases to 5.3% on next year’s forecast.

Overall this has been a fairly productive year for the group. Profits were up, but underlying profits seem to have seen just a modest rise. Net assets increased though, due to the reduction in deferred consideration, and the operating cash flow improved with a decent amount of free cash being generated. All of the brands seem to have done fairly well, and Ewemove has now moved into profit which bodes well for the coming year. The ban on tenant fees, which is something I fully support generally, is not good for this company and offers some headwinds going into 2019. The forward PE of 11.8 and yield of 5.3% mark the shares as decent value, however, and I am tempted to get back in here.