Safestyle has now released its final results for the year ended 2016.

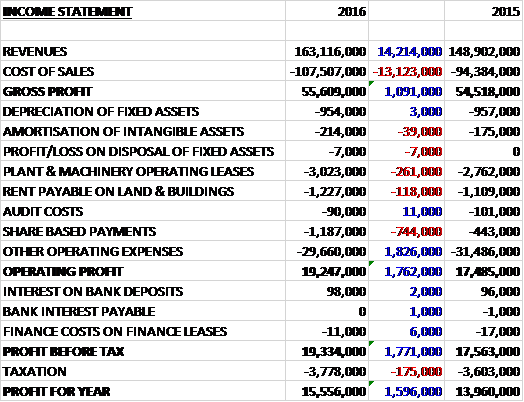

Revenues increased by £14.2M when compared to last year and after cost of sales grew by £13.1M, the gross profit was up £1.1M. There was a £261K increase in operating lease costs, a £118K growth in rent charges and a £744K increase in share based payments, offset by a £1.8M decline in other operating expenses to give an operating profit £1.8M above last time. Finance charges barely moved by tax costs increased by £175K to give a profit for the year of £15.6M, a growth of £1.6M year on year.

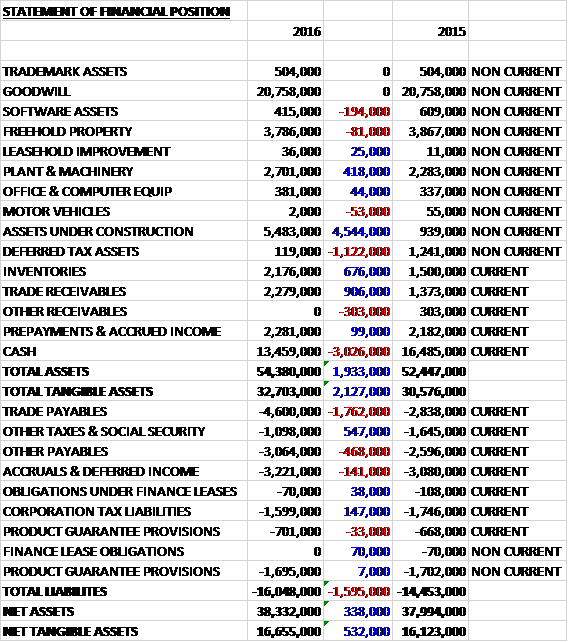

When compared to the end point of last year, total assets increased by £1.9M driven by a £4.5M growth in assets under construction, a £906K increase in trade receivables, a £676K growth in inventories and a £418K increase in plant and machinery, partially offset by a £3M decrease in cash, a £1.1M fall in deferred tax assets and a £303K decline in other receivables. Total liabilities also increased during the year as a £547K decline in tax and social security payables was more than offset by a £1.8M growth in trade payables and a £468K increase in other payables. The end result was a net tangible asset level of £16.7M, a growth of £532K year on year.

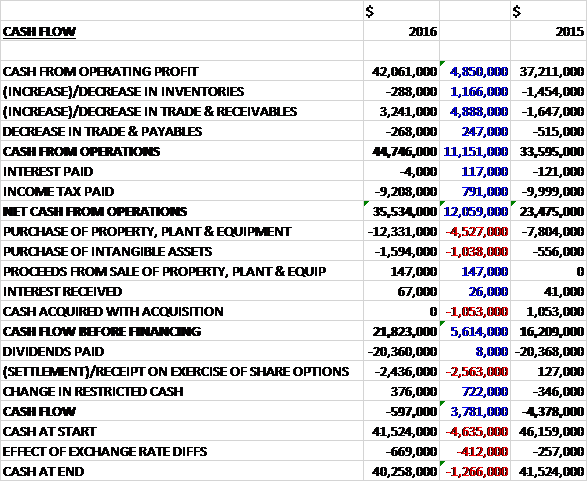

Before movements in working capital, cash profits increased by £5.4M to £24.3M. There was a cash outflow from working capital and a £353K increase in taxes paid which meant that the net cash from operations came in at £17.2M, a growth of £2.6M year on year. The group spent £5.9M on property, plant and equipment, mainly reflecting the factory expansion, to give a free cash flow of £11.4M. They paid back £108K on finance leases and spent £14.4M on dividends to give a cash outflow for the year of £3M and a cash level of £13.5M at the year-end.

During the year the volume of frames installed increased by 3.2% to 288,460 and the average unit sales price was up 6.4% to £565 following a price list increase at the start of 2016 to counteract the additional costs of the new consumer finance products introduced and also reflecting the growth in conservatory upgrades. The market share has continued to increased, up from 9.5% last year to 10.2% in 2016.

The group continued to expand their sales branch network during the year with new openings in Guildford and Norwich. In addition they added an installation depot in South Wales in February 2017 to increase their capacity in that region. There still remain significant opportunities to widen their sales network over the course of the coming year.

They have continued to increase their activity in generating enquiries from digital media and direct response channels, which accounted for 41% of all orders compared to 37% in the prior year. Lead generation from door canvassing remains an important part of the marketing mix, however, and the value of business from this source increased by 9%. The planned increased investment in direct and digital marketing will remain an important factor in 2017 as they aim to reduce lead generation costs.

The weakness in Sterling following Brexit resulted in increased raw material costs in the second half of the year. These have been fully offset through a price increase at the start of 2017, however. Going forward, the strength of their market position, low cost manufacturing capabilities and the track record of sustainable price increases leave the group well positioned to manage any further input cost pressures.

The investment in the expansion of the manufacturing facility is near completion and remains on plan and budget and scheduled to be fully operational in the summer of 2017. They have received and installed the new glass toughening furnace, high speed cutting table and high speed IGU line. By June they will have transferred the existing glass manufacturing process to the new factory. The manufacture of both the frames and double glazed units on a single site will reduce handling, improve quality, increase efficiency and enhance capacity as the group broadens their product range and continue to grow market share.

Following the launch and proof of concept of their conservatory upgrade product in 2015, growth accelerated in 2016 and they installed 551 conservatory upgrades against a target of 450. They expect continued growth in 2017 as the contribution from this revenue stream increases. The new premium products and colours introduced in 2016 have steadily gained traction and are contributing to the broader product offering and appeal.

So far in 2017, order intake is up 4% broadly reflecting the increase in selling prices and more than offsetting the higher raw material costs resulting from the weaker pound. The board are mindful of the uncertainty in the macroeconomic outlook but remain confident of delivering growth over the year ahead.

At the current share price the shares are trading on a PE ratio of 16.7 which falls to 14.6 on next year’s consensus forecast. After a 10.3% increase in the final dividend the shares are yielding 3.6% which increases to 3.9% on next year’s forecast.

Overall this has been another successful year for the group. Profits increased, net assets grew and the operating cash flow was up with plenty of free cash being generated. The group’s market share improved and the conservatory upgrade business seems to be doing well. There are headwinds in the form of raw material cost increases due to the strength of sterling but the group seems to be quite good at mitigating these effects and so far in 2017, price increases have been outpacing raw material hikes. The new factory expansion should also be coming on stream this year which should help with efficiencies. Going forward the PE is 14.6 and yield is 3.9% which looks about right to me and I continue to hold.

On the 18th May the group released a trading update. The year started positively with robust order intake in Q1, however recent trading has been weaker than expected reflecting the latest FENSA stats which have shown a significant contraction in the overall market. As a result, compared to a strong equivalent trading period last year, the group has seen more modest overall growth of 2% in order intake for the first four months of the year.

They expect to grow revenues in the first half but anticipate profits will be lower due to a combination of lower than planned volumes and some parallel running costs following investment in the new production facilities. There are a number of initiatives underway and combined with the impact of enhanced production productivity, the board expect an improved performance in the second half.

They continue to gain market share and build their order book during the period and whilst they are currently operating in a more challenging trading environment, the board are confident of delivering full year results broadly in line with market expectations.

This is a bit of a shame. There is no doubt this remains a great company in good shape but I am a little worried that the fall in demand has been very recent. I think the prudent thing to do would be to take profits now and wait to see if this is a blip or the start of something more serious.

On the 18th July the group released a half year trading update. Since their last trading update, the group has continued to trade in line with earlier months with order intake levels continuing 2% up year on year. Within this overall figure, however, the trend from week to week during Q2 has been more volatile than experienced for a long time. Furthermore, market stats show a market decline in volumes terms of over 10%. Against this backdrop of patchier consumer demand, it is clear that the group has taken further market share.

The group expect to report marginal revenue growth in the first half but with reduced profits. Given the uncertain market conditions and weaker consumer confidence, the board consider it prudent to expect only modest revenue growth again in the second half. This would result in profits for the year being lower than previously anticipated and broadly in line with last year. Cash flow has continued to be strong and they had net cash of £17.7M at the period end compared to £23.6M at the same point of 2016 reflecting the investment in new production facilities and the special dividend.

In anticipation of a continuation of the recent weaker trading environment, the board have taken action to reduce their operating costs in the second half. Long term, this may well turn out to be a buying opportunity but the market is just too uncertain at the moment. The group continues to outperform its peers but in a falling market, this doesn’t really help. I remain on the side lines for now.