IQE has now released its final results for the year ended 2016.

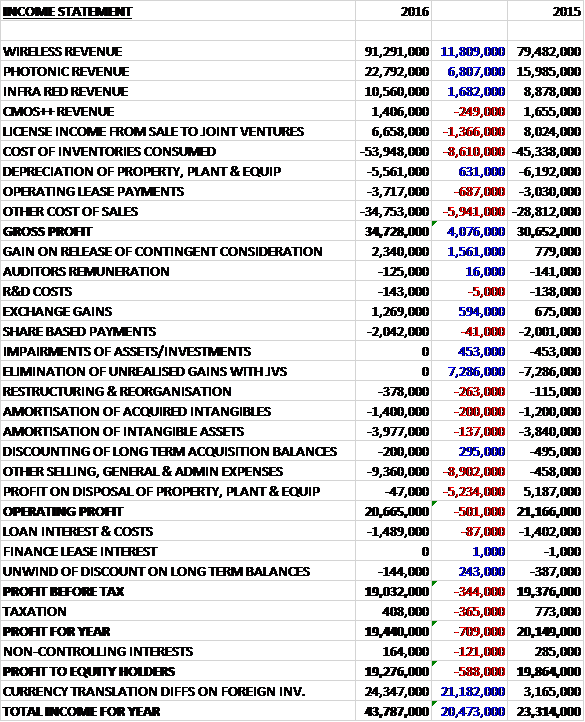

Revenues increased when compared to last year, aided by currency benefits as a £1.4M decline in licence income and a £249K fall in CMOS++ revenue was more than offset by an £11.8M growth in wireless revenue, a £6.8M increase in photonic revenue and a £1.7M growth in IR revenue. Cost of inventories were up £8.6M and other cost of sales increased by £6M to give a gross profit £4.1M above that of last year. The profit from the reduction in deferred consideration was up £1.6M, exchange gains increased by £594K, there were no investment impairments which were £453K last time, and no joint venture unrealised gains (£7.3M).

Offsetting this was an £8.9M increase in other general costs, partly related to currency movements, and a £5.2M reduction in the profit on disposal of fixed assets which saw operating profit fall by £501K. Finance costs fell slightly but tax income was down £365K to give a profit for the year of £19.3M, a decline of £588K year on year.

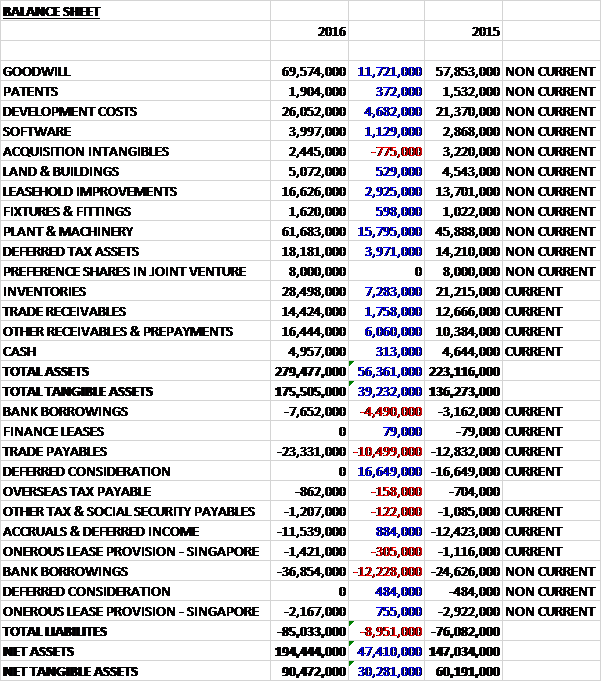

When compared to the end point of last year, total assets increased by £56.4M driven by a £15.8M growth in plant and machinery, an £11.7M increase in goodwill, a £7.3M growth in inventories, a £4.1M growth in development costs, a £3.9M increase in deferred tax assets and a £6.1M increase in other receivables and prepayments. Total liabilities also increased during the year as a £16.6M reduction in deferred consideration was more than offset by a £16.7M increase in bank borrowings and a £10.5M growth in trade payables. The end result was a net tangible asset level of £90.5M, a growth of £30.3M year on year.

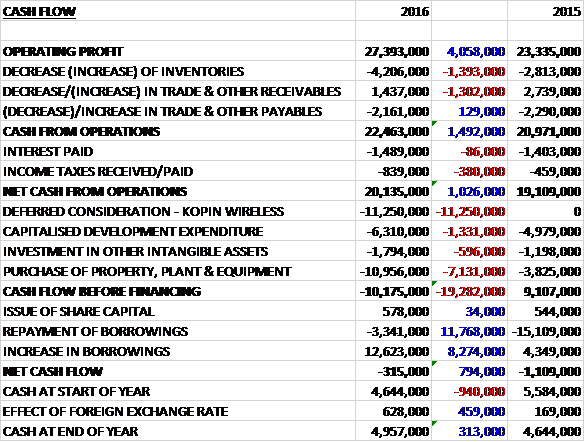

Before movements in working capital, cash profits increased by £4.1M to £27.4M. There was a cash outflow from working capital and tax payments increased by £380K to give a net cash from operations of £20.1M, a growth of £1M year on year. The group spent £6.3M on development expenditure, £1.8M on other intangible assets and £11M on property, plant and equipment, along with £11.3M on deferred consideration for Kopin. This meant that before financing there was a cash outflow of £10.2M. The group therefore took out a net £9.3M of new borrowings to give a cash outflow of £315K for the year and a cash level of £5M at the year-end.

The adjusted operating profit in the Wireless division was £8M, a growth of £803K year on year as the destocking that characterised last year was absent. The market cooled in 2013 as the innovation cycle slowed down but smartphone shipments increased by 2.8% in 2016 which is broadly in line with the group’s forecast for a mid-single digit rate of growth (a bit under I would say). The outlook for the wireless materials market has a good potential to return to double digit growth due to innovations in smartphone hardware such as the adoption of advanced photonics sensors, the adoption of GaN on Silicon technology for base stations, the transition to 5G communications and the adoption of compound semiconductors using cREO for other wireless communication chips.

The adjusted operating profit in the Photonics division was £6.9M, an increase of £2.6M when compared to last year with key milestones delivered on several major programmes during the second half, providing significant growth opportunities. The driver has been VCSEL and InP technologies which enable a broad range of applications from fibre optic communication to advanced sensors and industrial processes.

Vertical Cavity Surface Emitting Lasers (VCSEL) is the key enabling technology behind a number of high growth markets including 3D sensing, data communications, data centres, gesture recognition, health, cosmetics, illumination and heating applications. The group is the market leader for outsourced VCSEL materials. Indium Phosphide (InP) enables fibre to the premises. The continued development of this technology to achieve higher performance at lower costs plus the growth in data traffic is finally leading to the extension of the fibre optic network to the premises. The group has developed laser technologies with differentiated IP which underpins their high growth expectations for this business. Other drivers in this market include optical interconnects, 3D sensing, gesture recognition, laser projection and LEDs.

The adjusted operating profit in the IR business was £2.2M, a growth of £1M when compared to 2015. Significant contract wins and progress in a number of development programmes underpin the continued growth of this business and progress towards new high volume applications. The group is the technology leader in this market with the launch of the industry’s first 150mm indium antimonide wafers, a major milestone in reducing the overall cost of chips. This was followed up with a number of significant contract wins. In addition there has been significant work in developing these materials for consumer sensing applications which will drive much higher volumes in the future. The board expect this market to grow at a rate of about 5-10% for the near future.

The adjusted operating loss in the CMOS++ business was £1.6M, a decline of £91K year on year. The group is involved in multiple programmes which are developing the core technologies from which they expect significant revenue streams to emerge over the next three to five years.

The profit from license income sales to joint ventures was £6.7M, a decrease of £1.4M when compared to last year but this was higher than expected.

The advanced solar technology has been hampered by global macroeconomics as the cost of oil has fallen. The terrestrial market remains an opportunity but as a result of the shifting macroeconomics, focus has shifted to the space market where these advanced materials are used to power satellites where the higher efficiency has a dramatic cost benefit on payload. Product qualifications are underway with satellite manufacturers, paving the way for commercial revenues.

There have been a number of milestones this year. Good progress with new cREO technology delivered some early wins, including delivering a step change in GaN on silicon technology (the elimination of parasitic channel) and engagement in development programmes for advanced RF filter applications. A key customer is engaged in end market qualification using the group’s GaN on Silicon material, signifying that this technology is close to commercialisation. The UK joint venture was a catalyst in securing £300M of funding towards the continued development of a UK CS cluster and the Singapore joint venture has been selected as a partner in a major programme for CS on silicon technology.

The group generated a non-cash profit of £2.3M arising from a reduction in the estimated remaining deferred consideration settled via a trade discount. The consideration has now been fully settled. The restructuring and reorganisation costs of £400K reflect some one-off costs relating to staff, facility and asset write downs associated with the restructuring of the manufacturing operations. The gain on disposal of fixed assets from 2015 related to a non-cash exceptional gain of £4.8M relating to the group’s contribution to the creation of a joint venture.

Going forward, the current financial year has started well and the group is trading in line with expectations. The board remain confident that they are on track to achieve expectations for the full year and expect to benefit from strong cash flows.

If we exclude the profit from the deferred consideration elimination, the shares are trading on a PE ratio of 23.6 which falls to 17.8 on next year’s consensus forecast. At the year-end the group was in a net debt position of £39.5M compared to £23.2M at the start of the year although if we include the deferred consideration, there was a 2% decline in net debt and a lot of the increase was actually down to currency movements. No dividends were declared for the year.

Overall then this has been a decent year for the group. It is quite hard to get at the underlying profits but if we strip away this year’s gain on the release of contingent consideration and last year’s profit from sale of items to the joint venture, underlying profits did grow. Net assets also increased, as did the operating cash flow although no free cash was generated. The wireless division is slowing down somewhat and has been overtaken by the photonics division which seems to be going very well. The IR business is still small but seems to be growing nicely too. All this is positive then but the valuation is also rather high. There is quite a bit of debt and a forward PE of 17.8 is tempting me to get out while the going is good.

On the 19th May the group announced that Finance Director Philip Rasmussen and Operations Director Howard Williams both sold 1,900,000 shares at a value of £1.3M each. The transactions are apparently for future retirement planning purposes and leaved Philip with 1,573,357 shares and Howard with 2,392,965. As it happens, I agree with the directors and think that it would be sensible to bank profits here given the shares have more than doubled.

On the 20th July the group released a trading update covering the first half of the year. They expect to deliver around £70M in revenues, reflecting increased sales in each of the three primary markets. Notably, photonics continued to deliver strong double digit growth, enjoying the early phase of a significant ramp in VCSEL wager supply for mass market consumer applications. As a result, overall wafer sales are expected to grow by around 16%. This has also been supplemented by £1M of license income, although this was below the £3.5M received in the first half of last year.

The group is engaged in a range of programmes which provide significant upside potential to its near and mid-term growth expectations. The start of the mass market ramp for VCSEL wafers marks an inflection point in the commercialisation of this technology. The group has secured multiple multi-year contracts for this ramp which reflects its strong competitive advantages including its technology leadership and its proven track record in delivering wafers into high volume consumer markets.

As a result the board has now approved a capacity expansion plan to meet higher levels of expected demand for H2 2018. This follows increased investment during the first half of 2017 in operating costs, product development and working capital. As part of the expansion plan the ground announced that it has agreed terms for the lease of a new premises in South Wales. The lease is with the Cardiff City Region, is for eleven years and provides the group with an option to extend or purchase the freehold. They have also placed orders for new MOCVD equipment. Following the devaluation of Sterling, currency provided a tailwind of about 10% year on year.

Overall, all business units have progressed in line with expectations but the photonics unit has been the stand out with continued strong double digit growth, accelerating towards the end of the period. In light of recent progress and its increasingly confident outlook, the board expects the group will now exceed market expectations for the full year and whilst it is early into the start of the mass-market adoption of their technology, it is possible that with the current contract momentum, a more significant upgrade to current market expectations could be delivered for 2018.

So, there is a lot to digest here. It seems clear that there is potential for exciting growth here, and the last sentence sounds very bullish. It should also be noted, that it sounds as though here will be quite a big demand for cash this year so I very much doubt there will be any free cash available again, and the shares are now looking rather expensive. In conclusion, however, I regret taking profits here and feel the upside potential is still potentially significant so I have bought back in (at a much higher price than I sold 🙁 )

On the 28th July the group announced that CEO Andrew Nelson sold 5,800,000 shares in the company at a value of £6.15M. In addition Chairman Godfrey Ainsworth sold 1,000,000 shares at a value of £1.05M. These disposals are apparently for future retirement planning purposes and in the case of the CEO, the sale was used to secure the required funds to repay an existing loan which was used to purchase shares in the first place. It is his intention that he will repay the existing loan ahead of the repayment date. They have no plans to sell any more shares and after the transaction, Dr. Nelson still holds 29,459,218 shares and Dr Ainsworth has 2,154,197 shares.