Spectris has now released their final results for the year ended 2016.

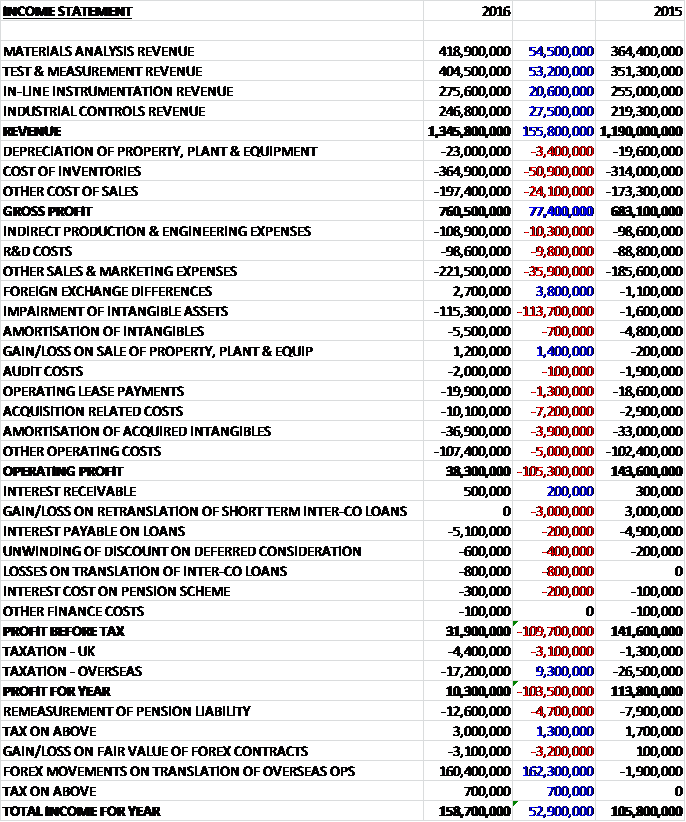

Revenues increased when compared to last year, mainly as a result of favourable currency movements with a £54.5M growth in Materials Analysis revenue, a £53.2M increase in Test and Measurement revenue, a £27.5M growth in Industrial Controls revenue and a £20.6M increase in In-line instrumentation revenue. Cost of inventories was up £50.9M and other cost of sales increased by £27.5M to give a gross profit £77.4M above that of last time. Indirect production costs grew by £10.3M, R&D costs were up £9.8M and other sales and marketing expenses increased by £35.9M. We then see a £113.7M increase in intangible asset impairments and a £7.2M growth in acquisition related costs which meant that the operating profit fell by £105.3M. Finance costs increased somewhat, mainly due to the lack of a gain on the retranslation of inter-company loans but tax charges declined by £6.2M to give a profit for the year of £10.3M, a decline of £103.5M.

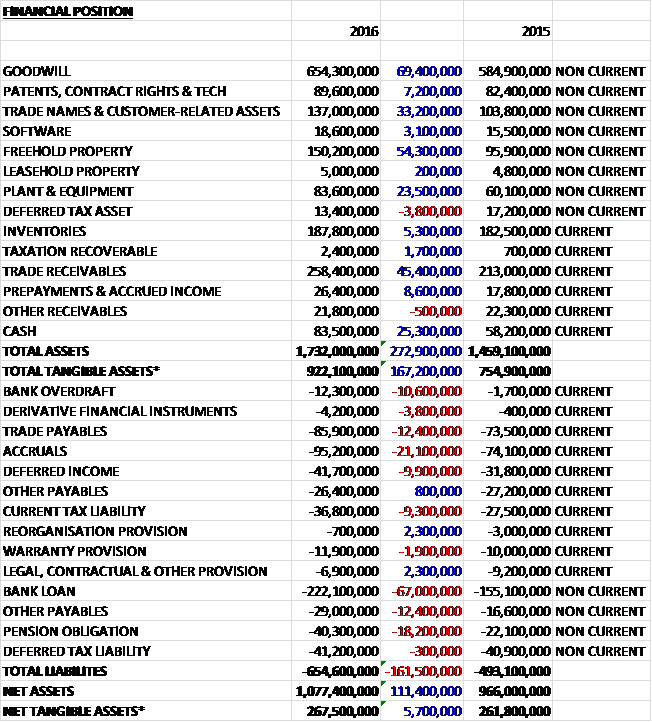

When compared to the end point of last year, total assets increased by £272.9M driven by a £69.4M growth in goodwill, a £54.3M increase in freehold property, a £45.4M growth in trade receivables, a £33.2M increase in trade mark values, a £25.3M growth in cash and a £23.5M increase in plant and equipment. Total liabilities also increased during the year due to a £67M growth in the bank loan, a £21.1M increase in accruals, an £18.2M growth in pension obligations, a £12.4M increase in trade payables and a £12.4M growth in other payables. The end result was a net tangible asset level of £267.5M, a growth of £5.7M year on year.

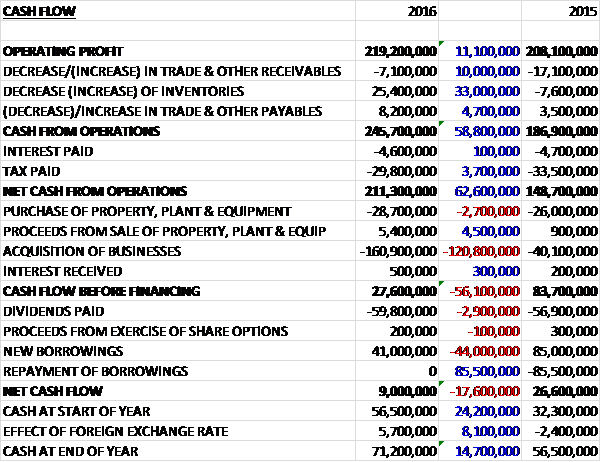

Before movements in working capital, cash profits increased by £11.1M to £219.2M. There was a cash inflow from working capital and tax payments declined by £3.7M to give a net cash from operations of £211.3M, a growth of £62.6M year on year. The group spent £28.7M on capex and £160.9M on acquisitions to give a free cash flow of £27.6M. This did not cover the £59.8M paid out in dividends so the group took out £41M of new loans to give a cash flow of £9M and a cash level of £71.2M at the year-end.

Overall the adjusted operating profit increased by 11% but acquisitions accounted for 4.6% of this growth and positive forex movements accounted for 12.5% so like for like profits actually declined by 6.2% during the year.

The operating profit in the Materials Analysis business was £76.2M, a like for like increase of £15.8M year on year although like for like sales growth was just 2% driven by China and Japan with North America and Europe down slightly. The growth in profits was mainly due to a better mix of product and cost cutting actions.

From the start of 2017 the group merged two of the segment’s operating businesses – Malvern Instruments and PANalytical. In November, PANAlytical launched Aeris a benchtop x-ray powder diffractometer and the target markets have been extended beyond the cement, minerals, metals and research markets traditionally associated with PANalytical to include the pharmaceuticals and fine chemicals markets where Malvern holds a leading position.

Sales to the pharmaceuticals and fine chemicals industries rose on a like for like basis during the year, particularly pleasing given last year benefited from the demand from regulatory compliance requirements in the Indian market. Asia saw particularly strong growth from China, India and Japan while European and North American sales were up modestly.

The metals, minerals and mining sector reversed its good 2015 performance and saw like for like sales decline. All regions experienced falls and large systems orders continued to be deferred or cancelled and the growth within the cement and building materials markets in North America and Europe in recent years has slowed. Aftermarket sales were solid, however, as customers’ production volumes continued at good levels.

Although there was reasonable sales growth to academic research institutes in North America and Asia, underlying demand was subdued with significant weakness in the UK. Sales to the semiconductor, electronics and telecoms industry grew strongly, particularly in Asia. Sales in North America were notably weaker year on year, however. Sales of the new ultra-high sensitivity particle counter products which were launched in 2015, performed well.

Going forward, the merger of Malvern and PANalytical is expected to begin to generate revenue synergies as they benefit from a more comprehensive offering to their customers. The underlying trading in conditions in the end markets will be the key driver of near term performance, however. Within pharmaceuticals the board expect regulatory scrutiny of manufacturing processes to continue to increase and drive demand for their material characterisation and clean room products and services. They expect these factors will more than offset what is likely to remain an unpredictable academic research market given public sector budget constraints in certain regions. The board are also seeing a cautiously improving investment client in the mining sector but do not expect to see a major pick-up in demand as yet.

The operating profit in the Test and Measurement business was £61.8M, a like for like decline of £7.8M excluding a £7.8M benefit from forex movements and a £5.1M increase from acquisitions. Like for like sales fell by 4% and only Asia showed any growth with sales in North America notably lower and European sales down modestly.

The underlying demand from the automotive sector remained healthy, particularly in R&D with one of the key drivers of demand being the electrification of power trains for deployment in electric and hybrid vehicles. This created opportunities for the group’s EDrive testing solution which enables the electric motor, inverter and battery data to be quickly evaluated. This also creates opportunities for the NVH service offering as engine noise is reduced from motor vehicles, noise evaluation and control shifts focus to sources elsewhere in the car such as tyres.

In machine manufacturing there was sales growth as a decline in North America was offset by increased sales to Asia and Europe. Sales to the aerospace sector decreased and were lower in each of the regions except North America due to the completion of several major R&D programmes. During the year the group custom-developed sensing solutions for Marenco’s new helicopter. Reflecting some pressure on public finances, sales to academic research institutes declined with weakness in demand in all regions except China. Sales to consumer electronics customers declined although sales patterns are lumpy reflecting the scheduling of projects by customers.

Sales of the environmental noise monitoring services declined partly due to a one-off major contract in 2015. The UK and Japan were the only major markets to deliver growth as the business secured a key contract to provide Heathrow Airport with 50 noise monitoring terminals, and launched Airport Noise Monitoring on Demand. They established a dedicated urban sales force to widen their market reach for noise monitoring equipment and services and secured orders during the year.

The weakness in the unconventional oil and gas markets continued during the year and the group saw a further sizeable decline in sales of their microseismic monitoring solutions, particularly in North America. As a result, they have looked to develop opportunities in other markets and are making progress in this regard in Latin America and the Middle East. Their performance was better in the mining sector where sales were flat, with demand for microseismic monitoring growing. For example they have been working more closely with Grasberg, the world’s largest copper-gold mine, supplying microseismic monitoring equipment and analytics for different phases of development as well as improving safety and efficiency.

Going forward the group expect the automotive and aerospace sectors to benefit from further growth in demand for engineering software applications. Additionally the continued robust investments in the development of electric and hybrid vehicles will support demand for their torque and eDrive solutions. The underlying business trends in the consumer electronics market remain healthy but market conditions in the oil and gas industry are expected to remain subdued. There may be more opportunities for the deployment of microseismic in the mining space, however.

The operating profit in the In-Line Instrumentation business was £41.2M, a like for like decrease of £3.8M excluding a £5.4M benefit from forex movements and a £600K contribution from acquisitions. Like for like sales declined by 4% as a small rise in North American sales was more than offset by declineS in Asia and Europe, reflecting ongoing weakness in capex across many heavy process industries.

In the pulp and paper market, like for like sales were down slightly. They continued to see a diversification away from graphic paper towards the tissue and pulp markets, translating into growth for their tissue business which is partly offsetting the decline in traditional coating bladed.

In the energy and utilities market, sales were down notably as the weak oil and gas markets continued to have an adverse impact on demand. There was a lack of new larger projects in the hydro-carbon processing sector but other areas such as industrial gasses, emissions monitoring and the Hummingbird OEM sensor business continued to perform well. In November the group launched their first moisture detector which allows the fast and accurate measurement of moisture in process applications. It is designed to integrate with their digital oxygen analyser as the measurement of both oxygen and moisture is a common requirement in many applications.

The group are continuing to see modest growth in the wind energy sector and have focused on wind farm owners and operators in addition to the traditional turbine OEM segment, in order to offer them a post-warranty solution for their turbine fleet that is OEM independent with this initiative having identified significant opportunities. They have also expended their offering to non-wind power applications in other industrial markets with the B&K Vibro business securing a condition monitoring contract with a biomass power plant in the UK and a contract to supply a turnkey condition monitoring and machine protection solution for remote monitoring at a polyethylene plant in Northern Asia.

Sales to the web and converting industries increased notably during the year with a particularly strong performance in Q4 after customers were delaying projects in 2015. They have seen a number of opportunities emerge in the medical market and in food, particularly in relation to snack products. For example, a medical tube manufacturer uses the group’s measurement and control system to control the critical dimensions and quality of tis extruded products and in India a snack manufacturer has improved quality and production efficiency with online moisture and oil measurement for crisps and snacks lines.

Going forward, the changing mix in the pulp and paper business is expected to continue in 2017 and the group expect to benefit from the combination of Capstone’s software tools with BTG’s instruments to capture new opportunities. They expect growth from the energy and utilities sector to be modest. The renewable energy sector remains healthy and the expansion of their offering to differing customer types and new areas of the market offer potential new sales opportunities but the oil and gas sector remains fragile.

The operating profit in the Industrial Controls business was £21.6M, a like for like fall of £15M excluding a £1.7M forex benefit and a £2.3M contribution from acquisitions. Like for like sales declined by 2% with a sharp decline in sales to North America. The poor profit performance was further exacerbated by the performance of Omega.

Omega derives the majority of its sales from the US and the weak US industrial environment impacted demand for its products. In addition, the implementation of a new ERP system at the business highlighted the need for certain processes to be improved with temporary additional resources required during the consolidation of two distribution centres on the US east coast. This resulted in significant inventory adjustments and higher labour costs. A new organisational structure and management team has been put in place and the focus is on remedial action to redesign the operational processes and improve customer service.

In Asia there was strong sales growth, in particular driven by continued good progress in the expansion of the group’s process measurement and control business outside the US. The internationalisation of Omega continues to produce promising results, with good sales growth in all major markets outside the US. In Europe overall segment sales were flat with a challenging year for their industrial networking business being partly offset by sales growth in process measurement and control products.

The increasing trend towards the industrial internet of things is benefiting their industrial automation and networking business and the group’s product development was focused on simplifying the integration of customer generated data and IoT cloud platforms. During the year they launched the latest version of their Crimson software, adding control capability to their products. This provides a key solution for customers as it removes the need to purchase standalone control components. They had further success with their networking products in the automotive industry, securing a contract for as major car maker’s new plant in Latin America.

The acquisition of Label Vision Systems in 2015 has delivered very positive results during 2016 with strong sales growth of its products as the market expands due to regulatory trends and quality requirements. It has been fully integrated into Microscan and this has enabled the expansion of LVS products into key international markets and to leverage the synergies between LVS and Microscan operations. Following the launch in 2015 of a scalable industrial barcode imager and smart camera platform, further developments were made this year with autofocus and smart camera versions.

Going forward, given the significant exposure to the US, performance will be largely driven by the performance of US industrial markets. The PMI manufacturing index has turned more positive recently but it is too early to assess the extent of any positive market momentum. At Omega the board expect the organisational changes to deliver an improvement in performance and to exit the year with margins at historic levels.

There were a number of impairments during the year. There was a £94.4M impairment charge relating to Omega as a consequence of the 2016 performance and lower projected cash flows. This has resulted in a reassessment of its expected future business performance in light of the trading environment and the actions required to improve profitability. There was also a £20.9M impairment charge relating to ESG due to the continuing difficult external market conditions caused by the low oil and gas prices.

In February the group acquired CAS Clean Air Service for £12M, generating goodwill of £5M. The business is based in Switzerland and extends the group’s capabilities in monitoring and calibration services in the life sciences market. In June the group acquired Integrated Process Systems, an Indian agent, for a total consideration of £900K, generating goodwill of £500K. It is being integrated into the Test and Measurement segment. Also in June the group acquired Capstone Technology Corporation for a total consideration of £14.8M, generating goodwill of £9.6M. The business is based in the US and is a provider of software solutions for process control optimisation and decision support, serving multiple industries such as pulp and paper, chemicals, utilities, oil and gas and beverages. It is being integrated into the in-line instrumentation segment.

In July the group acquired Sound and Vibration Technology for a consideration of £400K, generating £100K of goodwill. The business is based in the UK and provides sound and vibration test based solutions. Also in July the group acquired DISCOM for a total consideration of £20.4M, generating goodwill of £12.2M. The business is based in Germany and provides integrated solutions combining hardware and software to enhance production quality and identify potential problems in manufacturing processes. It is being integrated into the Test and Measurement segment.

In September the group acquired Millbook for a total consideration of £125.7M, generating goodwill of £54.1M. The business is based in the UK and extends the group’s capabilities to provide test, validation and engineering services to the automotive, transport and tyre, petrochemical, defence and securities industries. It is being integrated into the Test and Measurement segment. The revenue and operating profit contribution from the acquired businesses in the year was £28.9M and £2.1M respectively.

The year ended well with like for like sales growth in Q4 following challenging trading conditions in the first nine months of the year although end market growth in the near term is expected to be modest. Planned capex in 2017 is expected to be significantly higher than in 2016 at around £70M, primarily related to expansion opportunities at Millbrook and a number of infrastructure projects at HBM, Omega and Malvern Instruments.

At the current share price the shares are trading on a PE ratio of 26.3 (if we ignore the intangible impairment) and this falls to 19.7 on next year’s consensus forecast. At the year-end the group had a net debt position of £150.9M compared to £98.6M at the end of last year. After a 5% increase in the dividend the shares are yielding 2% which remains the same on next year’s forecast.

Overall then on the surface this has been a good year. Profits were up, excluding the impact of the impairments, net assets increased and the operating cash flow improved with some free cash being generated, although not enough to cover the dividends. Scratch beneath the surface, however, and it can be seen that favourable forex movements were responsible for the decent performance and like for like profits declined. The one sector that is doing fairly well is Materials Analysis which saw some modest sales growth which when mixed with cost cutting measures meant that profit grew nicely. Going forward, public spending restrictions are likely to hold back academic research demand, however.

All the other segments saw like for like profits decline. Both Test and Measurement, and In-line Instrumentation suffered from the weakness in the oil and gas industry – a driver that is likely to remain in the near term at least. Industrial Controls saw performance decline the most, affected by a weak US industrial environment and structural issues within the Omega business. Both of these drivers should improve in the coming year, however. So, with some markets remaining precarious I think the forward PE of 19.7 and dividend yield of 2% do not really properly account for the uncertainty and I do not hold.

On the 17th May the group released a trading update covering the first four months of the year. Reported sales were up 22% and like for like sales increased by 4% against a weak prior year comparator. Acquisitions contributed 5% to sales growth and forex movements positively impacted revenues by 13%. Like for like sales grew 11% in Asia Pacific, 4% in Europe and declined by 1% in North America.

In May the group completed the acquisition of Setpoint for a consideration of $10M. The business will become an integrated product line of Bruel and Kjaer Vibro, growing their presence in the condition monitoring market. Setpoint is a provider of vibration and condition monitoring solutions to process industries, primarily the oil and gas and power generation sectors. Its technology enables customers to improve machinery availability, productivity, and reliability by delivering accurate condition information.

The performance to date has been in line with expectations. Trading conditions in the period have improved but performance is still fairly mixed and as a result, the board’s underlying outlook for 2017 remains broadly unchanged.

On the 2nd June the group announced that Chairman Mark Williams acquired 15,000 shares at a value of just under £400K. This is quite a good buy in my opinion.