Conviviality Retail has now released its interim results for the year ending 2015.

When compared to the first half of last year revenues fell by £766K due to the closure of underperforming stores but a larger fall in cost of sales meant that gross profit was some £3.1M higher. During the first half of the year, the only one-off cost was a £531K restructuring charge compared to £3.3M worth of costs relating to the IPO that occurred last year. We also see a £381K share based payment this year and other operating costs were £2.7M higher relating to increased costs at company owned stores to give an operating profit of £2.7M compared to a small loss during the first half of last year. Finance costs were significantly lower than last time but there was a tax charge as opposed to a rebate that meant the profit for the period was £2.1M, a £3M positive swing when compared to the first six months of 2014.

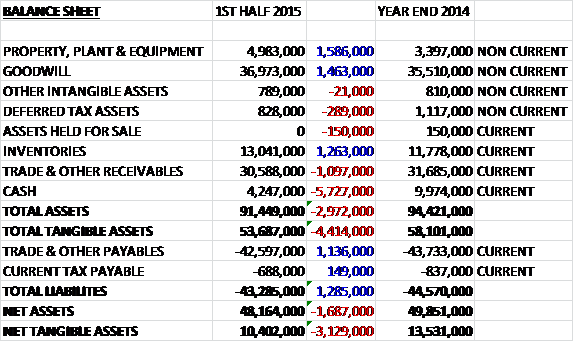

When compared to the end point of last year, total assets at the half year point fell by just under £3M as a £5.7M decline in cash levels and a £1.1M fall in trade and other receivables were partially offset by a £1.6M increase in property plant & equipment, a £1.5M growth in goodwill and a £1.3M increase in inventories. Total liabilities, what little there are, also fell mainly due to a £1.1M decline in trade and other payables to give net tangible assets of £10.4M, a decline of £3.1M.

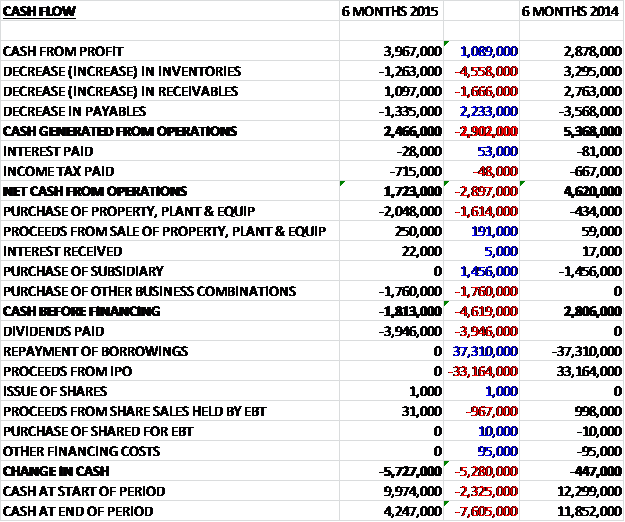

Before movements in working capital, cash profits were £1.1M higher than in the first half of last year but this was eroded by a decrease in payables and an increase in inventory so that cash generated from operations fell by £2.9M to just £1.7M. All of this cash was spent on the purchase of property plant and equipment, mainly relating to increased investment in the franchisee estate and logistics capabilities so that the £1.8M spent on the purchase of Rhythm and Booze sent the cash flow before financing to a negative £1.8M. As well as this, the group spent £3.9M on dividends so that the cash outflow for the period was £5.7M to leave just £4.3M at the end of the period. Clearly this is not a sustainable position as there is no free cash flow let alone enough to pay those dividends.

During the period, there has been an improvement in the quality of franchisees as underperforming ones are closed and successful ones expand. The logistics capability has been transformed, with replacement wracking in the warehouse completed that will improve the efficiency of the store pick operation and adds more capacity to support expansion. The off-licence franchisee margin increased 0.4% to help average franchisee profitability grow 6.4%.

One initiative that has been launched over the period is a price led grocery range to drive larger basket sizes. The group is very strong in their core traditional off-license category and as well as trying to drive grocery purchases, management have been focusing on improving the wine offering, hence the previous purchase of Wine Rack which also gives them scope to tailor the store offering depending on the area that it is located in. Other areas earmarked for growth are expansion in to new geographies and the launch of BB Warehouse on a trial basis in Wakefield. This format is designed to attract bulk purchase customers and there are plans to expand the trial over the next year.

On the 2nd May the company acquired certain assets of RNB stores including 26 outlets for a total consideration of £1.7M, of which £1.4M was goodwill. They subsequently acquired a further five stores for £180K. All stores were rebranded from the previous Rhythm and Booze brand to an appropriate Conviviality fascia. The acquisition allows the group to increase its presence in an area that it is underrepresented. During the period directors Keith Webb and Diana Hunter exercised and sold large numbers of shares, which in the case of the CEO came to a value of more than £1.3M. Amanda Jones has joined the company as COO

After the end of the balance sheet date the group announced that it will be commencing a trial to launch Bargain Booze in Scotland with the Scottish Midland Co-operative Society as the exclusive Scottish franchisee. The trial is expected to be completed by June and if it proves successful stores will be rolled out across Scotland.

Christmas trading was decent with growth of 2.6% over last year and franchisees saw trade coming into their stores during the weeks when shoppers would have traditionally visited supermarkets, an indication of the increasing trend for shoppers to buy convenience and local. So far in the second half the group is trading in line with expectations and the decent trading over Christmas gives the board confidence for the rest of the year.

An interim dividend of 2p was declared which, when added to the final dividend of 6p represents an impressive yield of 6.4% at the current share price. Overall this was a bit of a disappointing update. Profits have not really made much progress but it is the cash flow that seems to be more problematic and the group just doesn’t seem to be churning off much cash. Sure, the dividend yield is very good but unless the operational cash flow can improve, I can’t see it being sustainable. There are some interesting ideas to expand with the BB Warehouse and the incursion into Scotland being the most exciting but until some progress is made on cash flow, I am waiting on the side lines here.

On the 20th January it was announced that Close Asset Management had purchased 186,460 shares at a value of about £290K to take their holding up to 5.2% of the total share capital. The transaction actually took place last November so this is not really recent news but it is a bit of a vote of confidence from them nonetheless.

On the 23rd January it was announced that Milton Group, relating to their multi cap income fund and diverse income trust had sold 1,253,309 shares worth more than £1.6M. They still own more than 9% of the total share capital but this is rather disappointing.

On the 29th January we saw another shareholder selling some of their shares with Henderson Global Investors selling 1,200,806 shares at a value of about £1.6M. The continue to hold 10.24% of the total equity but this is another disappointing sign.

On the 4th February it was announced that the group had purchased GT News for a net cash consideration of £6M. This does not include any net assets so this will probably all be in the form of goodwill. The acquired group has 37 stores in the East Midland and Yorkshire which the group expect to help drive logistics and marketing efficiencies. GT News made a profit of just £400K on revenues of £57M and management expect the acquisition to be earnings enhancing during the year ending 2016.

On the 16th February it was announced that Henderson had continued their sell off of the group with a sale of over one million shares valued at around £1.7M. This is a pretty huge sale and leaves them with 8.58% of the total share capital. Whether they have finished their sale if of course, the question.

On the 24th February it appeared that some of these large institutional sell offs had been purchased by Premier Fund Managers. With a 500,000 share purchase in January, and another 500,000 share purchase in February, they have spent about £1.4M on CVR shares so far this year to bring their total holdings up to 8.7%.

On the 11th May the group released a trading update covering the year ending 2015. Revenues are expected to be £364M, an increase from the £355.7M recorded last year despite the phasing of new store openings being later than expected and the continued heavy discounting and competition in the market. EBITDA is expected to be slightly ahead of market expectations and they expect to end the year with more than £1M of cash. Retail sales are in line with last year with like for like Bargain Booze sales down £1.7M and Wine Rack sales up just 0.1%. The year saw some 21 existing franchisees opening additional stores and 35 new franchisees joined the group with a good pipeline of stores during the next year.

To further support the franchisees, the group has invested in store fascias, modernised their brands and become more connected with their customers through use of social media and digital marketing. In April the Click and Collect service was piloted and the app, which launched in December, has already achieved over 19,500 downloads. Overall this is a decent update, but doesn’t really do much to excite.

On the same day the group also announced the appointment of Ian Jones as non-executive director. Ian has spent over 30 years in the retail industry and was previously retail director at Homebase, before which he served on the operating board of Sainsbury. He has apparently been involved with Conviviality since 2013, advising the board on supply chain and operational matters such as the reconfiguration of the Crew distribution centre and the decision to bring the transport function in house.