Telecom Plus has now released its interim results for the year ending 2015.

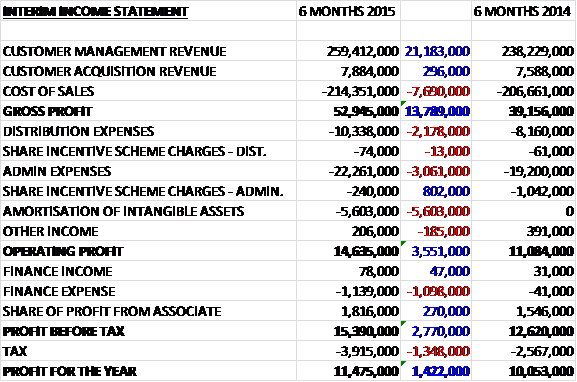

When compared to the first half of last year, revenues increased by £21.5M with an increase in the size of the customer base being partially offset by the impact of lower energy consumption due to the warm winter, with the smaller increase in cost of sales meaning that gross profit was £13.8M ahead of last year. Distribution expenses increased by £2.2M due to the increase in the number of services supplied and admin expenses were up £3.1M as the group continues to invest in headcount to support growth and despite a £5.6M amortisation of intangibles relating to the asset from the N Power deal the operating profit was £3.6M above that of last time. Finance expenses increased considerably and tax was up a similar amount to that the profit for the half year stood at £11.5M, an increase of £1.4M when compared to the first six months of last year.

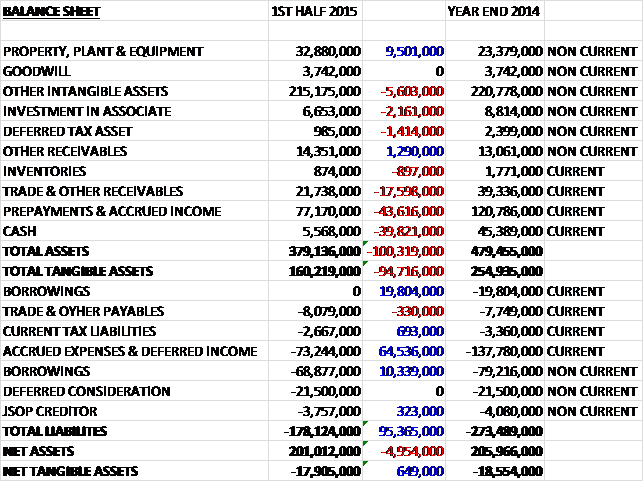

When compared to the end point of last year, total assets fell by £100.3M driven by a £43.6M decrease in prepayments & accrued income, a £39.8M decline in cash levels, a £17.6M fall in trade and other receivables, a £5.6M decline in intangible assets and a £2.2M fall in the value of the investment in the associate, partially offset by a £9.5M increase in property, plant and equipment relating to the refurbishment at the head office. Liabilities also fell during the period due to a £64.5M fall in accrued expenses and deferred income and a £30.2M fall in the level of borrowings. The end result is a small £649K increase in net tangible assets which still stand at a negative £17.9M.

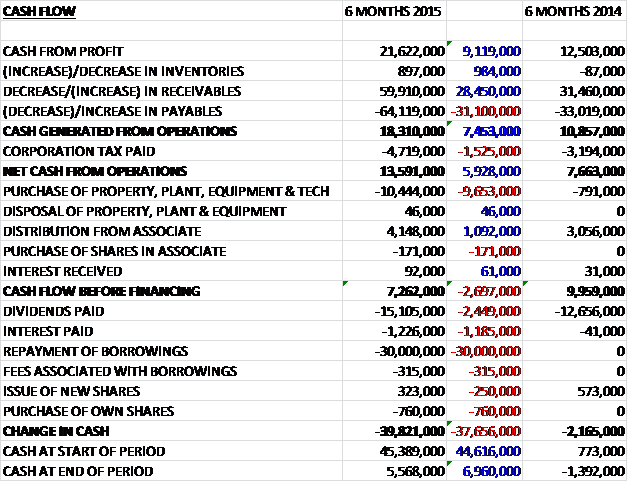

Before movements in working capital, cash profits increased by £9.1M to £21.6M but this was eroded somewhat by a fall in payables and after the increased tax payment the net cash from operations stood at £13.6M, an increase of £5.9M when compared to the first half of last year. The bulk of this was spent on property plant and equipment but due to the £4.1M dividend from the associate, the free cash flow stood at £7.3M, a small decline on last time due to the increased capital expenditure. Unfortunately this cash was not enough to pay for the £15.1M of dividends let alone the £30M loan repayment so that the net cash outflow for the period was a rather large £39.8M to give a cash level of just £5.6M at the end of the half, which probably won’t go that far.

During the period the number of customers grew by 34,733 and the number of services increased by 126,537 against a backdrop of a competitive market with independent energy suppliers enjoying a short term pricing advantage due to a combination of falling wholesale energy prices and not needing to make a full contribution towards certain social and environmental charges. In the telecoms market there has been heavy promotion from the big suppliers so it is pleasing to see that there was a net increase of 55,000 communications services and 61,000 energy services. About half of all the new customers applied for at least four core services and the group have seen a reduction in customer churn to under 1% per month. There are plans to introduce a number of initiatives, in particular the home mover processes which have the potential to further reduce churn in future.

The group have been recognised by Which as the UK’s best phone and broadband provider, and by Moneywise in their latest survey as the UK’s best energy provider for value and service which shows their continued prioritisation of customer service.

The Independent supplier of energy to business users, Opus, in which the group has a 20% interest made strong progress during the period with the number of electricity and gas sites growing to 179,614 and 25,832 respectively, representing a combined increase of more than 25% year on year. Turnover remains weighted to the second half of the year but despite the warm weather the business showed rapid organic growth with Telecom Plus’ share of the profits increasing by 17% to £1.8M. The board are confident that the outcome for the full year will be significantly ahead of the record profits last year.

The group continue to provide further incentives to their distributers with the subsidised branded Mini being taken by 650 partners and 10,000 tablets in circulation. During the year the group paid a tranche of the loan off early and extended the maturity of the rest so that there is now £70M to be paid with no payments now due until December 2015. They also extended the working capital facility from £25M to £40M despite not yet drawing down against it.

Although revenues are susceptible to warmer weather reducing the usage of gas, apparently the recently signed deal with N Power means that the group do not suffer a material impact on profitability, which is something I do not really understand. There is no doubt that the sector is facing a period of uncertainty with the upcoming election and political concern over rising energy prices may lead to further reviews of the energy market that could result in further consumer protection legislation being introduced and in the worst case scenario, the energy market could be renationalised under certain election outcomes. Disappointingly the board have signalled their intention to stop providing interim management statements and instead intent to update the market on progress on an event driven basis which is a step backwards in my view.

Going forward, management are confident that the group will deliver record revenues, profits and EPS for the current year. The group are currently not looking to enter the TV space due to the confusing market outlook and scepticism over whether this service will ever offer an attractive commercial opportunity that can sensibly be harnessed. They are looking at insurance and the provision of boiler cover, however. Similarly they are interested in providing water services with that market opening up to competition in 2017, although this is currently only going to include the supply to business customers with a further opening up probably dependent on the outcome of the election.

After a 19% increase in the interim dividend, at the current share price they are yielding 3.7%, increasing to 3.8% by the year end with the board spelling out their intention to pay a total dividend of 40p for the year and thereafter returning to the historic level of 75% of adjusted EPS despite the debt and the £21.5M of deferred consideration due to N Power in December 2016. Net debt stood at £84.8M at the end of the period compared to £75.1M at the end point of last year reflecting the office refurbishment, but it is still disappointing to see little progress made in reducing this.

Overall then, this is a decent update. Profits are up again with the board expecting record profits for the year as a whole and net tangible assets are creeping up slowly but remain negative. There is a positive operational cash flow this half year with a free cash flow of £7.3M but this does not go near to paying for the £15.1M of dividends and the £30M loan repayment. The renegotiation of the loan terms are helpful but there is still going to have to be a £70M payment after the year end and the deferred consideration is still lurking with £21.5M needing to be paid in 2016. The £40M of working capital facilities will probably have to be utilised to help out with this. The dividend yield of 3.8% is certainly decent but with the election just round the corner I fell the sensible option would be to wait and see what the outcome is with a Labour/SNP coalition possibly re-nationalising the energy industry which would clearly be a disaster for the group.

The chart shows that the share price has been on a decline for at least a year – I am not going to be investing in a chart that looks like this.

On the 16th April the group released a trading update covering the year ending 2015. There were very satisfactory levels of growth during the first half of the year in both customer and service numbers but this was followed by a much weaker Q3 and some improvement in Q4. This was partly due to some headwinds as established suppliers who had hedged against changes in energy price suffered when compared to new independent suppliers benefitting from substantially lower wholesale commodity prices. The group have now moved to a new head office in North London and have introduced changes to their offering in order to attract a higher quality customer in order to obtain better revenues per member, lower churn and reduce levels of bad debt.

The majority of customer invoices are prepared using estimated meter readings which gives rise to timing differences between the estimated volumes of energy invoiced to customers and the actual volume invoiced to the company by energy industry system operators, which contributes to the unbilled energy debtor carried forward on the balance sheet. After a recent assessment of the accuracy of the estimates, it has been shown that leakage and theft within the gas industry which will not be billable to customers, has been running at a higher rate than previously expected. This will have a negative balance sheet impact of £11M and for future periods, provision against leakage and theft is expected to reduce gas revenues between 2% and 3%. Due to the more sophisticated way that wholesale costs are reconciled to actual customer meter readings by electricity system operators, the impact is not significant in this market.

Although this is not a cash hit, it is concerning that this has been happening since 2007 as it seems strange that it has not been flagged up before now. It is also a concern that the group are looking to re-state previous year figures as opposed to taking the hit to profits this year which may be a bit misleading. For the year as a whole, adjusted pre-tax profit is likely to come in at £52M to £53M, affected by the above issue with theft, along with retail energy price reductions and lower energy usage during a warm year. The board are recommending a final dividend of 21p a share which corresponds to an annual yield of 4.9%, which is certainly not too bad.

Going forward, the board does not believe that the unfavourable conditions that have prevailed this year will go on indefinitely and they expect the gas between the standard variable tariffs currently paid by most customers and the cheaper introductory short-term fixed tariffs available to new customers will start to narrow during the year which should enable to the group to deliver decent organic growth in the number of customers using their service of between 40,000 to 60,000 during the year with an estimated adjusted pre-tax profit next year in the region of £54M and £58M which means that the dividend could be increased to yield some 5.6%.

This update is no doubt disappointing but management do seem to think that further progress will be made next year and that dividend yield is starting to look enticing – I will keep an eye on these shares for now.