Creston is an agency group providing clients with strategic marketing and brand consultancy services. The group as a whole seems to be very technology oriented and is focused on helping their clients with their digital marketing, social media and PR. The Communications division offers marketing and communications strategy including advertising, brand strategy, channel marketing, CRM, digital marketing, direct marketing, local marketing, social media marketing and PR. The Health division provides communications solutions to the healthcare and pharmaceutical sector, offering advertising, advocacy, brand consulting, digital and direct marketing, PR, reputational management and medical education. The Insight division performs market research services using face to face, telephone and online data collection techniques. Creston has now released its final results for the year ending 2014.

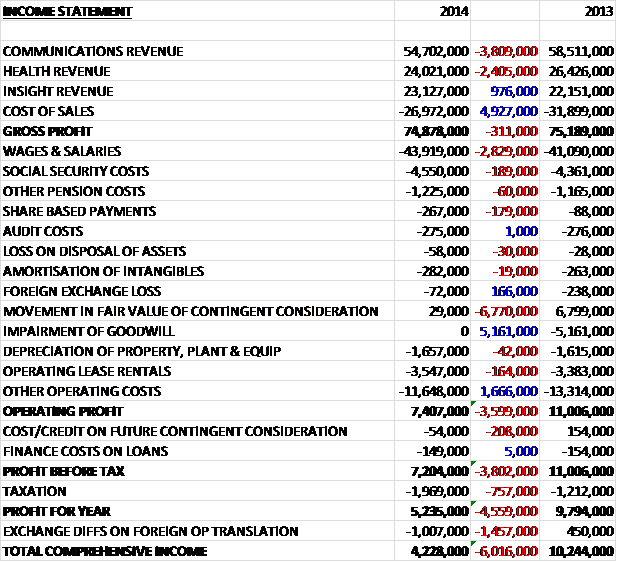

Overall revenues fell as communications sales fell by £3.8M and health sales reduced by £2.4M. Cost of sales also fell during the year to give a gross profit some £311K lower. We then see an increase in wages, partially offset by a fall in other operating costs with the big changes in one-off items being a £6.8M reduction in the movement of the fair value of continent consideration and the lack of a £5.2M impairment of goodwill that occurred last year. The end result is an operating profit of £7.4M, a £3.6M decline when compared to 2013. There was then a small cost relating to future contingent consideration and in increase in tax, partly due to the £1.7M release of a provision last year following the conclusion of an HMRC enquiry into deductibility of goodwill that was written off when a previous subsidiary ceased trading, and partly due to a higher rate of tax incurred on the group’s US operations so that the profit for the year fell by £4.6M to £5.2M.

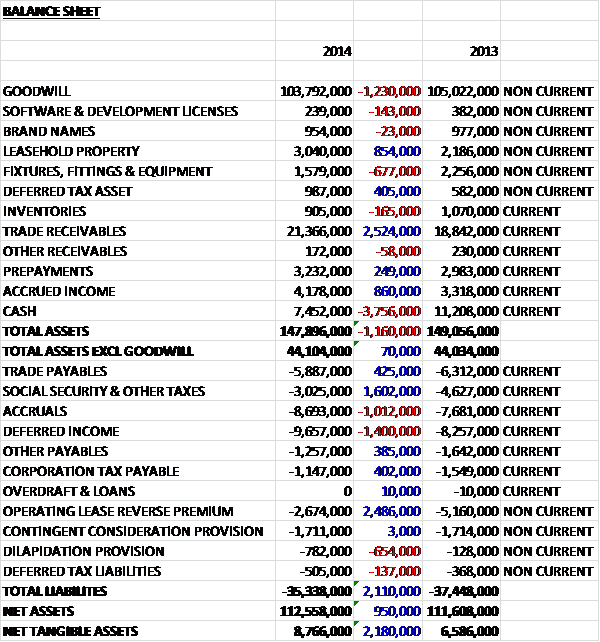

When compared to the end point of last year, total assets declined by £1.2M driven by a £3.8M fall in cash levels and a £1.3M decline in goodwill, somewhat offset by a £2.5M increase in trade receivables, an £860K growth in accrued income and an £854K growth in the value of leasehold properties. Total liabilities also fell during the year with a £2.5M decline in the operating lease reverse premium and a £1.6M fall in social security and other tax payables, partially offset by a £1.4M increase in deferred income liabilities and a £1M growth in accrued liabilities. When we take out goodwill, the net asset base is £8.8M, a £2.2M improvement on the figure last year. It is worth noting that there are £21.6M worth of operating lease payables off the balance sheet, mostly relating to the head office, which seems quite substantial given the net tangible asset level.

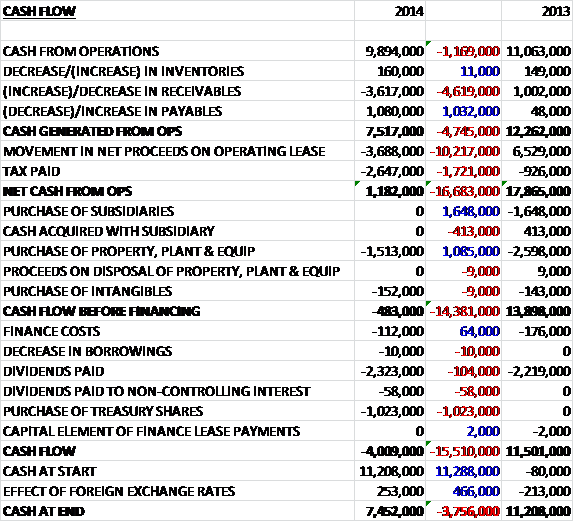

Before movements in working capital, cash profits fell by £1.2M to £9.9M before this was dragged down further by an increase in receivables which reflects a more normal working capital position so that operational cash flow before cash and operating lease changes was some £4.7M lower at £7.5M. This was eroded further by the £3.7M spent on operating leases (the cash to pay for this was received last year, hence the difference from last year) and the increased tax paid so that net cash from operations was just £1.2M. This was not quite enough to pay for the £1.7M worth of capital expenditure so there was a negative free cash flow of £483K. The group then spent $2.3M on dividends and £1M on the purchase of treasury shares so that there was a £4M cash outflow for the year to give a healthy cash level of £7.5M at the year end.

The small decline in revenue was a result of a busy first half spent pitching for new business plus some client volatility but wins filtered through in the second half of the year with £8.6M in net new business wins contributing to a second half growth of 3%. This increase in pitching activity and increased property costs affected profits which accounts for the small decline seen but the very high level of new business wins almost offset the first half shortfall.

Profit at the communications division was £5.6M, a decline of £600K when compared to last year as a result of the lower revenue and increased property costs and the investment in new business activity during the first half of the year. There is a generally positive sentiment across the sectors in which the business operates in with the latest Bellwether report being the most positive in seven years in the industry and more specifically social, data, mobile, customer experience, content marketing, multi-channel and personalisation have been noted as the biggest areas of opportunity. The major shifts in the market with regards to the move towards digital marketing have not gone unnoticed by legacy advertising agencies which may increase competition in the arena, although Creston does seem to be particularly in tune with the ever changing digital market.

During the year work included the development of a new platform for automotive dealer marketing portals and new mobile apps for Danone, while the group is also engaged on a programme in partnership with The Bakery. This programme enables them to tap into over 400 young technology companies around the world and the business is well into the process of developing technology driven brand solutions for Danone, Unilever and Public Health England in this way with three other major brands at the start of this process. New business wins during the year included Arthritis Research UK, Bentley, HSBC, Sky and Virgin Trains, along with additional brands from Unilever. Significant work during the year included the Durex Earth Hour campaign which achieved 85 million video views across more than 50 countries within a few weeks. There were also notable projects with the Playstation 4 launch, which included the PS4 branded OXO tower stunt.

During the next year, the primary focus will be to establish and embed the new client relationships that were achieved during this year. Following the spree during the first half of the year, the group will now concentrate on fewer, selected pitches to improve conversion and not allow this activity to impact the current service levels to existing clients. Internationally, the business is looking to grow through partnerships, joint ventures and acquisitions. Going forward, with a strong new business performance at the end of last year, the division is expected to make a stronger start to this year. The new business pipeline remains strong but while the level of market activity continues to increase, management remains cautious as volatility still exists within budgets.

Profit at the health division was £4M, a fall of £2.7M when compared to 2013 driven by the loss of the US Sanofi business in Q4 last year, partially offset by the UK health companies performing well with like for like revenue growth of 5% and continued growth of the digital healthcare agency DJM, acquired in the second half of 2013. These factors are showed by a 44% decline in headline in profit and a 22% increase in the second half of the year. During the year the group has seen the shape of agency procurement change with rostered agency numbers being reduced and the emphasis being on cost cutting putting significant pressure on profits. In the UK cost constraints will continue following the Pharmaceutical Price Regulation Scheme which means the industry may have to reshape itself yet again to generate growth.

In the US enrolment into health insurance exchanges began expanding public and private health care coverage which means that payers are more often the key decision makers rather than doctors or patients and direct to consumer advertising has undergone closer scrutiny and companies have reduced medical education budgets. This has led to a period of uncertainty for pharmaceutical marketers but the opportunity to reach more insured people in the US means there is a wider audience to communicate with. During the year the group launched Chemia, a new network covering creative, PR and digital government relations and medical education; and Liberation, a conflict PR agency. Additionally, Looped was launched which is a brand and creative consultancy.

New business wins during the year included the WHO, MSD, Takeda, Alere, GAVI Alliance, Novartis, UN WSSCC and further Gilead brands. After the period end, the business also won a contract with Cow and Gate as a result of a referral from the Communications business which is something than management are really trying to push going forward. Future growth is seen to come from continuing technological innovations such as the new health kit from Apple that means patients don’t need to visit their GP to have their routine monitoring done which creates an opportunity for the industry to move towards more personalised medicine and the communications to support this type of technology, including educating both doctors and patients, will become a new specialist area. Another area that the business is looking to exploit is getting involved earlier in the pre-licencing process for emerging medicines.

Profit at the insight division was £1.7M, an increase of £300K when compared to last year with growth coming from both revenue growth and the realigning of the cost base. For the first time since 2008, the general trading environment across market research in the UK and internationally showed signs of improvement but trading levels remained well below those before the recession. For ICM the period represented a recovery following the structural changes undertaken last year and growth was seen from existing customers such as Aviva and Vodafone, along with the addition of new clients including the British Chambers of Commerce and HM Passport Office. Marketing Sciences enjoyed a good year of growth driven by increased client relationships with Tesco, Danone, Igloo, Kimberley Clark, Velux and Reckitt Benckiser. Post year end, the group acquired Walnut, a recent start-up specialising in neuroscience for £100K and the business will continue to innovate in neuroscience and the measurement of emotions.

The annual report contains some examples of the work that the group does which I think gives a better understanding of what some of the contracts involve. One was to help the Crown Commercial Service reach and engage audiences around serious topics. In order to achieve this the group collaborated between different agencies and external partners utilising market research, websites, localised media campaigns, social media and direct mail with each campaign being tailored to the specific target audience. This resulted in increased traffic to websites, increased calls to contact centres and significant amounts of press coverage leading to behavioural change and a growing knowledge of the issues being promoted.

Another project was conducted on behalf of Reckitt brand Durex. They wanted to create a campaign that would generate over 100 million engagements whilst taking a more emotional positon on sex and love and whilst it could be naughty and cheeky, it also had to show the brand’s mature side and be on a global scale. The group created a series of Facebook posts and a short film suggesting that the Earth Hour was the ideal time for couples to escape the screen and have some fun in the dark, ironically using Facebook, Youtube and Twitter to spread the message. The campaign achieved nearly 2 billion impressions worldwide and successfully promoted the Durex brand globally.

The group also worked with the WHO who wanted to highlight the increasing threat of vector-borne diseases with the slogan “Small Bite: Big Threat”. Two Creston health businesses worked with the organisation to develop two campaign posters, an infographic and a policy document which were shared with over 150 country offices globally to raise awareness and drive action locally. The team also created a stand at Heathrow. The campaign was a success and the materials attracted attention from the UN and Centres for Disease Control and Prevention.

The group worked with Canon Europe to develop a B2B campaign to reinforce perceptions of Canon as a business services partner. The idea was that by getting to know their customers better to provide the insights and vision that will support businesses that strive to be exceptional. The group developed assets from print and digital display through to insight based content such as articles and white papers and in addition, a central content hub was established online to be stocked with fresh insights and engaging content over the course of the campaign.

During the year the group moved to a new head office in London which incurred £900K of costs incurred during the vacant period of Creston House when the group paid double rent, rates and service charges and £500K relating to move costs, and double charges on existing leases. Last year the group received £7.2M on signing the lease relating to a reverse premium and agreed dilapidation obligations, of which £3.7M was used this year to fulfil the dilapidation obligation. Last year we also saw some one-off charges relating to the earlier acquisition of Cooney Waters. Management decided that the future performance of the group would not be as good as initially expected which had the effect of reducing the contingent consideration likely to be paid by £6.8M which had the knock on effect of impairing goodwill to the tune of £5.2M. The remaining provision for contingent considerations stands at £1.7M which will be settled in July 2015 and 2016.

One strategic objective that was achieved during the year was the completion of the so called Co-location strategy where all London subsidiaries moved into the Creston House which is designed to improve collaboration between the different divisions which seems to be a clear strategy being adopted by the group, and of course to save on the overheads of having many fragmented offices spread around the city. The board have also mentioned a share buyback scheme in which up to £2M of shares will be acquired by group subject to being available at an appropriate price which should give the share price some support going forward.

The group seems to have some good headroom. There are currently no borrowings but there is a revolving credit facility of £20M that is currently undrawn and expires at the end of September 2015 although the group did pay £100K in non-utilisation fees.

The group is somewhat susceptible to exchange rate changes with a 10% strengthening of Sterling against the Euro leading to a £135K fall in profits whereas a 10% weakening against the Dollar would reduce profits by £170K. Other risks include the fact that this is a fast paced industry with relatively low barriers of entry that may encourage greater competition, the fact that the loss of a big client may materially impact performance, as seen with the Sanofi loss at the end of last year and the possibility of turbulence in the macro-economic environment may affect client budgets and performance. The challenging market place impacted the small healthcare research consultancy, Vitaris which failed to achieve critical mass and was closed during the year at a cost of £400K.

One of the group’s shareholders is David Marshall of Western Selection. I have encountered him before at Swallowfield and Western Selection like to get involved in the running of the companies in which they are invested and as such David is a non-executive director at the company. At the year-end CEO Don Elgie retired after spending 13 years as CEO and founding the group in 2001 who was succeeded by current CFO Barrie Brien, and Chairman David Grigson will step down from the board after more than four year in the job at the next AGM and will be succeeded by Richard Huntingford who has been a member of the board since 2011. After the year-end, Kathryn Herrick was appointed new CFO so this has been a real period of change for the board.

Going forward, the coming year will be one of investment in realigning the business under a unified group offer and while they remain cautious about the state of the broader macro-economic environment and the potential for it to affect client budgets, the board are confident that over the medium term the new strategy will enable them to deliver higher rates of growth over the medium term.

At the current share price the shares trade on a fair value P/E ratio of 13.7 but this falls to a cheap looking 9.4 on next year’s forecast. After a 6% increase, the shares are currently yielding a dividend of 3.3% which increases to 3.5% on next year’s prediction. At the year end the group had a net cash position of £5.7M compared to £9.5M at this point last year.

Overall then, this seemed like a slightly disappointing set of results. Profits fell during the year and despite improvements to net assets, the balance sheet still does not look that strong. The cash flow performance was also disappointing with a falling operating cash flow and no free cash flow. Performance in the second half of the year did improve however, with the poor first half performance, partly due to the loss of the US Sanofi contract, dragging the year down as a whole. There is apparently positive sentiment in the market but Creston does not really seem to be benefiting from this, possible as competition increases and clients are still looking to cut budgets.

The strategy to increase cross selling seems to be baring some fruit but the move to the new head office seems to be generating quite a few costs with a lot of double payment of rent and rates as some of the legacy offices are obviously still being used. This year has also seen some upheaval at the board level with the founder and CEO stepping aside to let the Finance Director take over. Going forward, this year is apparently going to be one of investment, which I guess means higher costs but the performance in the first half is likely to be better than a week comparator in 2014. In conclusion, I like the digital focus for the group but I still have some reservations about performance at the moment.