GSK have now released their Q1 results for the year ending 2015.

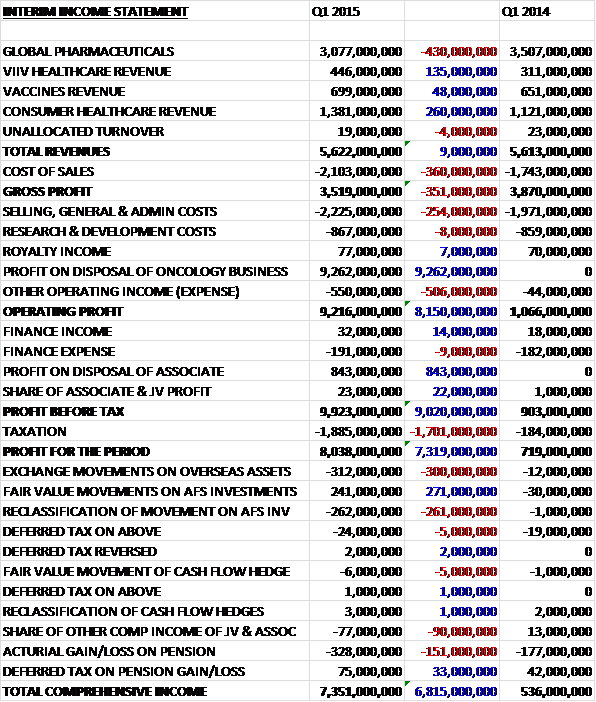

Overall revenues were broadly flat when compared to Q1 last year as a £430M decline in global pharmaceutical revenue was offset by a £260M increase in consumer healthcare sales and a £135M growth in ViiV Healthcare revenue. Cost of sales increased, however, to give a gross profit some £351M lower than last time. Other costs also increased with other operating expenses going up too, but this was vastly counteracted by the £9.3BN profit made on the sale of the oncology business. The group also made £843M on the disposal of an associate but the tax bill was some £1.701BN higher due to the profits on these disposals which gave a profit for the quarter some £7.319BN higher at £8.038BN. Core EPS for the quarter fell by 16% to 17.3p.

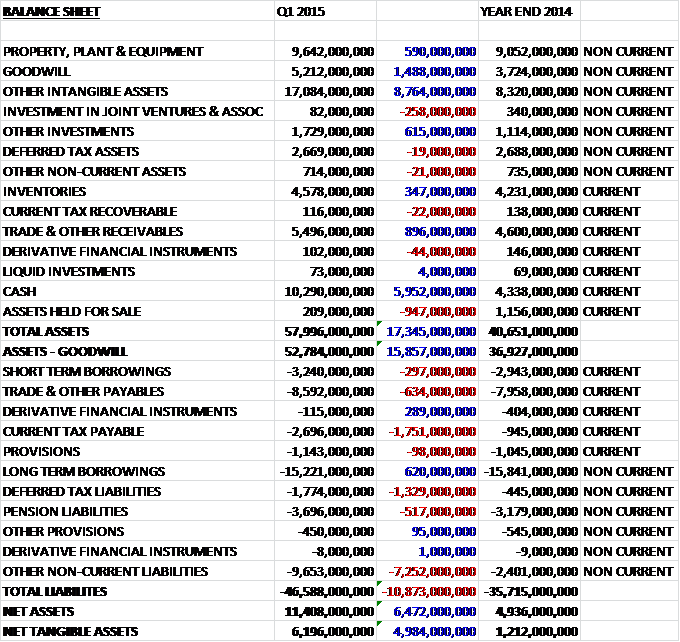

When compared to the end of last year, total assets increased by an incredible £17.345BN. This was driven by an £8.764BN increase in intangible assets, a £5.952BN growth in cash, a £1.488BN increase in goodwill and an £896M increase in receivables, somewhat offset by the £947M fall in assets held for sale (obviously converted into cash). Liabilities also increased during the period as a £7.252BN increase in “other” non-current liabilities which relates to the potential requirement to purchase the minority stakes in the joint ventures, a £1.751BN growth in current tax payable, a £1.329BN increase in deferred tax liabilities and a £634M growth in payables was partially offset by a £620M decline in long term borrowings to vive a net tangible asset level of £6.196BN, an increase of nearly £5BN and a much healthier looking balance sheet after the Novartis transaction.

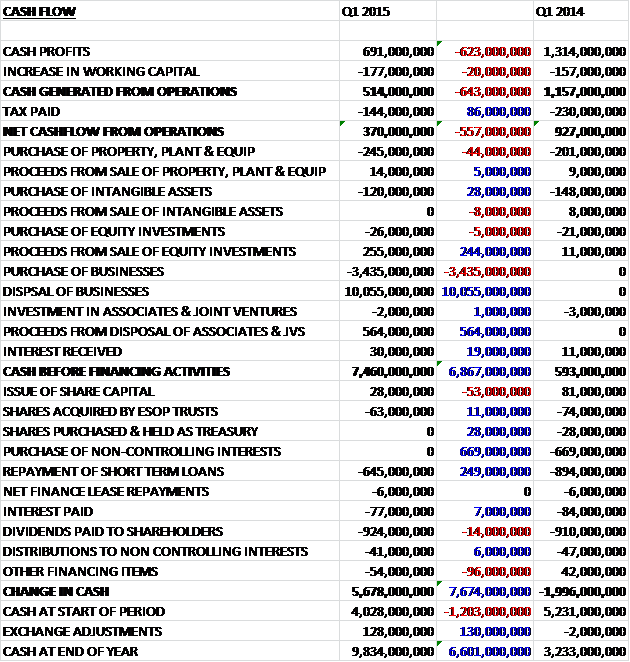

Before movements in in working capital, cash profits nearly halved to £691M when compared to the first quarter of last year. An increase in working capital, principally due to the inventory acquired from the former Novartis vaccine business, and a lower amount of tax paid meant that the net cash flow from operations stood at £370M for the quarter, a fall of £557M. The group was still free cash flow positive during the quarter, though, with a net £231M spent on tangible assets and £120M on intangibles. The cash flow was really affected by the Novartis deal, however, with a net £6.62BN being received from the purchase and sale of businesses. On top of this, there was also £564M brought in from the disposal of joint ventures and £255M from the sale of equity investments which meant that before financing, the cash flow was a massive £7.46BN. The group used £645M to repay some loans and £924M was distributed to shareholders as dividends but this still left a cash flow for the quarter of some £5.678BN to leave a cash pile of £9.834BN, although it is worth noting that the tax bill arising from the disposal is yet to be paid.

Core operating profit in global pharmaceuticals fell by 20% to £1.256BN. Respiratory sales declined by 9% to £1.408BN. In the US they were down 22% which reflected a 1% volume growth counteracted by a 23% negative impact on pricing, reflecting new contracts agreed in 2014 in response to competitive pressure in markets where Advair and Breo Ellipta compete. Sales of Advair were down 21%, Flovent sales fell by 38% and Ventolin sales were down 24%. The falls in sales of the latter two reflect the net negative impact of true up adjustments to accruals for returns and rebates, excluding the impact of this, sales were down 6% for Flovent whilst Ventolin underlying sales grew by 13%. Breo Ellipta recorded sales of £14M whilst Anoro Ellipta, launched in Q2 2014, recorded sales of £9M.

European respiratory sales were down 4% to £392M with seratide sales down 11%, reflecting increasing competitive pressures and the transition of the portfolio to the newer products. Relvar Ellipta, approved for both COPD and asthma, recorded sales of £16M whilst Anoro Ellipta, with launches now underway in many countries throughout the region, recorded sales of £2M. Respiratory sales in the international region grew by 5% to £433M with emerging markets up 7% and Japan up 1%. In Emerging markets, sales of Seretide increased by 6% while Ventolin grew by 8%. In Japan sales of Relvar Ellipta of £9M, together with strong growth in Veramyst and Xyzal more than offset the 27% decline in Adoair due to a strong comparison in Q1 last year.

Oncology sales for the first two months of the year were down by 18% to £216M. Sales in cardiovascular, metabolic and urology drugs fell 8% to £218M. The Avodart franchise fell by 7% with 13% growth in Duodart offset by a 15% decline in Avodart. Sales of Prolia fell by 33% due to the agreement in Q2 last year to terminate the joint commercialisation with Amgen in several European markets, Russia and Mexico. Immuno-inflammation sales grew 19% to £60M with Benlysta by far the largest contributor. Sales in other therapy areas fell 9% to £525M. Augmentin sales declined 3% and dermatology sales fell by 11%, with both being impacted by supply constraints due to capacity limitations. Relenza sales were down 25% reflecting Japanese government stockpiling in Q1 last year which was not repeated this year and sales of rare disease products fell by 10% as a result of generic competition to Mepron in the US.

Established product turnover fell by 20% to £650M. Sales in the US were down 42%, primarily due to a 75% fall in Lovaza sales due to generic competition. Europe was down 14% with Seroxat sales falling 33%, reflecting increased generic competition and international sales were down 8% reflecting lower sales of Seroxat in Japn due to generic competition and supply constraints and the impact of price pressures to Zeffix and Hepsera in China. Core operating profit in ViiV Healthcare increased by 55% to £318M with sales increasing 42% to £446M with the US up 66%, Europe up 35% and international up 9%. The ongoing roll-out of Tivicay resulted in sales of £112M and Triumeq, now launched in the US and Europe recorded sales of £81M. Epzicom, which benefited from use in combination with Tivicay, increased by 2% but Selzentry sales fell by 9%. There were also continued declines in the mature portfolio, mainly driven by generic competition to Combivir and Lexiva.

Core operating profit in vaccines fell by 31% to £161M but sales grew by 10% to £699M. In the US, reported growth of 14% reflected strong growth in Hepatitis vaccines which benefited from variations in CDC stockpile shipments and the replenishment of wholesaler inventory levels. Rotarix, up 12%, also benefited from the replenishment of wholesaler stock levels but this growth was partially offset by lower sales of Infanrix due to the return to the market of a competitor. In Europe sales grew by 4% on a reported basis but fell on a pro-forma basis due to a 9% fall in Infanrix which was impacted by the introduction of a competitor vaccine in 2014 and the phasing of shipments in some countries. Sales of hepatitis vaccines fell by 4% and Cervarix sales were down 27%, partly due to the phasing of shipments. These declines were partly offset by a 27% increase in Boostrix sales driven by better supply in comparison with Q1 last year. International sales grew by 13% on a reported basis and 3% pro-forma, benefiting from the phasing of shipments of a number of products. Synflorix sales grew 12% as a result of phasing, and hepatitis vaccines grew by 20% driven by the phasing of orders in the Middle East, but Boostrix sales fell 25% reflecting the phasing of orders in Brazil and the Middle East and Fluarix sales were down 75% due to the phasing of shipments in Brazil and Asia Pacific.

Core operating profit in consumer healthcare increased by 53% to £182M with sales up 24% to £1.381BN, benefiting significantly from the first month’s sales of the former Novartis products. On a pro-forma basis, growth was 8% reflecting the strong launch of Flonase OTC in the US. Other launches during the period included Fenbid Chewable in China, Sensodyne Repair and Protect Whitening in the US and Germany, and the rollout of Sensodyne mouthwash. US sales grew by 47% with Flonase being the main driver, holding an 11% market share after just 10 weeks from launch. Oral Health sales gave a strong performance with growth of 14%, driven by Sensodyne. Skin Health also delivered strong growth, aided by 27% growth of Abreva, boosted by stocking patterns but Tums supply suffered some disruption to stocking supply during the quarter.

Sales in Europe were up 32% with oral health doing well, reflecting strong performances from both Sensodyne and Aquafresh following an improved supply position, new advertising in key markets and the roll out of Sensodyne True White in the UK. Wellness also showed growth as regional respiratory brands Beechams and Coldrex benefited from a stronger cold and flu season but nutrition and skin health both saw sales decline reflecting disruption from stocking patterns and some supply shortages. International sales grew by 12% with China, India and Turkey all showing double digit increases to sales, in particular in oral and skin health. Wellness growth was impacted by a decline in Panadol sales due to a challenging competitive market in Australia and a tough comparator quarter in Latin America following supply improvements last year. In nutrition, Horlicks was up 4% with strong consumption growth in India partially offset by some retailer destocking.

Sales of products launched in the last five years accounted for £303M with particularly strong contributions from Tivicay and Triumeq in ViiV, a solid increase in Benlysta sales in immune-inflammation and the more than doubling of Relvar/Breo Ellipta sales to £41M in respiratory.

There are still a lot of potential drugs in the pipeline with around 40 in phase two and three development. In vaccines, the group acquired meningitis prevention Bexsero and Menveo which are both expected to contribute to profits. There is also a decent opportunity for Shingrix, the Shingles vaccine that recently published phase three data that demonstrated overall efficacy of over 97% and there are more than 20 new vaccines in development including potential protection against hepatitis C, RSV, typhoid, Group B Strep and MenABCWY (whatever that is!), Within pharmaceuticals, the company continues to expect to see declines in sales of Advair but due to new products, respiratory sales are expected to return to growth in 2016 with levels at or above current sales by 2020, which seems like quite a long time.

In HIV treatment, the recent launches of Tivicay and Triumeq have surpassed expectations and there is clear scope to develop multiple dolutegravir based regiments for the treatment of the disease over the next few years. Progress has been made to develop ViiV’s pipeline with several promising assets in development. Due to this improvement in prospects, the group has decided that it will retain its full existing holding and will now not be initiating an IPO of a minority stake in contrast to what was reported previously.

The group now has three major restructuring programmes underway: the transaction integration, restructure of its global pharmaceuticals business and the group-wide major change programme started in 2012. The group continues to expect to deliver £1BN of annual synergies following the Novartis transaction and has now identified opportunities to accelerate the delivery of the programme. As a result, over half of the total savings are now expected in 2016 with the programme expected to be mostly complete in 2017, two years earlier than initially thought. In Consumer Healthcare, cost savings of £400M are being targeted with a similar amount expected in vaccines where it has become clear that the acquired group has higher operating costs than initially expected.

The restructuring of the global pharmaceuticals business is expected to deliver about £1BN of annual cost savings to be delivered by 2017 with approximately half due next year which should mitigate ongoing changes to the pharmaceutical margin and support investment in recent and new launches. In total then, the group expects all restructuring to deliver annual cost savings of £3BN with total cash charges expected to be £3.65BN with non-cash charges of £1.35BN. So far, the group has paid out £1.3BN, mostly in cash relating to these changes. The majority of the restructuring is expected to be complete by 2017 and going forward, it will be simplified into one single programme.

Apparently in certain circumstances, Novartis has the right to require GSK to purchase its 36.5% shareholding in the Consumer Healthcare joint venture at a market based valuation. This right is exercisable from 2018 to 2035. As a result, there is an “other” liability of £6.204BN to cover this. Equally, the other shareholders in the ViiV Healthcare joint venture have a similar clause with Pfizer having the option to request an IPO for its 11.7% stake and Shinogi having the option for GSK to acquire its 10% shareholding in 2017, 2020 or 2022.

As already reported upon, GSK and Novartis have contributed their respective Consumer Healthcare businesses into a joint venture in a non-cash transaction. GSK has an interest of 63.5% and majority control. In addition, GSK acquired Novartis’ global vaccines business for an initial consideration of $5.25BN with potential milestone payments of up to $1.8BN, the first of which saw them pay Novartis $450M in March. The final part of the deal involved the divesting of GSK’s Oncology business for a consideration of £10.4BN with the profit on disposal after tax hitting £7.342BN.

It is notable that the board have changed their allocation of the funds from the Novartis transaction, reducing the amount that is being returned to shareholders. This is because the pricing environment is becoming more difficult and there are a number of situations where either much less cash will be coming in to the group or they will have to pay out a great deal of cash. These include the above mentioned put options of the partners in the ViiV healthcare and Consumer Healthcare business and the possible introduction of generic Advair in the US. This year there are a number of headwinds that include the dilutive effect of the transaction and continuation of the issues that faced the group at the end of 2014. Following this year, it is expected that performance will improve with revenues and earnings expected to grow from 2016 to 2020.

As already mentioned, the group are looking to prioritise the use of cash to prop up the level of ordinary dividends during a period of falling profits, and to invest in more rapid delivery of synergy benefits and growth opportunities. As such, the group have announced that it will pay dividends of 80p per annum for the next three years and to return 20p per share to shareholders in a special dividend in Q4 as a result of the cash received from Novartis, which is substantially less than originally mooted.

Going forward, core EPS in 2015 is expected to decline at a rate in the high teens on a constant currency basis, primarily due to pricing pressure in Advair, the dilutive effect of the transaction and the inherited cost base of the Novartis businesses. In 2016, there should be a significant recovery in core EPS with a double digit percentage growth as the headwinds experienced this year diminish and the synergy benefits of the transaction contribute more meaningfully. From 2016 to 2020 the compound annual growth rate is expected to be in the low to mid-single digits with vaccines growing at mid to high single digits, consumer healthcare growing at a rate of mid-single digits and pharmaceuticals growing at low single digits. The introduction of generic competition to Advair has been factored in to this analysis but there is no assumption of premature loss to any of the other key products and includes contribution from mepoluzimab and Shingrix that are currently in the pipeline stage.

Due to the deal with Novartis, net debt at the end of the quarter stood at £8.098BN, a vast improvement from the £14.377BN at the end of last year and the £13.66BN at the same period last year. The group has declared an unchanged Q1 dividend of 19p (compared to Q1 last year) and the 80p announced for the year represents a yield of 5.5% at the current share price which seems pretty decent.

Seretide/Advair is still by far the largest drug by sales, at £898M with a number of others hovering around the 180M mark, including Avodart, Infanrix, and Epzicom, all of which haven’t changed much year on year. This remains the basic problem with GSK, for some time now they have been reliant on one drug and now we see that in their largest market, pricing pressures are underway that could seriously undermine earnings going forward and the replacement drugs, Bero and Anoro Ellipta are clearly still in their infancy despite having promise. Having said that, the Novartis deal really shores up the balance sheet and the retention of a lot of the capital from this deal is probably a sensible idea; ViiV healthcare seems to be doing very well and drugs Tivicay and Triumeq seem as though they could be real earners for the group. In addition the 5.5% dividend yield should underpin the share price despite the year of decline that the group is no doubt entering. A decision on this company is quite difficult for me, I have sold a portion of my holding by retain some shares which were supposed to add some ballast to my portfolio.

On the 7th May the group announced that Manvinder Singh Banga will join as non-executive director. He will succeed Deryck Maughan. Manvinder previously worked as president of global foods, home and personal care at Unilever and is currently also a non-executive director at M&S and Thomson Reuters.

The decline in the share price has clearly set in and there does not seem many signs of a reversal. I am sorely tempted to sell out here completely.

On the 22nd June the group announced the divestment of its meningitis vaccines Nimenrix and Mencevax to Pfitzer for a total consideration of £82M including some deferred consideration. These two vaccines are sold outside the US and had sales of £34M in 2014. The divestment became necessary due to competition concerns following the acquisition of meningitis vaccines Menveo and Bexsero from Novartis.