Character is engaged in the design, development and international distribution of toys, games and gifts. They are listed on the AIM exchange and have now released their final results for the year ending 2014.

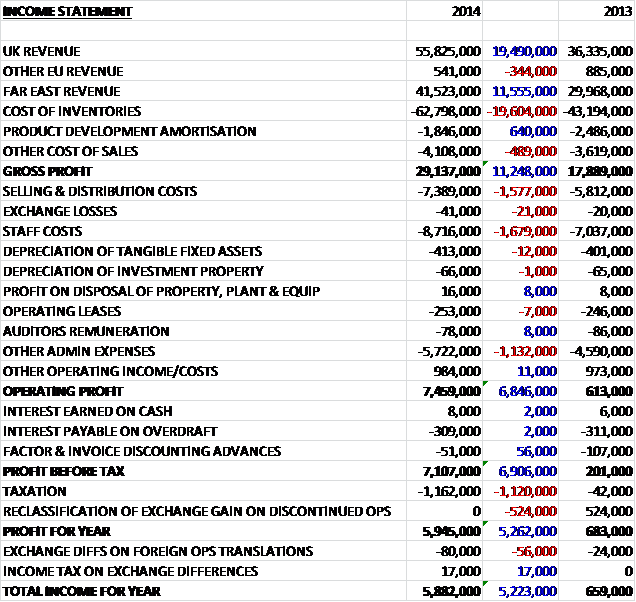

Overall revenues increased considerably as growth in UK and Far East sales was only partially offset by a decline in other European revenue. Cost of inventories also increased to give a gross profit some £11.2M ahead of last year. We then see a £1.6M increase in selling and distribution costs, a £1.7M growth in staff costs and a £1.1M increase in other admin expenses to give an operating profit £6.8M above that of 2013. We then see a halving of factor and invoice discounting advances (whatever they are) but also a £1.2M increase in tax and the lack of a £524K positive reclassification of exchange gain on discontinued operations that occurred last year. In all, the group made a profit for the year of £5.9M, an increase of £5.3M year on year.

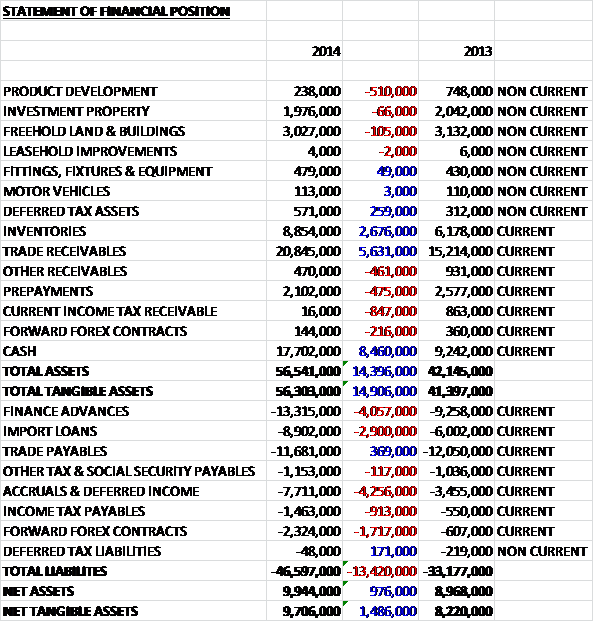

When compared to the end point of last year, total assets increased by £14.4M driven by an £8.4M increase in cash, a £5.6M growth in trade receivables and a £2.7M increase in inventories. Liabilities also increased during the year due to a £4.3M growth in accruals and deferred income, a £4.1M increase in finance advances which are advances against trade receivables, a £2.9M increase in import loans which are short term trade finance instruments, and a £1.7M growth in forward foreign exchange contract liabilities. The end result is a £1.5M growth in net tangible assets to £9.7M. The operating lease liabilities are negligible, indeed the receipts due to the group from its leasing activities outweigh any payments it is due to make. Of more note, perhaps, is the £2.1M worth of minimum royalties to be paid.

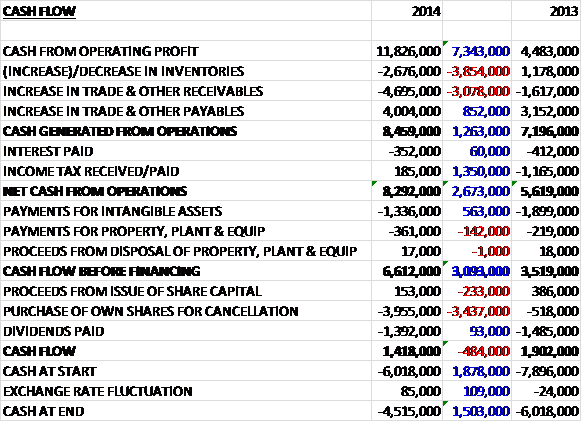

Before movements in working capital, cash profits increased by £7.3M to £11.8M. Due to an increase in receivables and inventories, this was eroded somewhat to become a £1.3M increase to £8.5M which after interest paid and a tax rebate gave rise to an operating cash inflow of £8.3M, a £2.7M growth year on year. This was more than enough to pay for capital expenditure and the group made a free cash flow of £6.6M, nearly £4M of which was spent on share buy-backs which represents an incredible 10% of the total share capital, and £1.4M was spent on dividends to give a cash flow for the year of £1.4M and a net debt of £4.5M at the year end – I think I would prefer to see this cash used to pay off debt rather than buy back shares but this is a good cash generation nonetheless.

Operating profit at the UK division was £2.2M, a positive swing of £2.6M when compared to the loss last year. Growth of UK sales across several categories has increased substantially with strong domestic sales coming from key ranges such as Peppa Pig, Teksta, Chill Factor, Minecraft, Dr Who, Fireman Sam, The Zelfs and Disney Princess Palace Pets. There was also strong growth from Peppa Pig in Australia and Europe along with Dr Who in the US. The operating profit at the Far East division was £8.8M, an increase of £3.8M when compared to 2013. The operating profit at the EU division was £103K, a decline of £56K year on year.

As their brands continue to mature, the group expects to see further growth from these as they continue to apply their development and marketing skills to them. In addition, revenues are expected to further increase due to the new products to be officially unveiled at the Toy Fair in London in a month’s time.

The group has secured a number of new licenses during the year with examples including The Clangers which should be ready for retail by June 2015, and the Teletubbies through an agreement with DHX Media. A new sixty episode series of Teletubbies is in production and the group expects to launch the range in the UK during 2016 with international launches following. As well as winning “Toy of the Year” for Teksta, the electronic puppy, the group has also won “supplier of the year” from Argos and Tesco, and the Teksta T-Rex also received the Creative Play Award in the electronics an multimedia section from Creative Steps.

The group seems to have a good number of its toys included in the official DreamToys listing which is an accurate prediction of the toys that will be in most demand at Christmas. There are two products in the top 12 and seven more in the full list of 72 toys. Leading the list for the group are Little Live Pets Bird Cage and the Minecraft figures. The other toys from the portfolio that are on the list are Minecraft Animal Mobs, Peppa Pig Weebles Wind and Wobble Playhouse, Peppa Pig Muddly Puddle Jumbo Jets, ChillFactor Ice Cream Maker, Teksta T-Rex, Cra-Z-loom Bracelet Maker and Cra-Z-Knitz Ultimate Designer Knitting Station.

The group are somewhat dependent on one customer with some 16% of revenues coming from this customer compared to 15% last year. There is also one brand that accounts for 18% of UK sales. They also seem very susceptible to changes in the US dollar/Sterling exchange rate with a 10% strengthening of Sterling against the Dollar giving rise to an incredible £8.3M reduction in profit and this year, the adverse currency movements gave rise to a £1.9M charge. The group does hedge some of this exposure, however. Finally, the group have outsourced production to China which also carries its own potential risks.

The debt structure seems a little complicated. The group has a bank overdraft of £1M, a trade finance facility of £13.5M and a £5M revolving loan facility which will expire within one year. The UK subsidiary also has an ongoing recourse invoice discounting facility of £20M.

All of the executive directors have been with the company for a long time with all of them except Michael Hyde being with the group since 1991, three of them being joint founders. The directors seem to have been very generously rewarded this year with a huge £555K bonus taking the highest paid director, JJ Diver to £812K for the year! After the year end, the group issued some 1.8M shares to employees exercising share options which is more than the 1.6M shares purchased for cancellation which cost the group £3.4M. The group has the authority to buy-back another £3.4M worth of shares and it remains part of the strategy to purchase its own shares when appropriate.

The new year has started off well with very pleasing sales at the consumer level which in the lead up to the Christmas season, is building ahead of expectations and the board remains confident that the company can deliver another year of solid progress resulting in enhanced profitability. At the current share price the shares trade on a rather expensive looking 18.1 but this improves considerably to 11.7 on next year’s consensus forecast. After a 10% increase, the shares are currently yielding 1.6% in dividends, increasing to 1.9% next year.

Overall this has been a good year for Character. Profits were up, net assets increased and both operational and free cash flow grew year on year too. The group seems to have some great brands with Tekstra, Peppa Pig and Minecraft looking good. Going forward, the Teletubbies license looks good and the Clangers might add some earnings too. Additionally as the other brands start to mature, earnings are likely to increase too. Not everything is positive, though. The group seems susceptible to Sterling weakness against the US Dollar, there is one customer that accounts for more than 10% of revenues and the board seem to be overpaid to me. In all though, a decent future P/E and the continued share buy backs look as though the shares may be decent value.