32 Red has now released its interim results for the year ending 2015.

Overall revenues increased when compared to the first half of last year with a £3M hike in UK revenue and a £400K growth in Italian revenue. Cost of sales increased by more, though, and the £2M point of consumption tax along with the £600K increase in the investment in the Italian business did not help, so that gross profit was some £754K lower. Admin costs increased by £264K and amortisation grew by £173K but legal costs associated with the UK remote gambling regulatory regime fell by £131K so that operating profit was £1.1M lower. After a small amount of interest income was more than offset by tax, the profit for the half year came in at just £76K, a decline of £1.1M year on year.

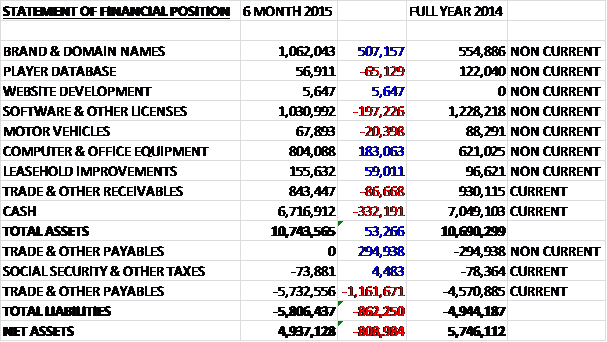

When compared to the end point of last year, total assets increased by just £53K as a £507K increase in the value of brands and a £183K growth in computer and office equipment was partially offset by a £332K fall in cash levels and a £197K decline in software and other licences. Liabilities also increased during the period driven by a £900K growth in payables. The end result is a net tangible asset level of £4.9M, a decline of £809K over the past six months.

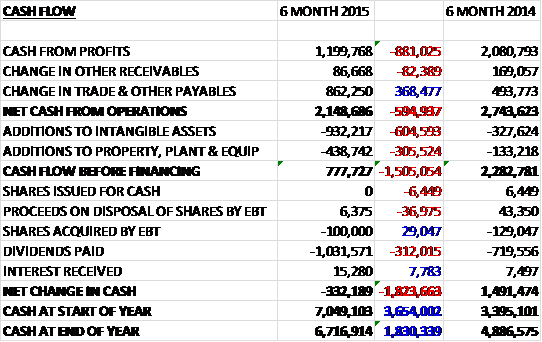

Before movements in working capital, cash profits fell by £881K to £1.2M. This was improved by a fall in payables so that net cash from operations was £2.1M, a decline of £595K year on year. The group then spent £932K on intangible assets and £439K on tangible assets to give a free cash flow of £778K which was not enough to cover the £1M spent on dividends so there was a cash outflow of £332K over the period to give a cash level of £6.7M at the period end.

During the period there was a 22% increase in active casino players to 62,214 which reflects the combination of accelerated new player recruitment, up 12%, and improved results from player retention and reactivation activities. Casino player yields did fall by 5% to £380, though, and casino cost per player acquisition grew by 9% to £197. The mobile casino did do well with revenues now representing 42% of total casino revenues.

The UK point of consumption tax was introduced in December and cost the group £2M during the first half of the year which probably explains why the group was not very profitable during the period.

The group suffered a £1M loss in Italy during the first half of the year compared to a £400K loss in the first half of last year as a result of the increased marketing activities in the country to capitalise on the strong growth opportunities in that market. In the country, NGR increased by 67% to £900K with a total of 4,285 new players recruited to give a total of 8,443 active players. The breadth and quality of games of the casino product in Italy is still behind that of the UK offering with further games to be introduced later in the year which should boost the appeal of the offer.

After the end of the half, the group acquired the remote online gaming business Roxy Palace for £8.4M comprising £2M in cash and the issue of 10M shares. Of the cash consideration, £1M is payable on completion, £500K in six months and another £500K at the end of December 2016. The business was founded in 2002 and built up a player database containing 230,000 registered players. It reported NGR of £10.1M and gross profit of £3.4M last year but this doesn’t include the effect of the point of consumption tax so profits going forward will be much lower. EBITDA was £1.6M last year so the acquisition does look fairly good value. The group will continue to operate the acquired brands in the UK going forward.

The second half of the year has started strongly with NGR for the first 12 weeks of the year up 52% excluding trading from the acquired Roxy business. Roxy also performed well and generated NGR of £2.5M since acquisition with the integration process progressing well. With the strong start to the period and the good progress integrating Roxy, the board is confident in delivering expectations for the full year. After a 10% increase in the interim dividend, the shares are currently yielding 3.4% increasing to 3.6% on Numis’ full year forecast.

Overall then, this was quite a difficult period for the group caused by the introduction of the point of consumption tax. Profits were down because of this and net assets also declined. In addition operating cash flow fell but the group was still free cash flow positive. In the UK, the number of casino players grew steadily with mobile doing well but the yield per player fell. In Italy, the number of players increased but the country is still not at a break-even level yet. The second half has started well and the acquisition looks decent so, with the view that full year targets are still going to be hit and with a decent dividend yield of 3.6% I will continue to hold.

To my untrained eye the uptrend still looks to be in place.

On the 30th November the group announced that the wife of non-executive director David Bowen acquired 20,200 shares at a cost of about £21K which is his first share purchase.

On the 21st January the group released their pre-close trading update for 2015. Overall, total NGR was up 51% to £48.6M and whilst part of this was due to the £5.2M contribution from Roxy Palace, core 32Red NGR was up 35% to £43.4M with Italian NGR increasing by 54% to £1.7M, casino NGR up 34% to £39.3M and other products growing by 42% to £2.4M.

The increased investment in market that is focused on the group’s strict returns criteria has accelerated organic revenue growth in the UK market. The focus has remained on the development of mobile device gaming and as a result mobile revenues were up 71%, representing 44% of the total.

The relocation of the acquired Roxy Palace business to Gibraltar and the integration of operations was completed in December, slightly ahead of schedule. NGR was in line with expectations during the integration phase and the business will now benefit from increased and more efficient marketing in the year ahead. The board have suggested they will continue to look for further acquisitions in the coming year.

The group have continued to make progress in Italy in what remains a competitive market and they hope to move towards break even in 2016.

Early trading in 2016 has been strong across the company’s products with revenues in the first few weeks up 27% on the same period of 2015 and up 54% including the contribution from Roxy Palace. The company expects to report EBITDA slightly ahead of expectations for 2015 and marketing expenditure will be increased again in 2016 with the board expecting further strong progress in the year ahead.

This is a difficult one. These results are clearly excellent but the focus on NGR and EBITDA does cause me some concern. What is the actual profitability here when we take into account tax and amortisation etc? I have now doubled my money on these shares over the past year so it seems to me now might be a time to book those profits. Probably too soon knowing me but let’s see.

On the 10th February the group announced a special dividend of 3p per share which gives an annual yield of 4.1% at the current share price so this is a nice surprise. Perhaps a potential acquisition fell through?