Mission Marketing has now released its interim results for the year ending 2015.

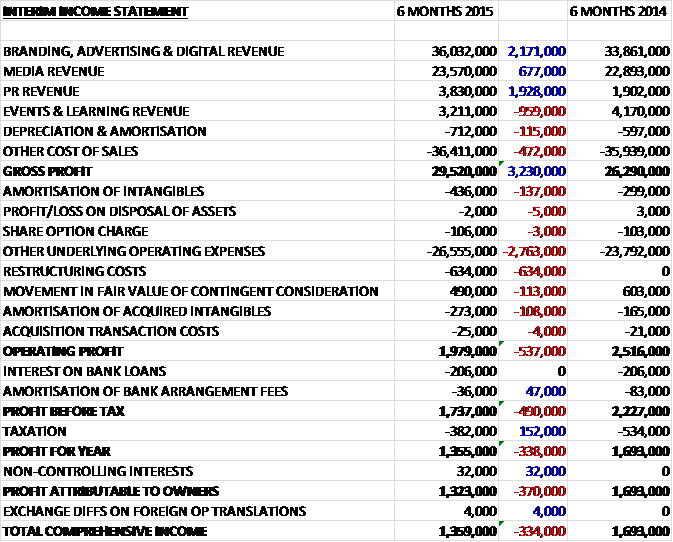

Overall revenues increased when compared to last year as a £959K decline in events and learning revenue was more than offset by a £2.2M growth in branding, advertising and digital revenue; a £1.9M increase in PR revenue and a £677K growth in media revenue. Cost of sales also increased modestly to give a gross profit some £3.2M higher. We then see a £2.8M increase in underlying admin costs but restructuring costs of £634K along with a £108K increase in the amortisation of acquired intangibles and a £113K reduction in the favourable movement in deferred consideration meant that operating profit fell by £537K. The amortisation of bank arrangement fees fell slightly and tax was down to give a profit attributable to the equity holders of £1.3M, a decline of £370K year on year.

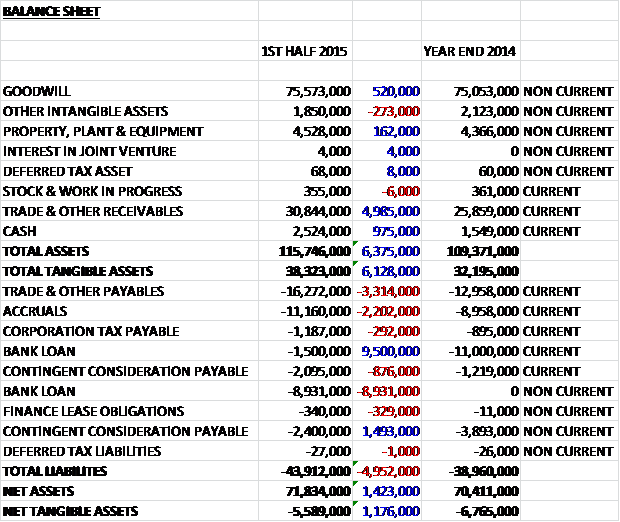

When compared to the end point of last year, total assets increased by £6.4M driven by a £5M growth in receivables, a £975K increase in cash and a £520K growth in goodwill. Liabilities also increased during the period as a £3.3M increase in payables, a £2.2M growth in accruals and a £329K increase in finance lease obligations was partially offset by a £600K fall in contingent consideration payable. The end result is a negative net tangible asset level of -£5.6M, a favourable movement of £1.2M over the period.

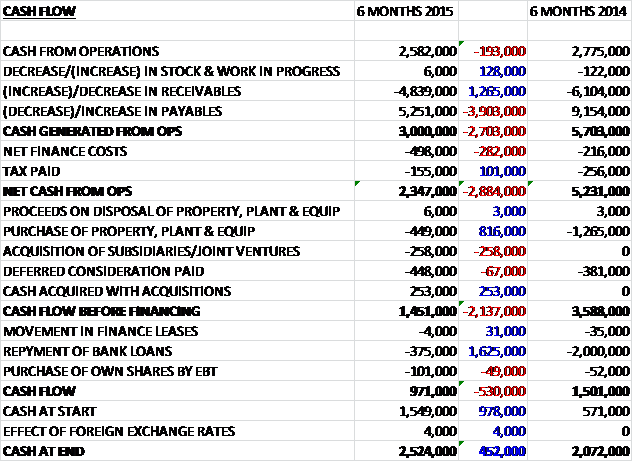

Before movements in working capital, cash profits fell by £193K to £2.6M. The increase in payables more than offset the fall in receivables but the payable growth was less than that of the first half of last year and after increased finance costs and slightly lower tax was paid, the net cash from operations came in at £2.3M, a decline of £2.9M year on year. The group then spent £449K on property, plant and equipment and £448K on deferred consideration so that free cash stood at £1.5M, of which £375K was spent to pay back loans and £101K was used to buy shares for the bonus scheme. The end result is a cash inflow of £971K to give a cash level of £2.5M at the end of the half.

The operating profit in the branding, advertising and digital division was £2.5M, just £7K less than last year. The operating profit in the media division was £442K, an increase of £100K year on year. The operating profit in the PR division was £460K, a growth of £360K when compared to the first half of 2014. The operating profit in the Events and Learning division was £35K, an increase of £10K year on year. The profit margin remained at 8% as improved margins in the PR, Media and Events and learning activities, partly driven by the restructuring undertaken at the start of the year, offset the higher initial running costs of the overseas businesses and the start-up of the new Sports Marketing agency. The spending cycles of the customers tend to result in a second half bias which is expected to be repeated this year.

The group have improved both their reach and their expertise, particularly within digital and data development areas whilst at the same time creating new initiatives such as Ethology which sees a harnessing of data with insights and direction that delivers responses from consumers. New business wins include Ask, Autoline, BMW, Brewin Dolphin, British Airways, Diageo, Muller Wiseman, RAC, Sage, SAS, and Siemens.

At the end of last year, Speed PR was launched which has apparently gone well and this year Splash has been bedded in in Asia. The April Six opening in San Francisco continued to thrive as does the recent merger to create the Bigdog agency with offices now in Leicester, Birmingham, Norwich and London. Alongside this activity they recently launched Mongoose Sports Marketing by hiring a new team. Some recent wins at this agency suggest that their approach is resonating with Corporates, Brands and Events.

Proof Comms, Splash Interactive, Speed Comms and Brandon Hill Comms were all acquired in the second half of 2014. In addition, the Weather Print and Digital Communications was acquired in February this year and the group commenced pre-launch activities in connection with its new sports marketing venture. These new entities contributed operating profit of £300K so organic growth seems to be rather negligible.

Following the announcement that Stephen Boyd will step down from the board as non-executive director, the group have announced the appointment of Julian Hanson-Smith from October. Julian set up the financial PR firm Financial Dynamics before pursuing a career in private equity. The Chairman has stated that the group are looking for further acquisitions and should make a couple of announcements later in the year. The board expects the full year expectations to be met.

Net debt at the end of the first half of the year stood at £7.9M compared to £9.5M at the end of last year. At the end of the year the group had £14.6M of committed facilities, of which £4M was undrawn with an additional overdraft facility of £3M. Due to the phasing of working capital requirements, an increase in net debt is expected in the second half of the year so there is not a great deal of firepower for further investment in these facilities really.

The interim dividend increased from 0.25p to 0.3p which gives a dividend yield of 2.6% which increases to 2.7% on FinnCap’s full year estimate.

Overall then, this was a bit of a mixed set of results. Profits fell year on year, due to restructuring costs but net tangible assets did increase, remaining negative. Operating cash flow was down, with comparisons not helped by a large increase in payables during the first half of last year. The group did generate a decent amount of free cash, however. The media and PR businesses with the drivers of growth with the other sectors remaining rather flat and the newer agencies contributed well which meant that organic growth does not seem that great. Net debt was down during the period but this is expected to reverse in the second half of the year but the board expect to meet full year expectations and a dividend yield of 2.7% is decent enough so I am content to wait to see what kind of growth can be achieved during the rest of the year.

The share price has moved around considerably but the trend since the start of the year is just about upwards.

On the 5th October the group announced that its April Six Agency opened its new office Singapore. It aims to be the first agency in the Asia-Pacific region to offer a specialist service for technology organisations with a global footprint. The group have appointed Brad Harris to run this office, someone who has 15 years’ experience leading technology marketing programmes in the region. He will be supported by the delivery team at Splash Interactive, the Singapore based digital marketing services agency acquired by the group last October.

On the 27th November the group announced the acquisition of Chapter Agency which includes the recently acquired Bell and Watson. The initial consideration is £1.3M payable in cash on completion and further consideration of up to £3.7M is payable subject to financial performance in 2015, 2016, 2017 and 2018, of which the first £200K will be payable in shares. Chapter was established in 2009 and is a Midlands-based advertising agency employing 29 people with a client base that includes Nissan, Yardley, Topps Tiles, Crodcube, Calor and Virgin Trains. Last year the business had profits of £400K. This seems like a decent addition, although that contingent consideration will have to be kept in check.

On the 18th December the group announced the appointment of Mike Rose to the board as an executive director. In 2009 Mike founded Chapter Agency Ltd where he has remained as MD since its recent acquisition by the group.

On the 22nd January the group released a trading update for the year. The group has experienced a strong second half and results for the year are expected to be in line with market expectations. The recent acquisitions are trading well but their addition to the group will result in an increase in the net debt position. They try and state that their balance sheet is strong but we know that from the last set of results that this is not true so I don’t know why they bring it up at all. This all seems OK, but nothing really to get excited about and I am out.