Ricardo have now released their interim results for 2013.

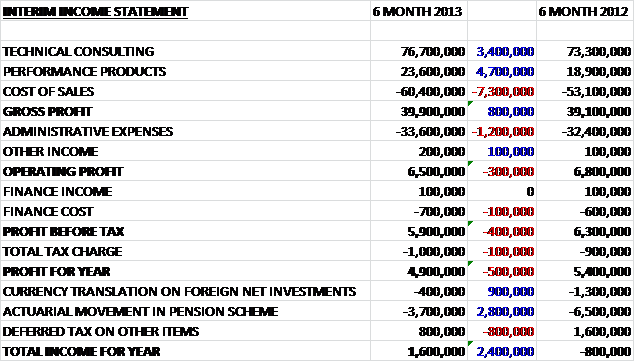

Revenues from both technical consulting (boosted by the acquired business) and performance products were on the up but with a similar increase in the cost of sales, Gross Profit was just £800K higher at £39.9M for the half year. Administrative expenses were £1.2M higher which meant that the operating profit was actually £300K less than last year. A slight increase in finance costs and tax drove the profit for the half year £500K lower to £4.9M. This suggests a bedding in period for the acquisition. The result is dragged down somewhat by actuarial movements in the pension scheme (albeit by less than the same period of last year) so the total income for the six months was £1.6M.

Income in the UK was up, boosted by the acquisition and strong passenger car and performance vehicle sector performance. Revenues in the US decreased slightly but revenues in Germany collapsed due to a key client taking their requirements in-house. Performance product revenues were driven by increased motorsport activity, delivery of defence vehicles and improved efficiency.

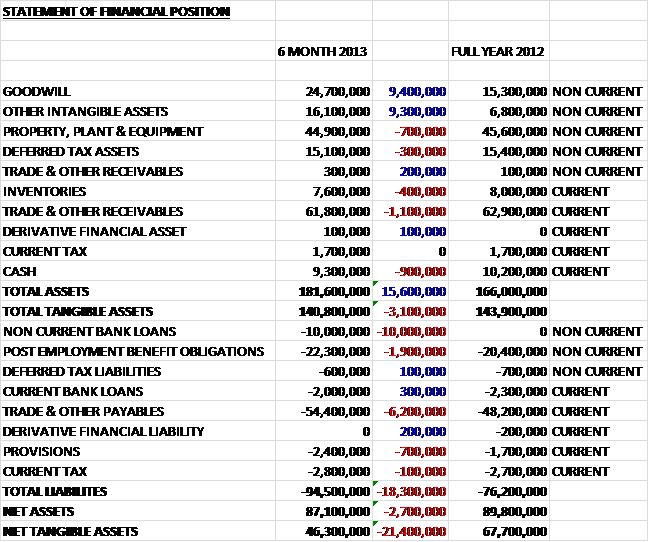

Starting with the assets, although they increased by £15.6M, that was driven completely by the increase in Goodwill (£9.4M) and other intangible assets (£9.3M) which is clearly related to the acquisition. Pretty much all the other main assets fell over the first 6 months of the year. The Goodwill asset was reviewed after the German segment lost a key client but it was determined that no impairment was required (£12.7M of that goodwill was in respect of the German Technical Consulting business, so quite a chunk).

Most of the liabilities increased, driven by a new bank loan of £10M and £6.2M more in trade and payables. Added to a small increase in provisions, total liabilities were up by £18.3M. This all lead to net assets decreasing by £2.7M to £87.1M and given the increases in assets were intangible, net tangible assets fell £21.4M to £46.3M. This is still a healthy level given the relatively small level of debt but it is a large undesirable movement. The pension scheme deficit is becoming a bit of a worry, however, and now stands at £22.3M (up from £20.4M at the end of the year). The increase is put down to reduction in the discount rate and higher expected inflation.

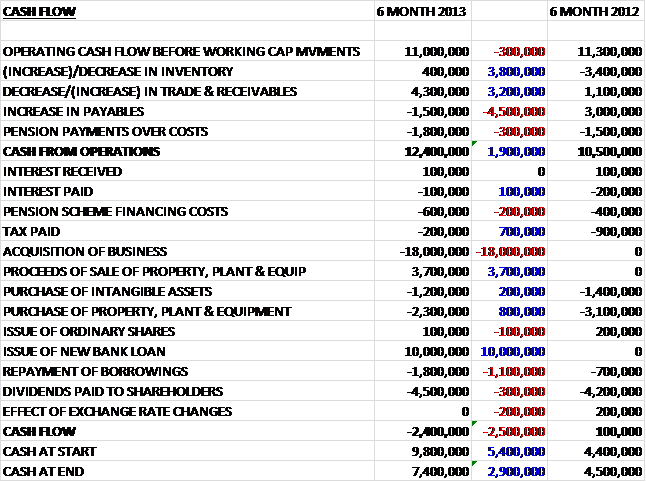

Before changes in working capital, the cash flow of £11M for the half year was at a similar level to that of the same period of last year. A tighter control on receivables helped the cash from operations up £1.9M on last year to £12.4M. There was a small amount paid out on the pension scheme and a negligible tax payment (very low, even considering the tax breaks they get from R&D) but the main point here is the £18M paid out to acquire AEA. There was an extra £3.7M received from the sale and leaseback of the German properties and slightly lower capital expenditure than last time plus a net £8.2M of new borrowing to give a fairly decent cash flow before increased dividends of £4.5M were paid out.

This all leaves the bottom line of a £2.4M outflow of cash. When it is considered that during this time, £18M was paid out for the acquisition but only £8.2M in new borrowings and £3.7M in one off receipts (£11.9M all together) had it not been for the acquisition, there would have been a strong positive cash flow here.

The profitability of Technical consulting was down slightly, while performance products have increased profits. Geographically, UK, most of Europe, Japan and Malaysia improved but in Germany, China and Other Asia sales have fallen. There was a major contract loss in Germany but it is a shame to see the fast growing Asian economies not doing so well for Ricardo. US performance should improve due to the structure of the order book. The order book looks fairly robust, albeit having been boosted by the acquisition, at £136M compared to £107M at the end of last year.

The group is in a position of net debt, which is quite unusual in recent years and suffered a swing of £10.6M, driven by the acquisition. At £2.7M, however, it is still very low and the borrowing facilities of £35M still look very safe. That purchase of AEA included £9.3M of Goodwill and £8.5M of other intangibles so there were no real assets to speak of.

Long term, continued focus on emissions regulation and fuel efficiency is good news for Ricardo, given their expertise in those areas. The continuing threats of asymmetric warfare are also giving opportunities for the group. Likewise, renewable energy is another area that Ricardo are active in, which is demonstrated by their work with David Brown Gear Systems and Samsung in designing a new gearbox for a new range of offshore wind turbines.

Ricardo have experienced good levels of activity in the automotive markets of China, Korea, Japan, UK and US with growth rates particularly strong in emerging economics where Ricardo is providing solutions to improve fuel economy and reduce emissions and they have secured a number of significant programmes across their main geographical markets. The group is achieving good levels of business in the Motorcycle industry with their big European client and new clients in Japan and China. The motorsport business has continued the supply of engines and transmission systems to McLaren and continues to provide transmission systems for the Japanese Super GT cars, along with transmission systems for an F1 team.

Agricultural and industrial vehicles have been doing well in Japan with relationships emerging with new companies in China, and starter orders hopefully the sign of more business there. The group has won some work in the industrial vehicles sector to develop a wide body version of TaxiBot with Israeli Aerospace Industries that allows planes to taxi under pilot control without the use of jet engines, thereby saving considerable fuel usage. In the Rail sector, a number of new customers have been attracted and there has been interest in developing Natural Gas as a locomotive fuel, a project on which Ricardo has helped a Railroad company in North America.

Further orders have also been received in the power generation sector, particularly in renewables with projects in both offshore and onshore wind turbines, tidal stream and solar power. They have also been active in developing energy storage solutions. In marine, ship makers are not looking to make huge investments so focus has remained on improving the efficiencies of current engines, including the integration of Gas powered vessels. The Government sector has been challenging, given the cutbacks that have been taking place and the UK public sector remains the largest market.

In performance products, demand for transmissions remains strong across many racing series and over 2,400 engines have now been delivered to McLaren. Rail transmission production has now started and a follow on order for these is expected that will take production through the next two years. Similarly, a new follow on order from Bugatti will take production of that transmission through to 2014 and a follow on order from the MoD for more Foxhound vehicles should keep the facility busy.

So, for the last six months we have seen revenues up, being particularly strong in the UK but counteracted by the loss of a client in Germany. Costs have increased to a greater degree, however, and profits were £500K lower at £4.9M. Net tangible assets fell £21M to £46.3M because the acquired company had no tangible assets to speak of and there was a negative cash flow of £2.4M. However, when it is noted that the £18M acquisition was only partially funded by new borrowing and one off receipts following the sale of the German offices, the cash flow looks fairly good. The share is currently yielding a 3.2% return, which is not too bad.

Overall then, this half year has been characterised by the acquisition and I think it is too soon to see how that will affect results for the full year. Profits are down slightly and the loss of the German client is a concern but the cash flow was fairly decent considering and going forward Ricardo should be able to benefit from increasing emissions regulation around the world. I will continue to hold.

On 16th May, Ricardo released an interim management statement. Overall it seemed to be very positive as customer activity has improved leading to a good pipeline across the group and the order book at the end of April stood at £130M. Revenue for the 8 months was up by 15% (3% discounting the influence of the acquisition). Also very pleasing to hear is that the German and US business are recovering after a difficult period.

Technical consulting levels have increased, driven by a broad range of projects from car manufacturers with work from the US, UK, Russia and the Far East. Demand in continental Europe remained subdued but Japan performed well. Outside the car market, new projects were started for power generation and rail applications, an example being the group advising Canadian National Railways on the potential use of Natural gas as a fuel for their locomotives.

Ricardo-AEA seems to be bedding in well and is in line with expectations. New orders have included a three year contract to monitor air quality in Riyadh and a contract to provide advice to Scottish organisations on how to reduce energy, water and material costs. The performance products segment continued to perform well with a new order for 76 more Foxhound vehicles and the continued supply of engines and components to motorsport companies and a new programme for the supply of transmissions for the Porsche cup.

Cash generation was strong, with a net cash position at the end of April of £11.3M. Overall, the business seems to be progressing well and there has been a pick up of activity outside of Europe and I believe this to be quite a positive update. The share price has picked up recently though and it is not all that cheap. I still consider Ricardo to be a good investment in the medium term though and may look at adding some more.

On 16th July, Ricardo released a trading update. It was mentioned that new contracts have been won in the car, defence, power generation and marine engine sectors and customer activity has been positive. Revenue levels the the whole year should be above that of last year, even when discounting the acquisition of Ricardo-AEA and profit performance should be above market expectations. There has been good cash generation which led to a net cash balance similar to the prior year. Remarkable when the year included the £18M purchase of AEA. All in all this a very upbeat statement and I think these shares are worthy of a buy.