Sainsbury has now released their interim results for the year ending 2016.

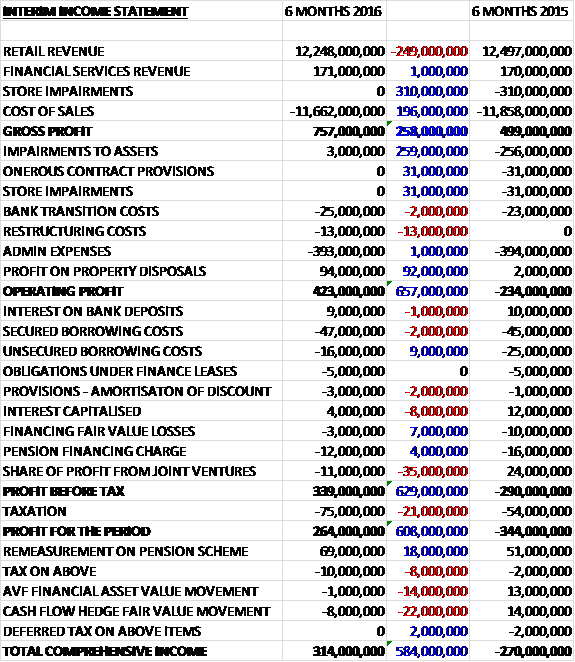

Revenues declined when compared to the first half of last year with a £249M fall in retail sales and a fairly flat financial services revenue. Cost of sales also fell and the lack of a £310M store impairment that occurred last year meant that gross profit increased by £258M. Underlying admin expenses were broadly flat but there was a host of non-underlying items that occurred last time that did not happen this time such as further impairments and onerous contract provisions. We also see a £92M increase in profit on property disposals that meant that operating profit saw a positive swing of £657M. Finance costs fell slightly (they are expected to increase in the second half due to lower capitalised interest and the perpetual securities coupons) but there was an £11M loss from joint ventures as opposed to a £24M gain last time and after tax increased by £21M the profit for the half year came in at £264M, a positive swing of £608M year on year.

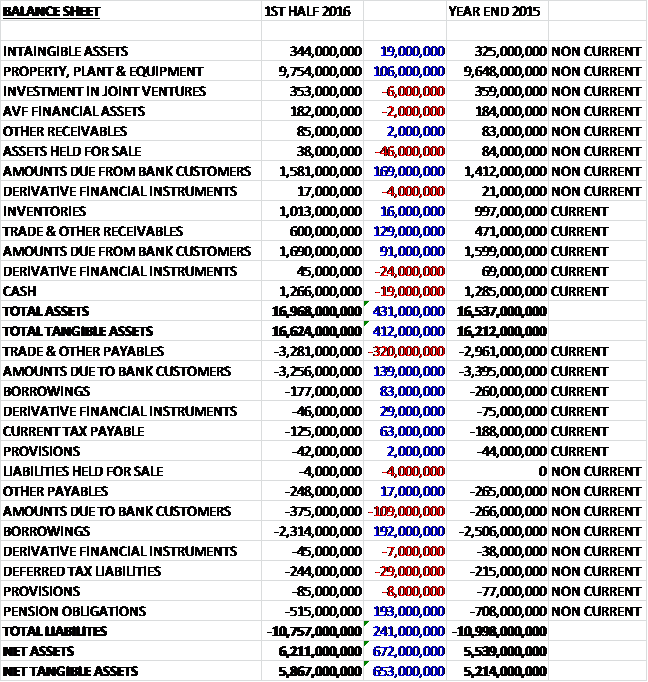

When compared to the end point of last year, total assets increased by £431M driven by a £260M growth in the amounts due from bank customers, a £129M increase in receivables, and a £106M growth in property, plant and equipment. Total liabilities declined by £241M as a £193M fall in pension obligations, a £275M decrease in borrowings and a £63M fall in current tax payable was partially offset by a £320M growth in trade and other payables. The end result is a net tangible asset level of £5.867BN, an increase of £653M over the past six months.

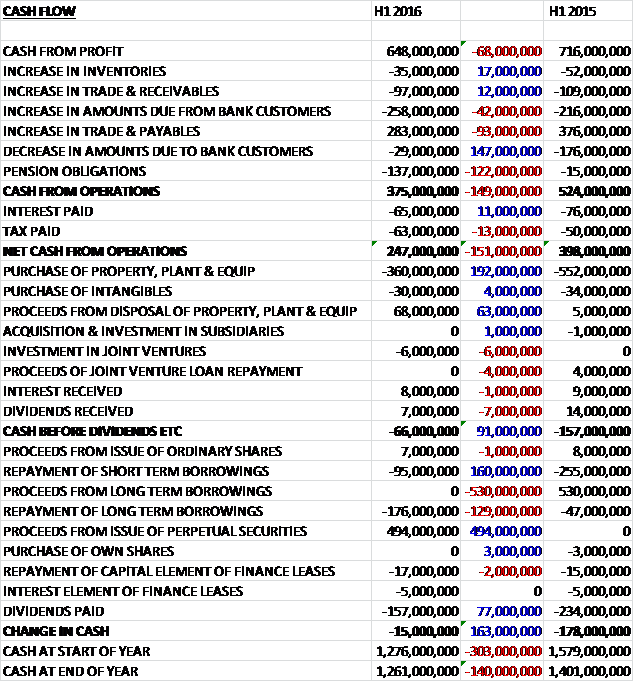

Before movements in working capital, cash profits fell by £68M to £648M. There was a general inflow from working capital but the group spent £122M more on the pension scheme (another £125M will be spent on pensions in the second half of the year) so that the net cash from operations was £247M, a decline of £151M year on year. This did not even cover the £360M spent on fixed tangible assets and there was a further £30M spent on intangibles so the cash outflow before financing was £66M. The group then received a £494M cash injection from the issue of perpetual securities which was used to pay off debt (a dubious trick to get debt off the balance sheet in my view) which left the cash outflow for the six months of £15M to give a £1.261BN cash level at the period-end.

Excellent harvests and high yields, particularly in Europe, have led to a drop in commodity prices. Fresh foods such as meat, fish, poultry and produce have seen the highest reductions year on year as food retailers pass the lower prices on to customers. The discounters have grown their market share to over 9%, charging lower prices on a limited selection of products and their growth continues to be a challenge to the established players. Customers are buying more items, driving an increase in volume growth but this is being offset by price deflation, ensuring overall grocery expenditure remains relatively neutral.

The underlying operating profit in the retail business was £332M, a decline of £56M year on year. Sales in the supermarkets were down just over 2%, reflecting the impact of food deflation and changing customer shopping habits. The group are trialling new formats in six of their supermarkets in response to changing customer shopping missions with changes including a different store layout and more checkout options to make it quicker and easier to shop in store and to offer customers more choice. They are making use of the supermarket space by putting the clothing and general merchandise ranges into more stores and offering products and services through concession partners such as Timpsons, Jessops, Argos and Explore Learning.

The group opened 37 convenience stores in the half and sales grew by nearly 11%, despite these stores selling a higher proportion of categories that are experiencing food deflation. They will continue to open one or two stores per week and will look at both smaller and larger sites than their standard convenience stores. The new trial format micro store in Holborn, central London, is just under 1,000 square foot and is designed to meet the needs of people working in the area who buy “food for now”.

The online business continued to grow, in both food and other categories like clothing. Groceries online grew by 7% and orders grew by nearly 14%. This included a record week for online, where they delivered 256,000 orders. At the end of the half they had 52 grocery click and collect sites and are on track to have a hundred by the end of 2015. As click and collect grows more popular, it makes commercial and operational sense to pick orders as close as possible to the collection point, minimising transport and handling costs.

The group have extended and improved their own brand bread range, introducing a selection of premium own brand loaves that are freshly baked in store, and adding new lines made from grains such as spelt, rye and quinoa. This investment has grown volumes by 10% since March and increased their bakery volume market share by 1.5% to 19.2%. The group have also removed nearly 35 tonnes of sugar from their juice ranges and have developed bespoke juice blends with improved flavours. During the period, they launched nearly 70 improved lines across the fish category and have introduced new party food lines such as mini dressed crabs in time for Christmas. The one brand ranges account for 49% of food sales. The premium range delivered over 2% volume growth and the core “By Sainsbury’s” range achieved volume growth of over 3% in response to the lower pricing strategy.

The group have reduced prices by £150M and have simplified their offers and reduced promotional activity in favour of regular lower prices. As well as being more popular with customers, this approach also helps improve forecasting, drives better availability and reduces waste.

The non-food business is an area that is ripe for expansion with only 126 stores offering the full range. The group continues to increase their market share in clothing and sales have grown by nearly 10% during the period as the partnership with Gok Wan and the collaboration with Admiral men’s sportswear proved popular. A successful back to school campaign solidified Sainsbury as the fourth biggest schoolwear retailer by volume. After a successful regional trial, Tu online was rolled out nationwide in the summer and initial sales exceeded estimates. General merchandise sales grew by 1.4% with the bedroom range up 23% due to the strength of the designer bedding offer and dinnerware, mugs and glassware also performing well.

The estimated market value of properties, including the 50% share of properties held in joint ventures, was £10.8BN, a decline of £300M due to a reduction in market rental values and a yield movement. Earlier in the year they opened a 72,000 square foot replacement supermarket in Fulham, increasing the size of the store by 50% and creating space to build 463 new homes. They expect to open a replacement supermarket at Nine Elms in London in summer 2016 and this development will include 737 new homes, local shops, restaurants and office space. These mixed-use developments will generate property profits of around £200M split over this year and next.

The underlying operating profit in the financial services business was £34M, although there was a £25M non-underlying cost relating to the bank migration. This compared to £35M underlying and £23M for the bank migration in the first half of last year. In all, the transition costs are now expected to be at the top end of the £340M to £380M range driven by a six to nine month delay in programme delivery. Loan volumes increased by 18% year on year, with a 23% increase in car loans and a 14% increase in home improvement loans. Despite an increasingly competitive market, the insurance portfolio produces sales growth of 11%. They opened their 200th Travel Money bureau and had their best month for travel money sales in July. Optimising the travel money website for mobile resulted in a 300% increase in sales conversion across these devices which aided the 49% growth in customer transactions.

The group continue to offer reward credit cards with no annual fee at a time when other providers have cut their reward schemes. They installed 49 ATMs in the half, taking the total estate to 1,622 with transactions increasing by 3.9%. The build of the bank platform is materially complete and testing continues. The plan now is to migrate savings customers in Spring/Summer 2016 and cards and loans customs in Spring/Summer 2017, which is between six and nine months later than planned, hence the previously mentioned increase in costs. The bank is expected to deliver a mid-single digit year on year growth in underlying profit in 2016 and capital injections are expected to be about £160M.

The Netto joint venture is on track to open 15 stores by the end of the year. At the end of the half they had six stores open and are learning about the growing discount market. The in store bakery products and British meat offer are particularly popular but the business is still loss making, with Sainsbury’s share of the loss £5M during the period due to start-up costs. The group’s underlying share of profit from its joint venture with British Land was £8M compared to £6M last time and the underlying share of profit from the joint venture with Land Securities was £1M, down from £2M last time. Overall it is expected that the share of profit from the property joint ventures will be slightly lower in 2016 as a whole with the share of losses from the start-up joint ventures being similar to last year.

The group announced a 4% pay increase for 137,000 staff members who work in the stores to a new hourly rate of £7.36 – no doubt pre-empting and reducing the effect of the new minimum wage legislation.

In July it was announced that Lloyds Pharmacy would acquire the Sainsbury pharmacy business for around £125M realising profit on disposal of about £100M. In addition, the group will receive commercial annual rate payments from Lloyds for each of the 277 in-store pharmacies and the transaction is expected to complete by the end of February 2016. It was also announced that the mobile phone joint venture with Vodafone will close towards the beginning of 2016. Customers will still be able to buy phones from the 38 phone shops, however.

At the period end the group had capital commitments of £195M and during the half year the group opened a new one million square foot general merchandise depot at Daventry International Rail Freight Terminal and also upgraded the Basingstoke distribution centre.

The cost savings programme is ahead of plan and the board expect savings of around £225M by the end of the year and are on track to deliver £500M in cost savings over the next three years. So far this year £115M of operational cost savings were achieved with an increase due to growth in the savings delivered from the core operational efficiency programme and one-off benefits relating to a review of their commercial expenditure and the organisational structure within stores and store support centres. The savings in the first half more than offset the inflationary pressures on costs, however, they expect this inflationary impact to step up by £13M in the second half as a result of the 4% wage increase.

During the period the group issued £250M of perpetual subordinated capital securities and £250M of perpetual subordinated convertible bonds which may be converted into shares of the company at the option of the holders at any time up to 23rd July 2021 at a conversion price of 348.6p. I do think that this is a bit of a sneaky way to keep a certain amount of debt off the balance sheet. The group used the proceeds of this to pay back some bank debt and also to make a payment to the pension scheme to reduce the obligations from £651M at the end of last year to £473M at the end of the period.

The bank has entered into a £400M asset backed commercial paper securitisation of consumer loans. Of this facility, £300M had been drawn as at the period-end. Interest on the notes is repayable at a floating rate linked to three-month LIBOR and their contractual repayment is determined by cash flows on the relevant personal loans included in the collateral pool. Core capital expenditure, excluding the bank, is expected to be around £550M for the whole year.

After a 20% fall in the interim dividend, the shares yield 5% which falls to 4.5% on the full year forecast. If we include the perpetual securities which I certainly think we should, the net debt stands at £2.377BN compared to £2.382BN at the point of last year but the board expect the net debt at the end of the year to reduce year on year. This does not include the bank’s own net debt balance.

Overall then, times continue to be tough for Sainsbury’s. Profits did increase but this was due to the various non-underlying costs that occurred last year and underlying profits declined year on year. Similarly, net assets improved but this was mainly as a result of the perpetual securities taken out moving debt off the balance sheet. Operating cash flow declined, which shows what is really going on and there was no free cash flow after capex.

Profits in the retail side fell, driven by a decline in sales at the supermarkets due to food price deflation and changing shopper habits. This decline in the core supermarkets was partially offset by increased sales in convenience stores, online and clothing. The financial services business delivered broadly flat results which were hampered by the bank transition costs being greater than expected, and the Netto stores are still loss making.

Costs going forward are going to grow due to the pay rise given to staff but this seems a canny move to make sure that the new living wage legislation effects are tapered over a few years. Another canny move seems to be the sale of the pharmacy business which will realise a decent profit and still allow the group to recoup some rental income from Lloyds.

Overall though, the core business is still in decline and the forward yield of 4.5% seems rather susceptible to more costs given that it is not covered by cash flow so I will continue to watch from the side lines here.

On the 22nd December the group released a statement that Lord Sainsbury had sold shares to take his holding below the 3% threshold. Apparently though this was only crossed as a result of a gift of shares to his charity.

On the 5th January, the group released a surprise announcement that it had made an approach of an offer for Home Retail group for shares and cash, which was rejected. The two companies have been working closely trialling a number of Argos concessions in Sainsbury stores. They now have until the 2nd February to announce a firm offer. This is a strange one, I can’t see how it makes strategic sense but I will watch the proceedings with interest.

On the 13th January the group released their Q3 trading statement. Excluding fuel, like for like retail sales were down 0.4% compared to 1.6% in the first half of the year, with total sales up 0.8% which has seen their market share increase during the quarter. They launched their new Taste the Difference wines in time for Christmas which contributed to sales growth of over 18% across the range and the programme to invest in the quality of over 3,000 products remains on track. Like for like volumes and transactions both increased year on year.

The group reduced their levels of vouchering and promotional items along with the number of multi-buys in favour of lower regular prices, continuing their commitment to simplify prices and promotions. During the period 16 convenience stores were opened and online groceries saw sales up nearly 10% with some 101 Click and Collect sites now available nationwide. General merchandise saw sales growth of 5% in the quarter and clothing was up nearly 6% despite the unseasonably warm weather. The bank saw an 11% volume growth in loans and a 29% increase in travel money transactions.

The board now expect like for like sales in the second half to be better than the first but food price deflation and pressures on pricing will ensure that the market remains challenging for the foreseeable future. Things certainly seem to be improving here but it has to be said Christmas trading is usually fairly good for the group. Growth remains negative on a like for like basis and I would like to wait and see what happens in normal trading and the proposed Home acquisition.

On the 2nd February the group announced that they had reached agreement on the key financial terms of a possible offer for Home Group. Under the terms of the offer, Home Group shareholders will receive 0.321 new Sainsbury shares and 55p in cash per Home Group share they hold. In addition they will receive about 25p from the Homebase return of capital and 2.8p in lieu of a final dividend for 2016. The Homebase capital return reflects the £200M return in respect of the sale of Homebase announced previously by the Home group.

The possible offer implies a value of about £1.1BN for the company based on the closing Sainsbury share price at this date or £1.3BN including the Homebase return of capital. Under the terms of the offer, Home Retail shareholders will own about 12% of the combined group. The board of Home Retail has indicated that it is willing to recommend the key financial terms of the offer to their shareholders.

Sainsbury expects the offer will be accretive to its EPS in the first full year of ownership and by the third year they expect double digit earnings accretion and a low to mid-teens return on invested capital with some £120M of EBITDA synergies expected to be generated by that point.

About a half of the identified synergies are expected to be generated from Argos Concessions arising from cost savings generated from the relocation of certain existing stores into concessions in Sainsbury stores, including but not limited to cross-selling opportunities and the expansion of click and collect desks. About a third of the synergies are expected to be cost synergies generated by removing duplication and overlap from both central and support functions at the two companies together with procurement benefits resulting from the increased scale. The remainder of synergies are expected to be further revenue synergies, principally from the sale of Sainsbury’s clothing, homewares and seasonal ranges through the existing Argos network.

It is expected that the realisation of the identified synergies will require one-off exceptional costs of about £140M split equally across the first three years following completion. It is also expected that incremental capex of about £140M will be incurred in the three years following completion, relating to store fit-out expenditure. About 20% of this capex will be incurred in the first year with the remainder split equally in the second and third years following completion.

The group intends to finance the cash consideration for the offer through its existing debt facilities and resources to be entirely refinanced at a later date through the proposed transfer of the financial services business to Sainsbury’s bank.

The group must either announce a firm intention to make an offer for Home or announce that it does not intend to make an offer by the close of play on the 23rd February.

Overall then, this is certainly interesting. There are huge synergies on offer here and the Sainsbury management do a good job of selling this. I am remaining on the sidelines but will watch with interest.

On the 15th March the group released its Q4 trading update. The supermarkets recorded both like for like transaction and volume growth and the group maintained their market share in the quarter. They also announced that they will be phasing out most of the multi-buy promotions by August and will continue to simplify their trading strategy in favour of lower regular prices. During the period they opened 16 convenience stores and online grocery sales grew at nearly 14%.

Clothing delivered over 10% growth and the newest Gok Wan collection had its best ever February launch. Entertainment also performed well, with nearly 11% growth driven by some big releases during the quarter. The bank saw a 15% volume growth in insurance new business and a 12% growth in travel money transaction volumes.

Overall then, this was actually a pretty decent update. The like for like sales decline seems to have been halted for now, although my other underlying concerns I covered at the time of the last update are still present and I am only going to update on Sainsbury again when those debt concerns have been addressed.