QinetiQ has now released its interim results for the year ending 2016.

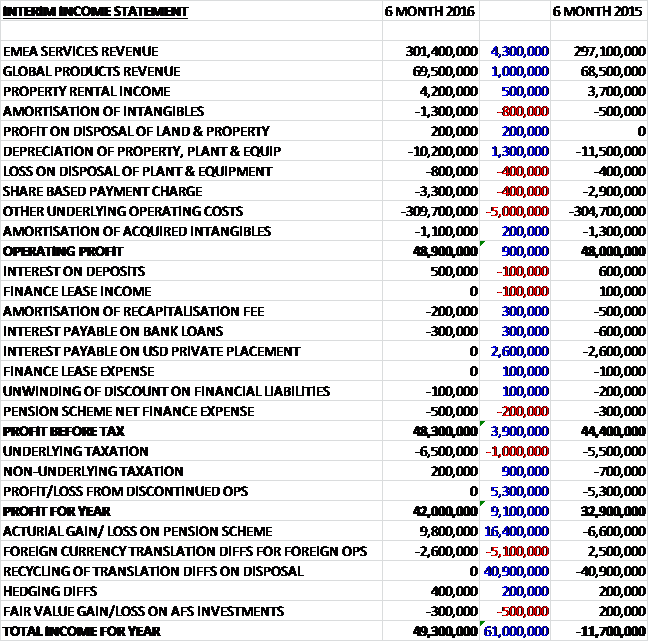

Revenues increased when compared to the first half of last year with a £4.3M increase in EMEA Services revenue, a £1M growth in global products revenue and a £500K increase in property rental income. A growth in amortisation was offset by a fall in depreciation but share based payments increased and other underlying operating costs grew by £5M so that the operating profit was £900K above that of the first half of 2015. Finance costs fell, mainly as a result of the £2.6M fall in the interest payable on the US private placement as the group paid the debt off following the sale of the US services business last year and the pre-tax profit grew by £3.9M. We then see a broadly flat tax charge but there was no loss from the discontinued operation that took place last time and the profit for the half year period came in at £42M, a growth of £9.1M year on year.

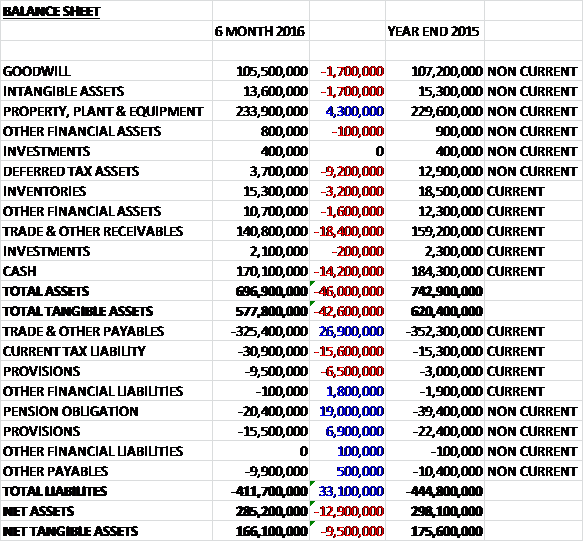

When compared to the end point of last year, total assets fell by £46M driven by an £18.4M decline in receivables despite the receivable acknowledged from the insurance company (see below), a £9.2M fall in deferred tax assets, a £14.2M decrease in tax and a £3.2M fall in the value of inventories, partially offset by a £4.3M growth in property, plant and equipment. Total liabilities also declined during the period as a £26.9M fall in payables, and a £19M decrease in the pension obligation was partially offset by a £15.6M growth in the current tax liability. The end result is a net tangible asset level of £166.1M, a decline of £9.5M over the past six months.

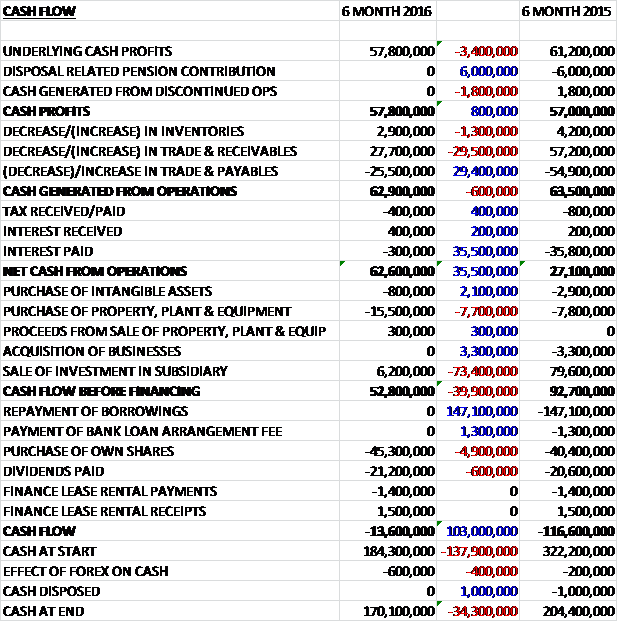

Underlying cash profits fell by £3.4M to £57.8M but last year’s one-off contribution to the pension scheme related to the disposal meant that actual cash profits increased by £800K. There was a small cash inflow from working capital during the period as both inventories and receivables fell but this effect was less than last time so the cash generated from operations fell by £600K. A massive interest payment last time as the group paid off its debt early, however, meant that net cash from operations came in at £62.6M, an increase of £35.5M year on year. The group spent £15.5M on property, plant & equipment and £800K on intangible assets to give a hefty free cash flow of £46.6M. The group also benefited from a £6.2M cash inflow from the sale of a subsidiary and all of this cash was spent with £21.2M going on dividends and £45.3M used to buy the company’s own shares which gave a cash outflow for the year of £13.6M and an impressive cash level of £170.1M at the period-end.

The group has been operating in a tough and uncertain market. Orders fell to £228.4M against a strong prior period when they were £320.5M. The market environment was challenging with budgets under pressure and some de-scoping and delay to orders. Additionally, about two thirds of the orders reduction from the prior period was due to the timing of multi-year contract awards and the impact of this on near-term revenue is expected to be limited. Some significant multi-year orders were awarded after the period-end including a £153M five year renewal for engineering support to the UK MOD for the A400M Atlas, Typhoon and Tornado aircraft under a new output-based model. In all, at the start of October the group had 90% of 2016 revenue under contract, consistent with the prior period end.

The trading environment in the UK is tough in the short term. The Government’s Strategic Defence and Security review will be published shortly, and its publication will help bring clarity on its priorities and the associated allocation of the UK defence budgets with efficiency and innovation likely to be the key themes. Also underway is a public consultation by the recently established Single Source Regulations Office on the proposed approach to calculating the baseline profit rate for single source contracts which is expected to conclude in early 2016. The regulations apply to new single source contracts, plus existing contracts when they come up for renewal with about 70% of the group’s total EMEA services revenue being derived from these types of contracts.

In the US, the defence downturn is reaching the bottom but the defence spending cycle is long. New Programs of Record for capabilities such as ground robots are still at least a year away and in the near term most opportunities are likely to be for the reset and recapitalisation of products previously used on operations. The Department of Defence is increasingly concerned that its technological superiority has been steadily eroding so it has launched the defence initiative, an effort to identify and invest in innovative ways to sustain and advance America’s military dominance for the 21st Century. This will put new resources behind innovation and R&D in technical areas where QinetiQ happens to have particular strengths. In Australia, the government needs to modernise its defence equipment and plans to replace the majority of its platforms over the next fifteen years, supported by an increase in defence expenditure to 2% of GDP.

The operating profit at the EMEA Services business was £42.7M, broadly flat year on year. In the Air business the group is working with the MOD and the supply chain to develop a new model to transform the provision of aircraft test and evaluation. Shortly after the period end, it was awarded two contract renewals under this new model, worth a combined £153M over five years, to deliver technical services to fast jets and heavy life aircraft. This new way of working improves long-term planning providing better visibility, and delivers considerable savings to the MOD. This award complements a £13M contract won in the period to assist the MOD in bringing the Delta Test variant of the A400M Atlas into UK service, and a £5M contract to evaluate flight control system upgrades to Boeing’s Chinook helicopter.

In international markets, the business was awarded a five year extension to the contract under which it manages and assists in the delivery of training at the Swedish Flight Physiological Centre. The Air business also delivers turnkey services for customers using Remotely Piloted Air Systems to meet growing demand particularly from international organisations such as the UN. Following last year’s opening of the Snowdonia Aerospace Centre at Llanbedr in Wales, the business is to demonstrate the use of Remotely Piloted Aircraft in tackling environmental issues in a project for the Welsh Government.

The weapons business was awarded a new contract with the MOD for a new research framework contract for trials, testing and analysis in cyber and electronic warfare. It also won a £5M contract from Raytheon to develop and qualify a new generation of the Paveway precision-guided bomb for the Typhoon aircraft due to enter service with the RAF in 2019. The targets offering was augmented in the period by the introduction of the new Firejet target which will underpin future expansion in international markets. During October, the weapons business led a team from across the group to deliver an international at sea demonstration at the Hebrides range, the largest in Europe. The exercise attracted nine ships from eight nations, culminating in the first ever launch of a ballistic rocket into space from the UK and its subsequent engagement by an SM3 missile launched by a US guided missile destroyer.

During the period the maritime business was awarded a new contract to deliver acceptance trials for the four new MARS class tankers. The business is targeting international markets, principally through the supply of mission systems for offshore patrol vessels, corvettes and frigates. It is also pursuing selected growth campaigns with a focus on emerging technologies such as autonomous systems. During the period it was selected to develop and deliver a containerised command system to control multiple unmanned systems for demonstration by the Royal Navy in 2016.

In the Cyber, Information and Training markets, although competition is fierce, budgets for C4ISR and cyber security are expected to grow as recent funding rounds have either protected or enhanced spending. The CIT business is the MOD’s leading supplier of C4ISR research, growing its research revenues in the period and winning new work to improve information systems for deployed headquarters. During the period the business was awarded a position with Northrop Grumman on a seven year framework contract to deliver cyber security support to the UK Government. CIT is also going to market in partnership with established prime contractors outside the UK, most notably in the US training and simulation market. Finally the business is providing secure receiver processing for the encrypted Public Regulated Service on the Galileo constellation of satellites, the EU version of GPS which goes live in 2017. During the period it launched a new receiver that will utilise the PRS service for use by governments, the military and emergency services across Europe.

In the Global Products division, orders fell from £71M to £57.6M due to reduced demand for military products driven by lower levels of operational spending the US and the timing of recapitalisation orders for the robot fleet, partially offset by a small increase in orders for OptaSense, the Distributed Acoustic Sensing business. The operating profit at the Global Products business was £7.1M, an increase of £400K when compared to the first half of last year, benefiting from a reduction in overhead costs in the US products business.

The US products business, which accounts for about 75% of revenues in the division, saw revenues generated by the sale of unmanned systems increase, principally for the maintenance, repair and overhaul, or reset of robots previously used on operations. Demand for survivability products continued to be impacted by reduced operational budgets, but the business shipped armour for the C-130 aircraft as well as ground vehicles during the period. Shortly after the period-end, the business was awarded an initial $16M contract by General Atomics to deliver control hardware and software for the Electromagnetic Aircraft Launch Control System and Advanced Arresting Gear for the US Navy’s next generation aircraft carrier.

At the end of September, the OptaSense business completed an 18 month development project with Deutsche Bahn which concluded that DAS technology has the potential to significantly reduce the cost of sensing in the rail industry. The business also won a contract with a Class 1 Railroad operator to deliver a software platform in preparation for a wider rollout of DAS technology. Although growth in the upstream oil and gas market has been constrained by the low price of oil, the business has signed a strategic marketing agreement with Weatherford. In infrastructure security, OptaSense signed a two-year framework agreement to deliver two hundred units to protect critical national infrastructure for a customer in the Middle East.

The Space Business is currently developing the computer and avionics for ESA’s Proba 3 satellites to be launched in 2018 to study the sun. Other EMEA product orders placed during the first half of the year included a contract to develop an electronic hub-drive for military ground vehicles for the US Defence Advanced Research Projects Agency worth $2M, with an option for a further $3M. Commerce Decisions won its first contract through its Australian arm and was selected to deliver bid evaluation criteria that will be used to assess prospective warship designers for the Canadian Surface Combatant.

During the period the group received deferred consideration of £6.2M relating to last year’s sale of the US Services division and this seems to represent the final payment relating to this as no further consideration remains outstanding.

It can be seen above that there was a big increase in the current tax liability. This was primarily related to a liability encountered in the US following a court decision in respect of taxes payable on the group’s acquisition of Dominion Technology Resources in 2008. An insurance policy was taken out at the time and if the court’s decision is final, the funds required to settle the dispute will be provided by the insurers so an offsetting receivable is reported on the balance sheet and this will not have an effect on the overall cash position of the company.

The £150M share buyback was completed by the end of September and a further £50M share repurchase was initiated today which will be executed over the next year provided there are no other significant and better opportunities for investment within the business. The group have indicated that capital expenditure is likely to increase further as they continue to invest in the LTPA contract. Given the timing of the SDSR, the immediate priorities are to engage with customers to understand its impact and the emerging opportunities and to ensure that the group delivers their expected performance this year.

During the period Steve Wadey joined the group as CEO in April having previously been Managing Director of MBDA UK and Technical Director for the MBDA Group.

There seems to be some progress being made on the pension deficit. During the period it fell by £19M due to a £12.2M actuarial gain and a £7.9M contribution from the company. There has been no change to the cash contributions required under the recovery plan, however, which continues to require £13M of company contributions per annum until the end of March 2018.

In the UK, the Government’s Strategic Defence and Security Review, together with ongoing defence transformation, are expected to continue to have an impact on the UK defence market and in the rest of 2016 there will continue to be uncertainty and the potential for interruptions to order flow but the EMEA Services division’s performance as a whole is expected to remain steady this year. Although the performance of Global Products remains dependent on the timing and shipment of key orders, revenue under contract for this year is as anticipated at this stage and overall the board’s expectations for group performance this year remains unchanged.

After a 6% increase in the interim dividend the shares are now yielding 2.1% increasing to 2.2% on the full year forecast.

Overall then this has been a solid period of trading for the group. Profits were up but net assets were down, although it should be noted there was a share buyback exercise taking place during the period which would have reduced the equity. Operating cash flows did increase but this was due to a large one-off payment related to the early repayment of debt that occurred in the first half of last year. The fall in orders looks rather alarming but the receipt of a £153M order after the end of the half meant that there is a similar amount of forward earnings already contracted for as last year.

The trading environment is tough with budget constraints at both the MOD and DOD. In the UK, much hinges on the SDSR and the single source contract review, both of which are ongoing and offer some uncertainty. In the US it seems that a recovery is still fairly some way off but the board believe a trough may have been reached there. EMEA Services were flat and performing decently with the cyber division looking interesting despite the strong competition in that area. Global Products is faring less well, suffering from a lack of demand but profits were improved by cost cutting in the US.

Going forward the shares yield 2.2% and there is a new £50M share buyback. This is clearly a quality, cash generative business that is going through a tough time in its end markets at the moment and I am tempted to dip in here on weakness.

On the 11th December it was announced that the group had reached an agreement to sell Cyveillance, previously a business unit in the US Services division. It has been bought by LookingGlass Cyber Solutions for a cash consideration of $35M.

On the 27th January the group announced the appointment of Lynn Brubaker as a non-executive director. She has most recently been VP and General Manager of Commercial Aerospace at Honeywell International so sounds like a decent appointment.

On the 10th February the group released their Q3 trading update where they confirmed previous guidance for the group performance for 2016 was still relevant. The UK defence market remains uncertain, however. While the government’s strategic defence and security review was published in December, it is likely to take some time before its impact is clear. Additionally, the single source regulations office is not expecting to publish the single source profit rate for the next year until March.

The performance of EMEA Services was in line with expectations in the period and revenue under contract for this year is as expected, although the division has continued to experience some de-scoping and delay to orders. During the period the business won a contract with Motorola Solutions to provide monitoring, assessment and assurance services in support of the delivery of the UK Emergency Services Network. As announced previously it also secured a £153M five year renewal from the MOD for aircraft engineering support.

In December the group sold Cyveillance Inc to Looking Glass Cyber Solutions for net proceeds of £22M. The business is a former unit of the US Services division which was sold in 2014 and had revenues of $18M last year.

Trading in Global Products was as expected during the period, and revenue under contract for this year is also as anticipated, although its performance remains dependent on the timing and shipment of key orders in what is a shorter order cycle business. Among their new orders in the period, the OptaSense business was awarded a contract to protect about 2,000KM of pipeline which, once installed, will be the world’s largest distribution fibre sensing project. The total value of the project is more than $30M of which about half has been contracted with Optasense.

Overall, the board’s expectations for group performance in the current year remain unchanged.

It is also worth noting that the company purchased for cancellation from Merrill Lynch, 1,024 shares worth about £22.5K.

Overall then, not much has changed here. I am a little concerned about the fact that there seems to be potential for order slippages to affect Q4 so, having been stopped out earlier this month I have decided not to re-enter here yet.

On the 24th March the group confirmed that they were on course to meet their expectations for the year. EMEA Services continued to perform as expected. Earlier this month, the Australian business announced that it had been awarded a five-year follow on contract with rolling extensions for up to 15 years to provide aircraft structural integrity services for the Australian Defence Force. Trading in global products has been as expected in the period with the US products business winning small robot and survivability orders for both US and overseas customers.

In March the UK Secretary of State for Defence announced that next year’s baseline profit rate for single source defence contracts will be just under 9% compared with 10.6% this year. This new rate will apply to new or renewed qualifying contracts signed from April 2016 and acts as the starting point for individual contracts.

So, trading this year seems to be going OK but the reduction in profits on government contracts is unwelcome news.