Compass how now released its final results for the year ended 2015.

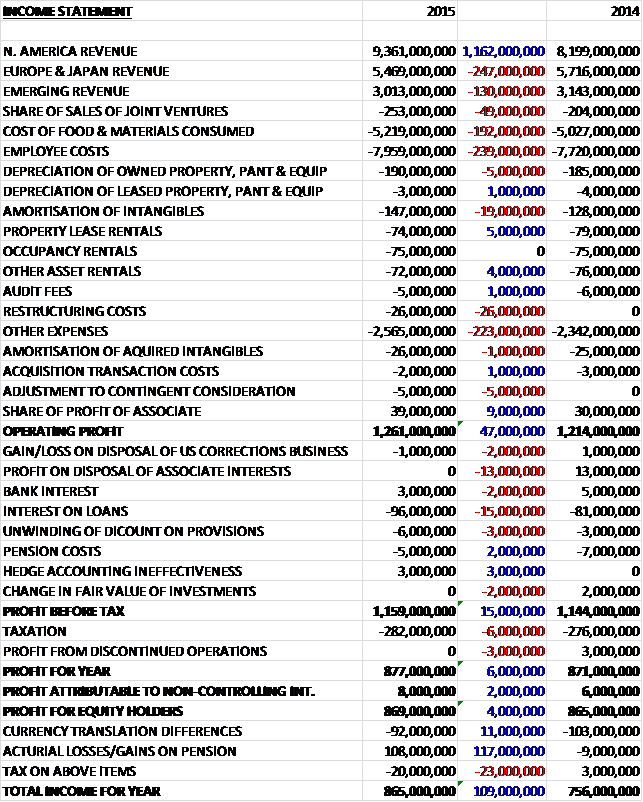

Revenues increased when compared to last year as a £247M decline in European and Japanese revenue and a £130M fall in Emerging Market revenue was more than offset by a £1.162BN growth in North American revenue. The cost of food and materials consumed grew by £192M and employee costs were up £239M with amortisation up £19M and other operating costs up £223M. There was £26M of restructuring costs that did not occur last year but despite this, operating profit increased by £47M. The loan interest then increased due to the additional debt required to finance the return of cash to shareholders (I really don’t understand the rationale of taking out debt to return cash to shareholders) and tax grew so that the profit for the year came in at £869M, an increase of just £4M year on year.

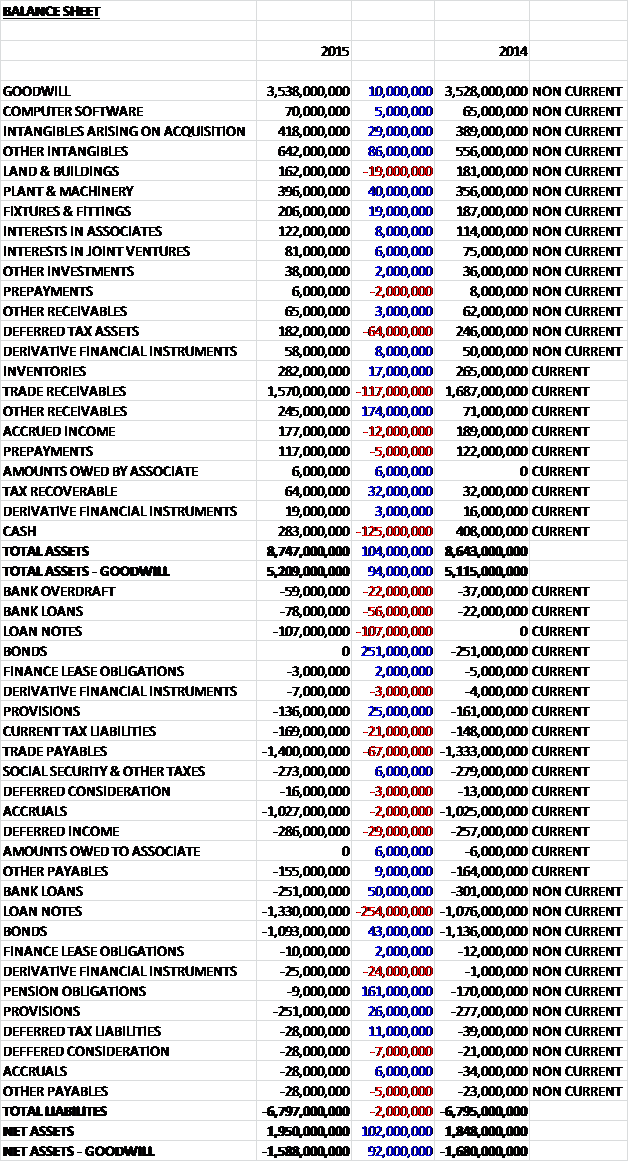

When compared to the end point of last year, total assets increased by £104M driven by a £174M growth in other current receivables, an £86M increase in other intangible assets, a £40M growth in plant and machinery, a £32M increase in current tax receivables and a £29M growth in acquired intangible assets, partially offset by a £117M fall in trade receivables, a £125M decline in cash, and a £64M decrease in deferred tax assets. Total liabilities also increased during the year as a £361M growth in loan notes, a £67M increase in trade payables, and a £29M growth in deferred income was partially offset by a £251M fall in bonds, and a £161M decline in pension obligations. If we discount goodwill, the end result is a net asset level of -£1.588BN, a positive movement of £92M year on year.

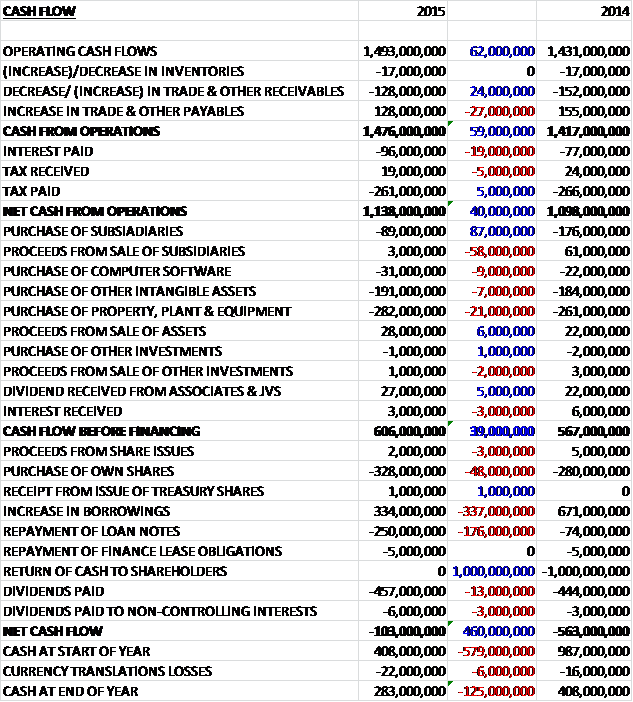

Before movements in working capital, cash profits increased by £62M. Working capital movements broadly cancelled each other out and after a higher amount of interest was paid, the net cash from operations was £1.138BN, an increase of £40M year on year. The group then spent £282M on property, plant & equipment, £191M on intangible assets and £89M on bolt-on acquisitions to give a free cash flow of £606M. Some £457M was paid out in dividends and more debt was taken out to buy £328M-worth of the company’s own shares to give a cash outflow for the year of £103M and a cash level at the year-end of £283M.

The underlying operating profit in North America was £768M, a growth of £96M year on year with the operating margin remaining static at 8.1%. This was driven by good new business wins and excellent retention rates. The group have seen some like for like volume improvement across most of the business which has been partly offset by volume and price weakness in the offshore and remote sector. The benefits from the ongoing efficiency programmes and the leveraging of the overhead base have been reinvested to drive and support the higher levels of growth and offset the impact of lower like for like in the offshore and remote sector, hence the flat margins.

Business and Industry has delivered good levels of net new business combined with some positive like for like volumes with contract wins including Kimberley Clark and Rogers Communications. In the healthcare and seniors sector, organic revenue growth was driven by new contracts for both food and support services including Genesis Health Systems. The group have also expanded their relationship with Community Health Systems through increased locations and services.

Organic revenue growth in the education sector came from net new business and increased levels of participation. Contract wins included Emory University, Chesterfield County Public Schools and Kennesaw State University. The sports and leisure business has delivered excellent organic revenue growth with near 100% retention and strong attendance levels at sporting events. Contract wins include the Mapfre Stadium, home of the Columbus Crew MLS team and Videotron Centre in Quebec City. The recent decline in key commodity prices has impacted like for like revenue in the offshore and remote business, however, new contracts continue to be won including Manitoba Hydro and Emera.

The underlying operating profit in Europe and Japan was £402M, a decline of £10M when compared to last year with margins that increased slightly from 7.2% and 7.3%. The organic revenue growth in the region was 1.9% in the full year and nearly 3% in the second half. This performance was driven by improving rates of net new business, reflecting the investments made over the last two years in the sales and retention teams. Like for like volumes remained broadly flat.

Accelerating levels of new business, especially in the UK, Spain and Japan, combined with improving retention rates across the region drove the positive net new performance. The group have expanded their relationship with several clients including Sony in Japan, Continental in Germany and the defence portfolio in France. They have won new contracts with the Universidad de Navarra and the Rafa Nadal Sports Centre, both in Spain; Weston Park and Entrust in the UK and a senior living contract with Le Noble Age in France. Retained contracts include the National College of Technology in Japan, ISE Andalucia in Spain, and the Edinburgh International Conference Centre, Kettering Hospital and the Ricoh Arena in the UK.

Like for like volumes in the UK, Germany and parts of Central Europe show an improving trend, but this is being offset by ongoing weakness in France and the exposure to the oil and gas market in the North Sea. The group continues to focus on operational efficiencies and cost reductions to support the growth that they are seeing and improve the operating margin, hence the small increase in margins seen.

The underlying operating profit in Fast Growing and Emerging markets was £218M, a fall of £8M when compared to 2014 on margins that remained steady. Organic revenue growth for the region was 6.9%. Emerging markets delivered organic revenue growth of 11% driven by strong new business which helped mitigate the decline in Australia.

In Australia, the offshore and remote business declined by 6% with clients reducing headcounts on site, construction projects coming to an end and some production contracts being mothballed. The group have won new business with BHP Billiton, however, to provide support services across several locations and they have retained contracts including Glencore. Other sectors continue to perform well and they won new business with the University of New England, multi-site contracts with both Mars and Nestle, and Target stores where they have developed an instore café offering.

The other offshore and remote business in the rest of the region has seen some growth driven by new business wins across Latin America, including, in Chile, BHP 7000 and Abengoa, a solar project in the Atacama Desert. This has more than offset the difficult oil and gas environment. They have just signed a new seven year contract with an existing client to build and operate a new remote camp in the CEMEAT region.

Double digit organic revenue growth in each of Brazil and Turkey reflected good new business wins, offset in part by some sharp declines in like for like volumes driven by challenging macroeconomic conditions. A continued focus on cost efficiencies has helped to partially mitigate the pressure from high cost inflation and declining volumes. New contract wins include the provision of multi services to Grupo Marista and food services to Coca Cola in Brazil and Doga schools and Carrefour in Turkey.

A strong new business performance in the Middle East included contracts with Al Ain Hospital, Corniche Hospital, Beach Mall and additional military sites. In South Africa they retained contracts with Nedbank and RCL Foods. Elsewhere in the region, New Zealand saw good levels of organic growth including the signing of a 15 year contract with the government to provide food services to public hospitals and the expansion of their relationship with the Defence Force. Double digit organic growth in India and China was driven by new business wins including SMIC Private School Shanghai and HAECO, an aircraft engineering group in Hong Kong.

The capital expenditure of £507M was slightly above the historic amount due to the investment in returning Europe to growth. It is believed that this rate will continue and in addition, next year they will be investing in a camp in their CAMEAT region as part of a long term contract extension with an existing client. As far as working capital is concerned, the board are expecting them to average out at a small outflow but net year there will also be a negative impact of around £70M due to the timing of the payroll run in September in the US and UK which will reverse in 2018.

During the year the group completed a number of small infill acquisitions in several countries for a total consideration of £93M, of which £76M was paid during the year with a further £13M of deferred consideration being paid relating to prior years. The acquired businesses contributed £6M to operating profit during the period. There were £230M of capital commitments contracted for but not provided for at the year-end with the majority of the commitments for intangible assets.

As announced previously the group is reducing their cost base in the offshore and remote business globally and in some emerging markets. This incremental restructuring cost of around £50M will be included in operating profit and this year some £26M was incurred, most of which was for labour cost reductions (£17M) and the rest as onerous contract provisions with the remaining £20M to £25M of restructuring costs to be incurred in 2016.

It is worth noting that the book value of goodwill attributable to Turkey is £70M with headroom of £27M. It is possible that changes in some key assumptions would cause the value of goodwill attributed to this country to fall below the carrying value which could lead to an impairment. This is not important to me but the market my view such an impairment differently.

Going forward, next year the board are changing the way they run the business and will adjust their regional reporting accordingly. These regions will be N. America, Europe (now including Turkey and Russia) and ROW (including Japan). This seems fairly sensible to me considering that emerging and fast growing margins no longer seem to be emerging or fast growing.

North America continues to deliver excellent growth, the business in Europe and Japan is enjoying a strong recovery and the fast growing and emerging regions performs fairly well despite lower volumes and pricing pressures in some parts of the market. The board’s expectations for 2016 are positive and unchanged. The pipeline of new contracts is strong, and the savings from the restructuring, together with the margin improvement in the rest of the group, are expected to offset the impact of lower volumes and pricing pressures in the fast growing and emerging region.

At the current share price the shares trade on a PE ratio of 21.3 which falls to 20.2 on next year’s consensus forecast. After an 11% increase in the total dividend, at the current share price the shares yield 2.6% which remains broadly the same on next year’s forecast and this year the group also bought back £328M of their own shares. The net debt at the year-end stood at £2.6BN compared to £2.371BN at the end of last year.

Overall then this has actually been a fairly good year for the group, Profits increased despite the restructuring costs, the operating cash flow improved and they continued to generate decent amounts of free cash. The net tangible asset level did improve, although it remained negative. The performance in North America has been very good but profits in both Europe and emerging markets fell due to currency headwinds – constant currency profits improved in both regions.

There are some headwinds, however. The offshore and remote business has been hit by the collapse in commodity prices and some emerging markets have become much more difficult with Brazil and Turkey causing particular problems. Indeed, the latter seems to be susceptible to a goodwill impairment.

Next year there will be further restructuring costs and with a PE of 20.2 and a dividend yield of 2.6% these shares look a bit too expensive to me despite their obvious appeal as a safe and steady ballast stock in a portfolio.

On the 11th December it was announced that director Alfredo Ruiz Plaza purchased 10,000 shares at a value of £112.8K. He now owns 64,746 shares in total – this seems to be a decent sized buy actually.

I have decided that these shares are probably a bit too expensive for me so this is likely to be my last update for Compass until the shares look a bit cheaper.