James Latham has now released its interim results for the year ending 2016.

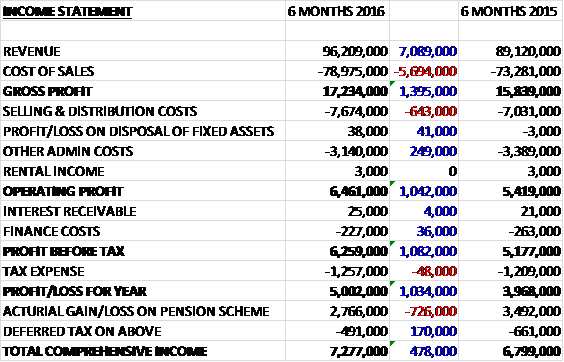

Revenues increased by £7.1M when compared to the first half of 2015 and after a growth in cost of sales, gross profits were £1.4M higher. Selling and distribution costs increased by £643K but admin costs fell and the operating profit grew by £1M. Finance costs fell modestly, reflecting reduced interest charges on the lower pension scheme deficit, but this was offset by a small growth in tax expenses to give a profit of £5M, a growth of £1M year on year.

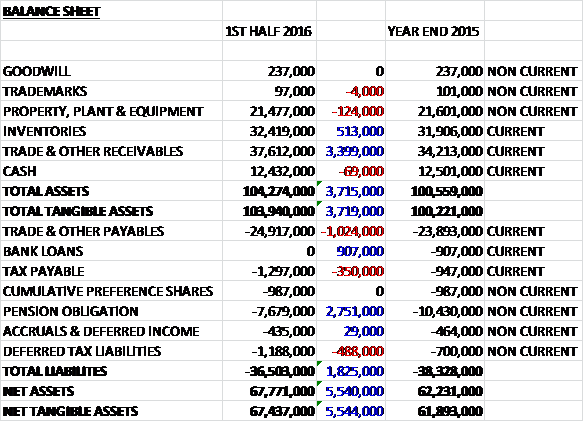

When compared to the end point of last year, total assets increased by £3.7M driven by a £3.4M growth in receivables, and a £513K increase in inventories. Total liabilities declined over the past six months as a £2.8M fall in the pension obligation was partially offset by a £1M growth in payables, a £488K increase in deferred tax liabilities and a £350K growth in current tax liabilities. The end result is a net tangible asset level of £67.4M, a growth of £5.5M over the past half year.

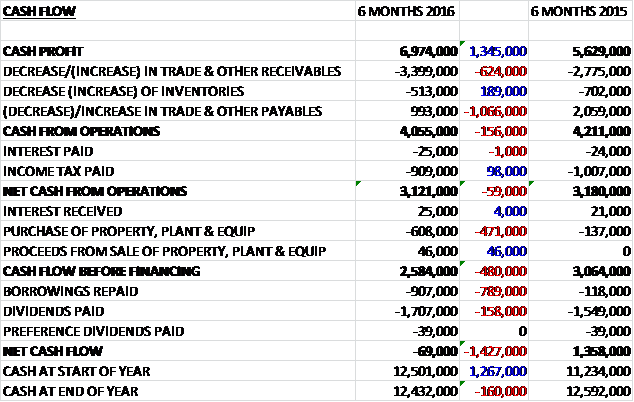

Before movements in working capital, cash profits increased by £1.3M to £7M. There was a cash outflow from working capital, in particular a £3.4M growth in receivables and after a slightly lower tax payment, the operating cash flow was £3.1M, broadly flat year on year. This easily covered the £608K spent on property, plant and equipment to give a free cash flow of £2.6M. The group then used this to repay £907K borrowings and to pay £1.7M in dividends which meant that the cash outflow for the half year was £69K with a cash level of £12.4M at the period-end.

Group revenue has grown as a result of higher sales volumes and product mix, which offset lower prices. This growth was both in panel products and timber with increased sales in decorative panels, doors, Accoya and WoodEx. Trading margins for the period are similar to the previous year with an improvement in panels and a small decline in timber. There were higher warehouse and distribution costs reflecting higher volumes handles and the extended working day at a number of depots but otherwise overheads have been well controlled and bad debts have been significantly lower than in previous periods. The group are continuing to take advantage of cash settlement discounts from suppliers where this represents a good return.

So far in the second half there has been growing revenues for October and early November, at slightly improved margins but market conditions continue to be difficult in some areas while improving in others. Overall, so far the group are trading comfortably in line with expectations. They are progressing with their plans to relocate the two oldest depots and are close to agreeing heads of terms on the new Yate site and are in negotiations for the new Wigston site.

From January 2016, Peter Latham will step down from being executive chairman and instead become non-executive chairman of the group with Nick Latham taking over most of the executive duties.

After an increase in the interim dividend, the shares are now yielding 1.9% which increases to 2% on the full year consensus forecast.

Overall, this has been another decent period for the group. Profits increased, as did net assets, aided by the pension deficit reduction. The operating cash flow did decline modestly but this was due to an increase in receivables and cash profits increased and once again, a good level of free cash has been generated. Although volumes are up, there has been a reduction in prices which should be watched but the new year has started well and, although the shares are not obviously that cheap with a forward PE of 15.4 and yield of 2%, and they are likely to get badly burned in the next UK economic downturn, this company seems to be doing well at this stage in the cycle and I am tempted to pick a few shares up.

On the 30th March the group released a trading statement. Revenue for the year is expected to be slightly lower than market expectations but pre-tax profit is likely to be higher. Quite light on detail, this, and not really much to go on.