Berkeley Group has now released its interim results for the year ending 2016.

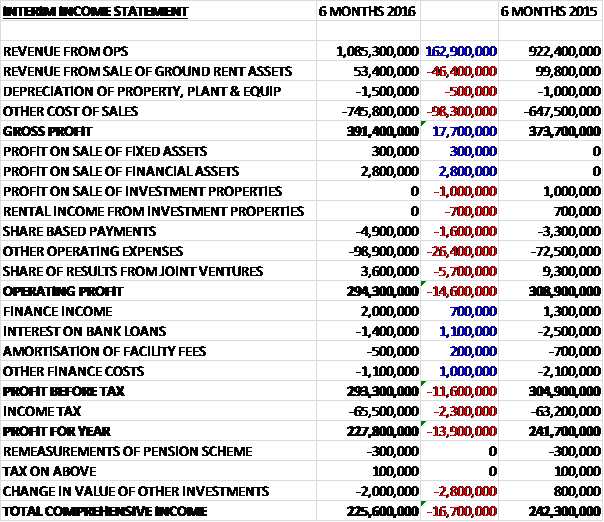

Revenues increased when compared to the first half of last year as a £46.4M decline in sales of ground rent assets was more than offset by a £162.9M growth in revenue from operations. Cost of sales also increased, which meant that gross profit was £17.7M ahead of last time. The group then made £2.8M on the sale of financial assets, offset by a £1.7M decline in income from investment properties and a £1.6M growth in share based payments. There was a £26.4M growth in other operating expenses, however, mainly as a result of the increased share scheme charge as the company’s share price increased (a £16.3M increase) and the group’s share of profits from joint ventures fell by £5.7M to give an operating profit some £14.6M below that of the first half of 2015. Finance costs did fall, but income tax increased to give a profit for the half year of £227.8M, a decline of £13.9M year on year.

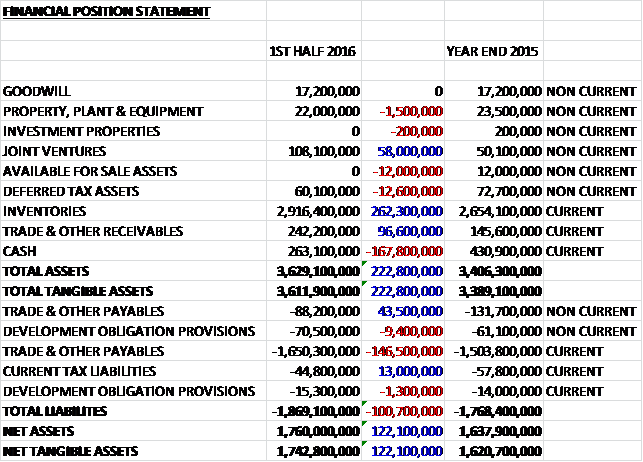

Total assets increased by £222.8M when compared to the end point of last year, driven by a £262.3M growth in inventories relating to land under development and work in progress, a £96.6M increase in receivables despite a reduction in receivables from joint ventures and a £58M growth in the value of the investment in joint ventures, partially offset by a £167.8M fall in cash, a 12.6M decline in deferred tax assets and a £12M sale of the available for sale assets. Total liabilities also increased during the period as a £103M growth in payables due to an increase in trade payables provisions and a £10.7M increase in provisions was partially offset by a £13M fall in current tax liabilities. The end result is a net tangible asset level of £1.724BN, a growth of £122.1M over the past six months.

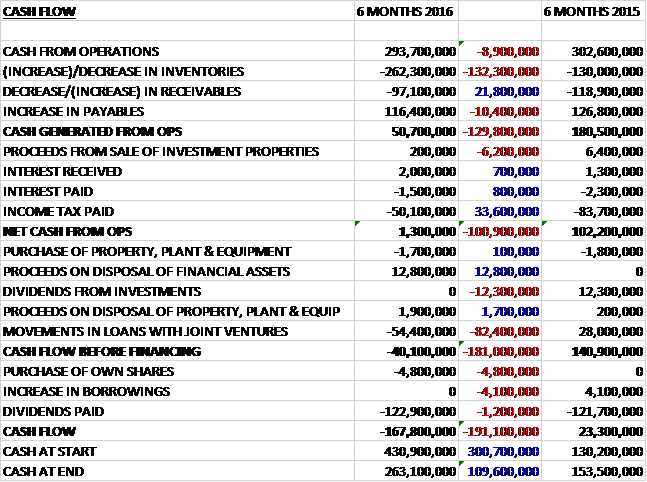

Before movements in working capital, cash profits fell by £8.9M to £293.7M. There was then a cash outflow through working capital with a large growth in inventories, partially offset by a £33.6M reduction in tax payments. This meant that the net cash from operations was just £1.3M, a decline of £100.9M year on year. The group then loaned a further £54.4M to joint ventures but received £12.8M from the sale of financial assets to give a cash outflow of £40.1M before financing. We then see some £122.9M spent on dividends along with a modest purchase of shares (no doubt to satisfy the director payments) to give a cash outflow of £167.8M for the period and a cash level of £263.1M at the end of the half.

The first six months of the year have seen a stable operating environment, supported by the decisive general election result, in which normal transaction levels experienced are consistent with the equivalent period last year. Sales price increases have continued in line with those reported in the wider market and are generally matched by cost increases. The cash due on forward sales over the next three years has increased by £137M to £3.096BN. The period saw the group’s launch of their new scheme at South Quay Plaza in Docklands along with launches of new phases on a number of other schemes. They continue to see good demand on both new and existing schemes, with domestic demand remaining strong and London continuing to attract inward investment from the UK and overseas. Cancellation rates of around 10% remain below the normal historic levels of 15% to 20% and completed stock remains at historically low levels with 39 completed residential properties held in the inventory at the period-end.

The total revenue from operations included £1.067BN of residential revenue and £18.5M of commercial revenue and there were no land sales in the period. A total of 2,091 new houses were sold across the SE at an average selling price of £506K compared to 1,372 at an average price of £649K in the first half of last year. The reduction in selling price reflects the mix of schemes completing in the period which were principally Riverlight and Goodmans Fields compared to the first completions at Ebury Square last time where the average selling price was some £6.4M!

The commercial revenue included the sale of 65,000 square feet of office, retail and leisure space across a number of the group’s developments including Battersea Reach, Langham Square, Fulham Reach, and Marine Wharf. This represented an increase of £8.4M over last time when the sales included 25,000 square feet of space at Fulham Reach, Langham Square and Worcester.

During the year the group sold a further portfolio of ground rent assets across some 43 sites for proceeds of £53.4M and a gross profit of £51M which is a decline of £34.1M year on year. This latest sale completes the disposal of the historic ground rent assets and there are no further assets ready for sale.

The group’s land bank of 38,233 plots (37,473 last year) is a combination of owned or contracted sites, most of which have a planning consent and are in construction with an average selling price of £473K (£456K last year). They also hold a strategic pipeline of long-term options for over 5,000 plots. The group has secured 14 planning consents this year, five on schemes which did not previously have an implementable planning consent, and nine revised consents. The new consents include 73 homes at Latchmere House in Ham, some 1,400 homes at White City, 594 homes at Southwater in Sussex and 247 homes at Taplow in Berkshire, in addition to over 800 homes at St. William’s site in Battersea. The revised consents include Royal Arsenal Riverside, Fleet, West Horsham, 190 Strand, Wimbledon Hill Park, Goodmans Fields, Royal Wells Park, Kingston Gas Works and Woodberry Down.

Four new sites have been acquired unconditionally during the year, West End Green in Paddington as well as sites in Wokingham, Cockfosters and Southwater, the latter having come through from the group’s strategic land. Two have been acquired on a conditional basis, including a site in Blackheath and the Fulham Gas Works site which is contracted to St. William. A the period-end, the group has 75 sites in its land holdings, of which 56 have an implementable planning consent and are in construction. Of the remaining 19 sites, two have an implementable consent and will shortly move into construction and nine have at least a resolution to grant planning consent. A further eight remain in the planning process, of which six are under conditional contracts.

The group’s share of profits from joint ventures was £3.6M, a decline of £5.7M and principally reflected a further 78 completions at 375 Kensington High Street and Stanmore Place. St. Edward has four schemes currently in development at Stanmore Place, 375 Kensington High Street, 190 Strand, and launched in this period, Green Park in Reading. 78 homes were sold in the period at an average selling price of £1M compared to 86 at £1.4M last time which reflects the mix of properties sold, predominantly 375 Kensington High Street. Some 2,038 plots in the group’s land holdings relate to St. Edward schemes and the business controls a commercial site in Westminster which has a detailed planning consent but will not move into development until the premises are vacated by the current tenant (no indication of when that might be).

2,425 plots on three sites in the group’s land holdings relate to St. William schemes. This joint venture with National Grid has the potential to deliver some 7,000 plots from an initial ten sites and is a clear source of future land. The sites in the land bank currently are at Battersea, Rickmansworth with the latter having contracted in the period.

The net promoter score for the group continues to be a key differentiator and at 69.8 is ahead of its industry peers. The group have also recently completed the development of a new product called the Urban Family House, which is designed to make higher density urban living work for families and deliver 50% more homes per hectare than standard terraced housing. It apparently maximises living space and provides every amenity that a modern family needs while making the very best use of land.

The group has been selected as the GLA’s preferred bidder on a 27 acre former Parcelforce site at Stephenson Street, adjacent to West Ham station which seems to have serious potential.

As well as the over-riding cyclicality of the industry, there obviously remain some short-term risks which include the upcoming EU referendum and the potential for continued changes to property taxation which may end up having an adverse effect on the housebuilding industry.

The group has some £575M of unused banking facilities so is very well covered and they are currently in a net cash position of £263.1M compared to £148.4M at the same point of last year and £430.9M at the year-end. At the current share price, the shares are yielding 4.9% which increases to 5.2% on the full year consensus forecast with a proposed £2 dividend to be paid every year until 2021.

Overall then this was another decent performance from the group. Profits did fall year on year but this was attributable to lower sales of ground rent assets and the ridiculous charges related to the share scheme. Net assets improved but the operating cash flow deteriorated with the large increase in inventories meaning there was no free cash generated during the period. Overall the housing market has been stable and the number of homes sold by the group has increased. The average price achieved for these homes has fallen but this was due to a very high end development at Ebury square completing last year.

There are a number of potential banana skins this year with the likely interest rate hike and EU referendum probably the most obvious, and with a PE ratio of 15.9 predicted this year the shares do not appear initially cheap. With a big net cash position, however, and a dividend yield of 5.2% they are actually better value than this metric shows in my opinion. I am very tempted to dip in here.

On the 19th January the group announced that a director in the company, Mr. Brightmore-Armour purchased 1,000 shares at a value of £37K which represents his maiden share purchase.

On the 18th March the group released a trading update covering November to February. The London housing market has remained stable over the period and they are seeing good underlying demand for their properties, with cash due on forward sales in excess of £3BN. Reservations are approximately 4% lower than in last year due to a change in mix of product and the strength of the forward sales secured in recent years. Transaction levels at the upper end of the housing market have been affected by the significant increase in transaction taxes over the last year and a half which will have consequential effects on the supply of new homes. Since the half year-end, they have sold 62 properties at prices over £2M, a similar number to the same period last year when the market slowed in the run up to the general election.

The group remains on course to deliver £2BN of pre-tax profit over the three years to 2018. For the current year, the board expects results to be at the top end of expectations after absorbing about £25M of accelerated operating expenses following the changes to the 2011 LTIP (that’s a huge amount!). At the end of April, they expect to see net cash in the region of £100M, allowing for further land expenditure.

The group have acquired four sites in the period, including two conditionally contracted long term regeneration schemes. These are the Oval Gasworks, adjacent to the Oval cricket ground in Lambeth and an 11.2 acre site in Hornsey which has been acquired by St. William. In addition, two sites have been contracted outside of London: a 23 acre site in Ascot which has been acquired unconditionally and a 12 acre site in Cookham contracted on a subject to planning basis. They have also made good progress in the period in enhancing their land holdings through three new and nine revised planning consents. The new consents are in Sevenoaks, Winchester and Kingston.