The group now has two divisions. Begbies Traynor is an insolvency, restructuring and investigations consultancy. Edisons was acquired in December 2014 and now makes up the property consultancy division. It is a national firm of chartered surveyors, providing services to banks, insolvency practitioners and owners of commercial property. They are now positioned so that their earnings are hopefully a little less counter-cyclical.

The Begbies Traynor division provides corporate insolvency which aims to either rescue the business or realise the value of assets and distribute any available funds to creditors; personal insolvency where they provide advice to debtors and creditors on all aspects of personal insolvency; and restructuring & financial consulting where they provide consulting services to businesses, professional advisors and financial institutions on debt refinancing, business valuations, corporate finance and business reviews together with conduct of financial investigations and due diligence.

The services offered at Eddisons include the valuation and sale of property, machinery and business assets including fixed charge property receiverships, insolvency insurance brokerage, property and facilities management and building consultancy services such as lease advisory, dilapidations advice and rating reviews. The group recognised revenue when the account can be reliably measured and its probable economic benefits will flow. Services provided to clients, which at the balance sheet date have not been billed are recognised as unbilled revenue.

The company has now released its final results for the year ended 2015.

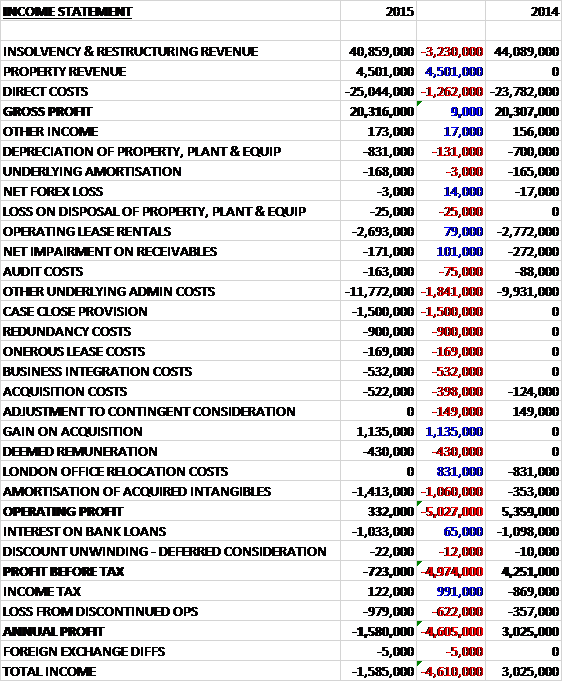

Revenues increased when compared to last year as a £3.2M fall in insolvency and restructuring revenue was more than offset by a £4.5M growth in property revenue. After direct costs, however, the gross profit was flat year on year. We then see a £131K increase in depreciation and a £1.8M growth in other underlying admin costs along with a £1.5M case close provision charge, £900K of redundancy costs, a £430K charge relating to deemed remuneration and £532K of business integration costs, all of which did not occur in 2014. In addition there was a £398K growth in acquisition costs and a £1.1M increase in the amortisation of acquired intangibles.

On the other hand, there was a £1.1M gain on acquisition and no London office relocation costs that were £831K last year. The result of all this is an operating profit that has fallen by £5M when compared to 2014. Finance costs were slightly lower but there was a £991K swing to a tax rebate, partially offset by a £622K increase in the loss from the discontinued operation to give an annual loss of £1.6M, a detrimental movement of £4.6M year on year.

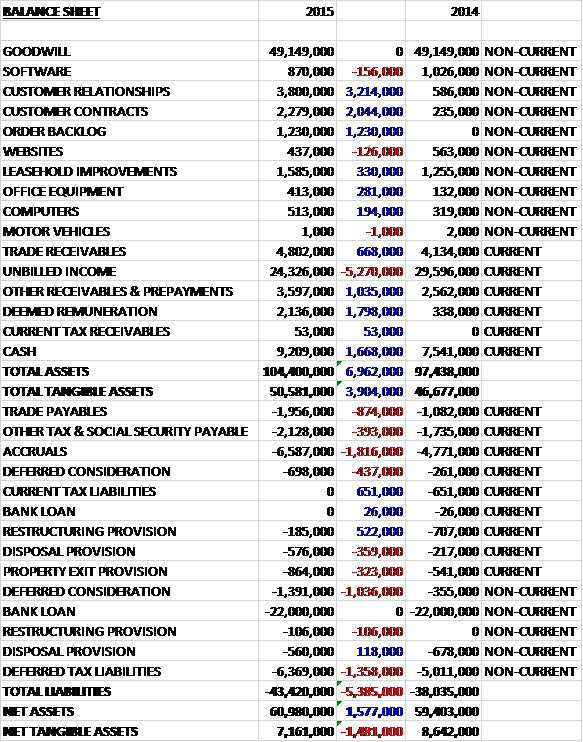

When compared to the end point of last year, total assets increased by £7M driven by a £3.2M growth in customer relationships, a £2M growth in customer contracts, a £1.2M increase in order backlogs, a £1.8M growth in deemed remuneration, a £1.7M increase in cash and a £1M growth in other receivables and prepayments, partially offset by a £5.3M decline in unbilled income. Total liabilities also increased during the year due to a £1.8M growth in accruals, a £1.4M increase in deferred tax liabilities and a £1.5M growth in deferred consideration. The end result is a net tangible asset level of £7.2M, a decline of £1.5M year on year.

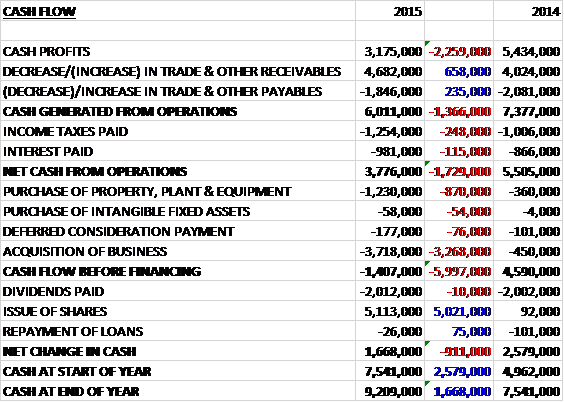

Before movements in working capital, cash profits declined by £2.3M to £3.2M. There was a cash inflow from a decrease in receivables but this was offset by more tax and interest so the net cash from operations came in at £3.8M, a fall of £1.8M year on year. The group spent £1.2M on fixed tangible assets, mainly relating to the new London office, and £177K on deferred consideration before £3.7M was spent on acquisitions to give a cash outflow of £1.4M before financing. The group then issued new shares which brought in £2M, enabling them to pay a dividend (I really don’t see the logic in issuing more shares and declaring a dividend!) and have a cash inflow of £1.7M for the year and a cash level of £9.2M at the year-end.

The discontinued operations include the global risk partners division and this year’s loss from discontinued operations includes a £570K loss on disposal. During the year the group invested in their London office with the team moving to new premises in Canary Wharf; and after the year-end they launched BTG Global Advisory, a new international alliance of independent insolvency, restructuring and financial advisory firms operating in key global jurisdictions (that’s as clear as mud then).

It was another difficult year for the insolvency industry with national volumes at their lowest level since 2007, falling from 18,994 to 16,380 and in addition, the insolvencies in Q1 2015 were just 4,014, the lowest quarterly level since Q4 2007, although these levels have now stabilised through the year. There has also been a change in the means of generating SME insolvency cases in recent years with the increasing use of internet-based marketing techniques.

The segment result in the Insolvency and Restructuring business was £8.5M, a decline of £2.3M year on year. The reduced level of market activity led to lower insolvency appointments for the group, which combined with the ongoing pressure on fee rates, caused the reduced revenue levels in the year. During the year the group restructured the division in response to the lower levels of market activity, together with discontinuing the loss-making global risk partners division. As a result of these cost-cutting actions completed this year, the cost base will reduce by some £1.5M in the new financial year.

The group will continue to develop this division through a combination of senior recruitment, acquisitions and staff development with the intention of increasing their market share, although they are already the market leader. Further development over the medium term could come from winning higher value, more complex instructions from existing clients and prospects.

The segment result in the Property business was £744K which represents the division’s maiden profit after being acquired in December 2014. The team is being appointed on a number of the group’s insolvency cases. In addition, operating synergies, through shared property and other overhead costs, are being realised in line with board plans. It is intended that the division will be developed through a combination of senior recruitment and acquisitions with the intention of developing the service offering and geographical coverage.

During the year the group made a number of acquisitions. Two insolvency practices were acquired – Ian Franses Associates in June 2014, a London-based insolvency practice; and Broadbents Business Recovery Services in April 2015, a Yorkshire-based insolvency practice. The total consideration was just over £1M satisfied by £800K in cash and £270K contingent consideration. The businesses have £1.2M in net assets which included £1.5M in intangible assets. Since the date of the acquisition, they contributed £357K to pre-tax profits so these look like good deals.

In December the group also acquired Eddisons Commercial Holdings, a property services consultancy. The total consideration was £7.6M which consisted of £6.3M in cash and £1.3M of contingent consideration deemed remuneration. The acquisition comes with £6.4M of net assets with £6.3M of those being intangible. The business contributed £511K to group pre-tax profit in the five months since its acquisition.

There are quite a lot of related party transactions at the group. Various properties used by members of the group during the year are owned by Ric Traynor, a director of the company. Rent paid on those properties totalled £720K which actually seems like quite a lot. Also, one commercial property used by the group is part owned by director Mark Fry which cost £85K in rent and he part owns a company which provides archiving facilities to the group which cost £24K. Finally Ric Traynor owns a company called Red Flag Alert and Begbies was charged a fee of £150K for use of their quarterly stats. These are probably all fine but it is worth keeping an eye on all of these items.

The group has principle banking facilities of £30M of which £22M has been drawn down. There are also £7.8M of non-cancellable operating leases outstanding. One thing worth noting is the number of receivables that are past their due date with about half of them overdue. This is as a result of the kind of work that the company which also means there are fairly large receivable impairments to contend with too. Presumably the group charges enough to take this into account. Due to the fairly sizeable debt here, the group is also somewhat susceptible to interest rate increases with a fifty basis point increase giving rise to a profit reduction of £71K, although there is probably a natural hedge with insolvencies likely to increase in this eventuality. The group also operates a defined contribution pension which cost £925K this year.

In addition to the above risks, the operating risks really relate to the macroeconomic environment where assignments run counter-cyclically. Also, the fact that the group operates in regulated markets gives rise to potential risks.

In December the group completed a share placing of 13,094,982 shares at a price of 40.5p per share in order to raise £5.3M which is a little disappointing to see.

Activity levels in the insolvency market have stabilised over the past year but there are no indications of a change in the benign financing environment in the UK and the board therefore remained cautious about activity levels in the near term. The combination of the reduced cost base in the insolvency division, the removal of losses from the discontinued business and the full year impact of the Eddisons acquisition, however, should leave the group well placed over the next year.

At the year-end, net debt stood at £12.8M compared to £14.5M at the end of last year. After the dividend was kept the same, the shares currently yield 5% which is what is expected for next year’s dividend yield too. As the group made a loss, we can’t use the PE ratio as a method of valuation but on next year’s consensus forecast, the shares trade on a PE ratio of 13.9.

Overall then, this has been a tough year for the group. They swung to a loss during the year and even when the plethora of “non-underlying” items are taken off, the performance was still below that of last year. Net assets also declined and operating cash flow declined with now cash left after the acquisitions to pay the dividend. The core insolvency business is struggling due to the benign financing conditions in the country, although the decline seems to have stabilised and the much smaller property division contributed its first profit to the group.

The insolvency acquisitions look good value and the Eddisons purchase was definitely important in order to diversify earnings a bit. Going forward, business is likely to remain difficult but the sale of the loss making discontinued operation and the reduction in the cost base of the insolvency division should improve the bottom line next year. With a forward PE of 13.9 and dividend yield of 5% these shares are not expensive and are looking a bit interesting in my view.