Begbies Traynor has now released its interim results for the year ending 2016.

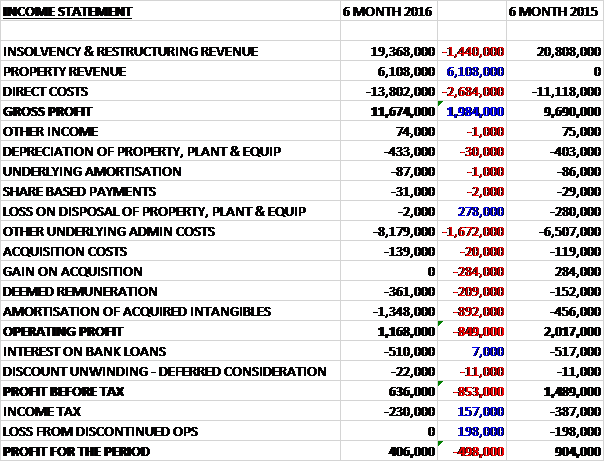

Revenues increased when compared to the first half of last year as the £1.4M decline in insolvency and restructuring revenue was more than offset by a £6.1M property revenue. Direct costs increased somewhat, but the gross profit was some £2M ahead. We then see a £278K decline in the loss on disposal of fixed assets but other underlying admin costs were up £1.7M. We also see the lack of the £284K gain on acquisition that occurred last time along with a £209K growth in deemed remuneration and an £892K increase in the amortisation of acquired intangibles which meant that operating profit fell by £849K. Finance costs were broadly flat but the tax charge was £157K lower and there was no loss from the discontinued operation which cost £198K last time. The end result is a half year profit of £406K, a decline of £498K year on year.

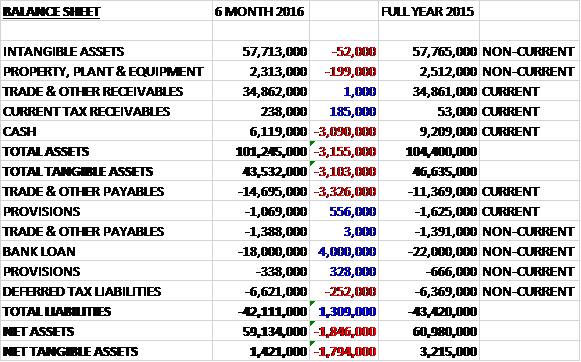

When compared to the end point of last year, total assets declined by £3.1M driven by a £3.1M fall in cash levels, and a £199K decline in property, plant & equipment partially offset by a £185K growth in current tax receivables. Total liabilities also declined as a £4M reduction in the bank loan and an £884K fall in provisions was partially offset by a £3.3M increase in payables and a £252K growth in deferred tax liabilities. The end result is a net tangible asset level of just £1.4M, a decline of £1.8M over the past six months.

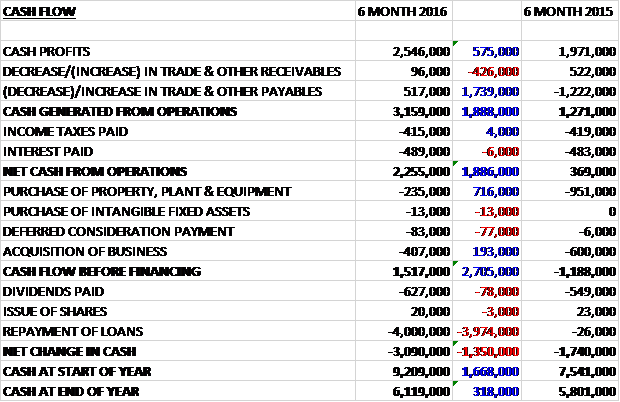

Before movements in working capital, cash profits increased by £575K to £2.5M. There was also an inflow from working capital, in particular and increase in payables which, after flat tax and interest payments, meant that the net cash from operations came in at £2.3M, a growth of £1.9M year on year. The group then spent £248K on capex along with £83K of deferred consideration and £407K on acquisitions to give a free cash flow of £1.5M. This did not cover the £4M of loan repayments, let alone the dividends, however, and the cash outflow for the half year stood at £3.1M to give a cash level of £6.1M at the end of the half.

The underlying EBITDA in the insolvency and restructuring business is £4.3M, a decline of £361K year on year. The insolvency market continues to be challenging with a further 10% reduction in the number of UK insolvencies over the course of the period which are now at their lowest level since 2007. The overall market conditions have led to reductions in revenue in the division but the impact has been somewhat mitigated by thorough cost control and operating margins were broadly maintained. Progress has been made in increasing market share which has been further enhanced by the acquisition of P&A.

The underlying EBITDA in the property business is £1.2M and this was the first contribution from the division, although pre-acquisition EBITDA was £1M. The integration of the Eddisons business into the group has proceeded well with synergy savings exceeding the initial targets with a further £500K of annual synergy savings on top of the £500K already identified which has led to operating margins increasing from 14.1% to 19%, further helped by the exit of non-profitable contracts. After the period-end, they completed the acquisition of Taylors, a specialist business property valuation consultancy which will add further depth to the group’s capabilities in this division.

In September the group acquired the P&A Sheffield team who are a significant regional provider of business recovery and insolvency services with a strength in asset based lending and creditor services out of administration for an initial consideration of £400K and a contingent consideration of £500K. After the year end the group acquired Taylors Business Surveyors and Valuers which specialises in providing commercial business and property valuations for secured lending purposes on behalf of a wide range of financial institutions, including all of the major high street banks. Taylors was acquired for a maximum consideration of £1.9M with an initial consideration of £500K in cash and £600K through the issue of shares along with deferred consideration of up to £750K. It made a pre-tax profit of £200K last year.

As there are no indications of a change to the benign financing environment in the UK which would cause an increase in insolvency levels, the board remains cautious about activity levels in the division in the near term and are focusing on cost control. Overall, their expectations for the year remain unchanged and they have stated they are still looking for acquisitions.

At the current share price, the shares are trading on a forward PE of 13.9 and have a dividend yield of 5% after the interim dividend was maintained. They were in a net debt position of £11.9M at the end of the half compared to £16.2M at the same point of last time.

Overall then this has been another difficult period. Profits have fallen but this was only due to the recent acquisitions, net assets have also declined but the operating cash flow has shown an improvement with the group now generating some free cash, albeit not enough to cover debt repayments. The insolvency market remains difficult, with a further decline in business over the period but the property division is now contributing to profits with some good cost synergies generated. The acquisitions look a good fit but I would like to see less reliance on so much debt.

Overall, expectations are unchanged and with reducing debt, a PE of 13.9 and yield of 5%, these shares look decent value to me.

On the 10th March the group released a trading update covering Q3. Performance has been consistent with the outlook reported at the time of the half year results with both divisions performing as anticipated. The estimated number of company insolvencies in England and Wales for 2015 was 14,629, a decrease of 10.3% when compared to 2014, and the lowest level since 1989.

On the 3rd June the group announced the acquisition of Pugh Auctions for an initial cash consideration of £2M from existing resources. Additional contingent consideration of up to £2.6M will become payable subject to the achievement of financial targets in the five years following the transaction. Pugh is the largest firm of commercial property auctioneers operating outside London with regular auctions being held in Leeds and Manchester. They had no assets to speak of and last year generated pre-tac profits of £800K. The acquisition is expected to be earnings enhancing in the current year so this looks like a good deal to me.