Ashley House operates in the design, construction management and management services space in the UK. The principle activities are design, construction management, consultancy and asset management services primarily working with providers of health and social care on infrastructure developments from project inception to completion of construction and beyond.

Construction contract revenues are recognised under the percentage of completion method. Where the outcome of a construction contract can be reliably estimated, revenue and costs are recognised to the stage of completion of the contract activity at the balance sheet date. Where the outcome of a construction contract can’t be estimated reliably, contract revenue is recognised to the extent of contract costs incurred where it is probable that they will be recoverable. Contract costs are recognised as expenses in the period in which they are incurred and when it is probable that total contract costs will exceed total contract revenue, the expected total loss is recognised as an expense immediately.

Design and development fees are recognised as the service is provided and where it is possible that total costs will exceed total contract revenue, the expected loss is recognised as an expense immediately. Asset management fees relate to the provision of services to manage property assets and revenue is also recognised as the service is provided.

The group has a number of associates and joint ventures. Infracare, AHBB ELL and AHBB LHIL operate in the NHS Local Improvement Finance Trust arena. They are public private partnerships which provide purpose built premises for health and local authority services in England. They are jointly held with Amber Infrastructure with Ashley House having control over development activities and Amber having control of investment activities. The group jointly controls IPC Plus and Wilco Plus with groups of GPs and these businesses are engaged in providing clinical services in West Sussex and Wiltshire respectively.

The group also owns a share in Best Practice which provides a healthspace facility for use by local healthcare practitioners in Hampshire and is owned with two GPs. In addition, they own a share in Portsmouth Health which provides clinical services in Hampshire and is also owned with a group of GPs. Ashley House has now released its final results for the year ended 2015.

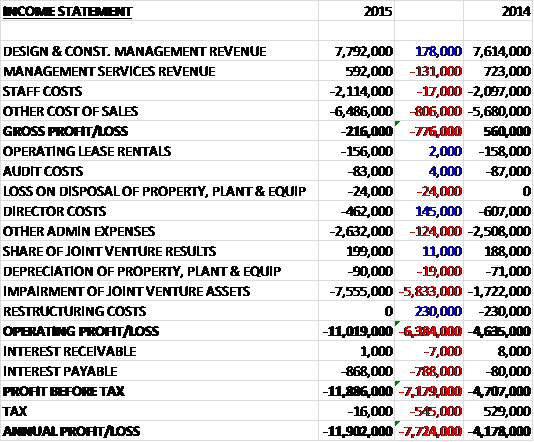

Revenues increased slightly as a £131K decline in management services revenue was more than offset by a £178K growth in design and construction management revenue. Staff costs were broadly flat but other cost of sales grew which meant that the gross loss was £216K, a detrimental movement of £776K over last year. We then see a £24K loss on disposal of property, plant and equipment offset by a decline in other admin expenses relating to reduced director pay and there were no restructuring costs which accounted for £230K last year. We do have a £5.8M growth in joint venture asset impairments though, which gave an operating loss of £11M, an increase of £6.4M. Interest costs then increased by £788K and a small tax expense represented a £545K adverse movement over 2014 as some expenses were not deductible for tax purposes so that the annual loss came in at £11.9M, an increase of £7.7M year on year.

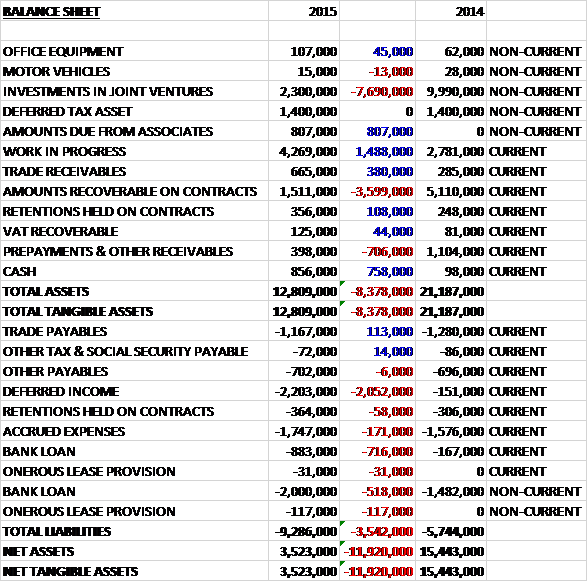

Total assets declined by £8.4M when compared to last year, driven by a £7.7M impairment of the investment in joint ventures, a £3.6M fall on amounts recoverable on contracts and a £706K reduction in prepayments and other receivables, partially offset by a £1.5M growth in work in progress, an £807K increase on amounts due from associated companies and a £758K growth in cash. Total liabilities increased during the year due to a £2.1M growth in deferred income and a £1.2M increase in borrowings. The end result is a net tangible asset level of £3.5M, a decline of £11.9M year on year – pretty poor stuff.

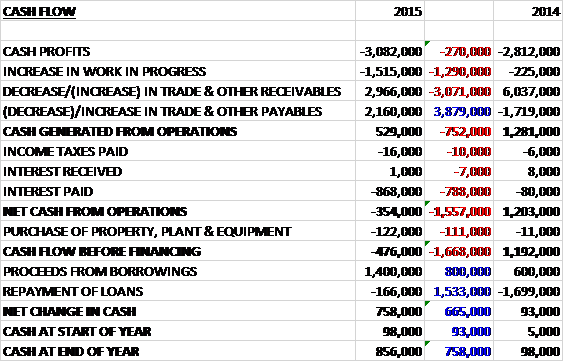

Before movements in working capital, cash losses widened by £270K to £3.1M. There was a cash inflow from working capital, however, with a fall in receivables and a growth in payables but the effect was less than last year and the net cash from operations was £529K, a decline of £752K year on year. We also see a bit of growth in interest paid so that there was a net cash outflow of £354K from operations, an adverse movement of £1.7M on last year. Capex was low at just £122K but the group still needed to take out some more borrowings which gave a cash inflow of £758K for the year and a cash level of £856K at the year-end.

The loss in the design and construction management division was £457K compared to a profit of £161K last year and the profit in the management services business was £440K, a decline of £106K year on year. The pipeline of schemes continues to grow in both quality and quantity, though, dominated by Extra Care schemes. Good progress has been made during the year with four schemes on-site at the year-end. Both of the flagship schemes at Harwich and Walton are progressing to plan and are expected to reach financial close this year, contributing about £21M to revenues over the next two years as they are built out.

The health business continued to be slow but there are signs of activity, albeit on a much reduced level. The group are currently contracted on a number of schemes and projects for a GP surgery in Danbury and a Pathology Lab in Basildon are underway, contributing about £1.4M of revenue during the year. Both the scheme at Dabury and the next three health schemes are forward funded and the group is looking to do more in this area. During the year the group completed an extension and refurb to GP premises in Hillingdon. The outlook for health is considered to be improving with some small signs of recovery in the market, but not as quick as the board would like. Nonetheless they remain committed to the sector.

The group were appointed as property partner for two organisations: HSN Care with whom they are developing a pipeline of housing designed for profoundly disabled adults and where they are now in advanced stages with three schemes; and national charity Hft who provide services for people with learning disabilities throughout England.

The company has signed a funding and partnership agreement with Funding Affordable Homes which is a newly established investment company set up to serve investors in the affordable homes sector. They have agreed to work together on the development and delivery of affordable Extra Care housing for older people. The schemes will be forward funded by FAH during construction and through to completion allowing the group to develop the business without needing to grow external debt and this arrangement will give them a much needed boost to their current pipeline delivery.

The group has won a place on North Yorkshire County Council’s Extra Care Housing Framework to design, fund, build, deliver and asset manage Extra Care accommodation in various locations in York and North Yorkshire. This appointment is apparently not guaranteed to bring any work but the framework will be used by other bodies looking to commission services. The board believe that the market for Extra Care Housing is growing. During the year the first Extra Care scheme undertaken by the group was completed in Grimsby. It was a development of 60 flats providing purpose-built accommodation for vulnerable older people.

In the immediate future it is likely that revenue streams will be variable but more predictable as the emphasis swings towards the construction phase of pipeline delivery and as the scheme volumes increase, this should have a smoothing effect on volatility. The growth in the pipeline continues to be dominated by Extra Care projects which have increased from £106.8M to £148.5M during the year, of which two schemes at a value of £12.4M are on-site. The health pipeline currently stands at £31.9M across 13 schemes with two schemes worth £5.1M currently on-site.

The current economic conditions create uncertainty over the level of new schemes required by the company’s social housing clients; the level of new schemes required by the NHS; the contribution earned to cover the cost base; and the availability of finance within the sector. The group is very reliant on their largest client, Coal Pension Properties led who represent and astonishing 52% of total revenues so this reliance is a key risk.

As far as financing is concerned, the group has a £2M development finance facility with Novus which has been fully drawn down with the first tranche of £740K due by August 2016 and the second tranche of £1.3M payable in November 2016. One of the joint ventures also has a bank loan of £883K from Lloyds and the group also has an undrawn overdraft of £500K available at pretty extortionate exchange rates.

In July the company received an approach to acquire its interest in the NHS LIFT joint ventures. This is now unlikely to complete in the structure first envisaged due to a number of complexities (no hint as to what they might be). Following these discussions the board conducted a full impairment review and in light of the very low activity within the NHS estate they have written down the value to just £2.3M which led to an impairment of £7.6M as the board has anticipated that whilst the LIFT arrangements may still have value at the end of their exclusivity periods, it is prudent to revise the useful economic life to nine and a half years, which is the average remaining period of exclusivity.

During the year the group sold its interest in Best Practice to Portsmouth Health for a consideration of £1. All amounts due to the group from the business have been incorporated in a formalised loan which is interest free for the first four years by which point, the board expect it to be repaid. There is no indication as to why the group has done this but it doesn’t sound like this is a great deal!

Interestingly in September 2013 the group granted options to some directions with an exercise price of 15p but they will not be exercisable until the share price reaches 37p which is a considerable premium to the current price.

During the year a number of changes were made to the board. Jonathan Holmes moved from CEO to Commercial Director and Tony Walters moved from Finance Director to CEO. In addition, John Moy joined as a non-executive director. He is a significant investor in the group and he replaced Richard Darch who stepped down due to his increasing executive commitments with Capita Health Partners.

Going forward, the board see challenges ahead but the “general direction of travel” is apparently positive as the group gear themselves up to deliver the pipeline schemes to financial close. They remain in the early stages of their recovery but there is confidence that they can deliver sustained growth for the business and they expect to post a profit in the next year.

The group made a loss this year so looking at the current PE would be pointless but based on next year’s consensus forecast, the shares trade on a forward PE of 5.1 which seems very cheap. There are no dividends paid here. At the year-end, net debt stood at £2M, a growth of £476K over the end of last year.

Overall then, this has been a very difficult year for the group. The loss worsened, even when the impairment is excluded; net assets are down and the group is close to having a negative tangible book value and the operating cash flow worsened. There is some evidence that the worst could be over, however, the pipeline looks much better and the funding agreement with Funding Affordable Homes looks like a very important step. The health sectors looks like it will continue to be difficult for some time but there are opportunities in the Extra Care sector catering for elderly people and those with disabilities.

It is a concern that one client makes up more than half of revenues and the big impairment does not bode well for the future of those joint ventures and additionally, the change in leadership could add extra uncertainty. The options are interesting though and heavily incentivise the board to increase the share price (although I suppose they do act as a cap on the share price) and with a forward PE of just 5.1 these shares could be worth a gamble?