Poundland is the largest single price value general merchandise retailer in Europe with a network of 588 stores across the UK and Ireland with a further five stores in Spain. Stores are typically in areas with high footfall across a mixture of high streets, shopping centres and retail parks and are all operated on a leasehold basis. They have an office in Hong Kong in order to supply products and an exclusive sourcing arrangement in India.

It has now released its final results for the year ended 2015.

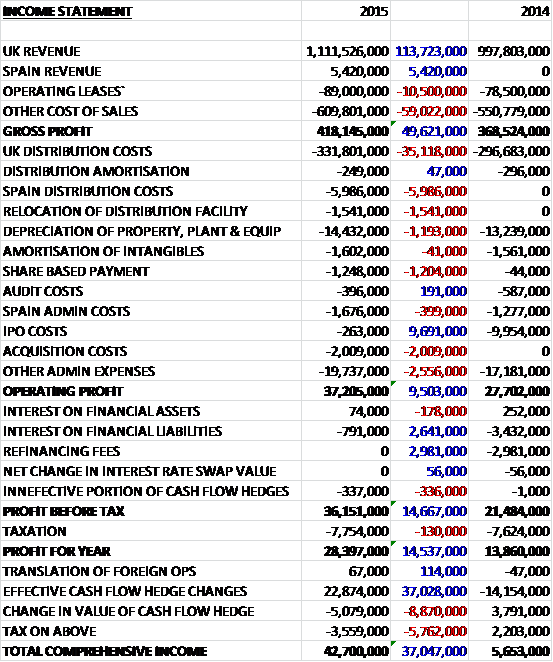

Revenues increased when compared to last year with a £113.7M growth in UK revenue due to both an increase in like for like sales and store openings, and a £5.4M increase in Spanish revenue. Operating lease costs grew by £10.5M and other cost of sales increased by £59M to give a gross profit some £49.6M higher than in 2014. Distribution costs grew by £35.1M and there were a number of “non-underlying items” with a £6M increase in Spanish distribution costs, a £1.5M charge relating to the relocation of a distribution facility, a £1.2M growth in depreciation, a £1.2M increase in share based payments, a £2M acquisition costs relating to the proposed 99p store acquisition and a £2.6M growth in other admin expenses, offset by a £9.7M reduction in IPO costs. Finance costs reduced due to a £2.6M reduction in interest and the lack of £3M of financing fees that occurred last year. Tax was slightly higher to give a profit for the year of £28.4M, an increase of £14.5M year on year.

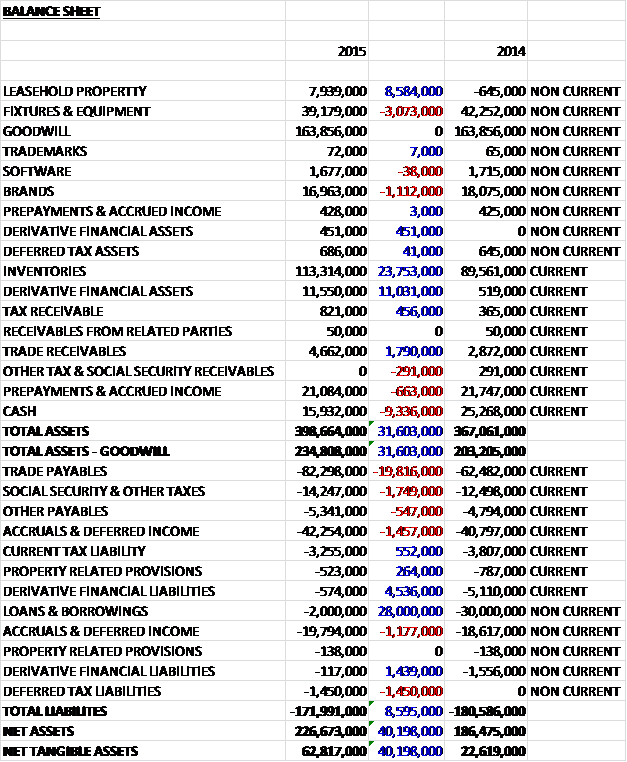

Total assets increased by £31.6M when compared to the end of point of last year driven by a £23.8M growth in inventories, an £11M increase in derivative financial assets, an £8.6M growth in leasehold property due to the transfer of some items from fixtures and equipment (I can’t fathom how there was a negative number last year!), and a £1.8M increase in trade receivables partially offset by a £3.1M fall in fixtures and equipment, and a £1.1M decline in the value of brands. Conversely, total liabilities fell during the year as a £28M fall in loans and borrowings and a £6M decline in derivative financial liabilities was partially offset by a £19.8M growth in trade receivables, a £2.6M increase in accruals and deferred income, a £1.8M growth in other tax payables and a £1.5M increase in deferred tax liabilities. The end result is a net tangible asset level of £62.8M, a growth of £40.2M year on year.

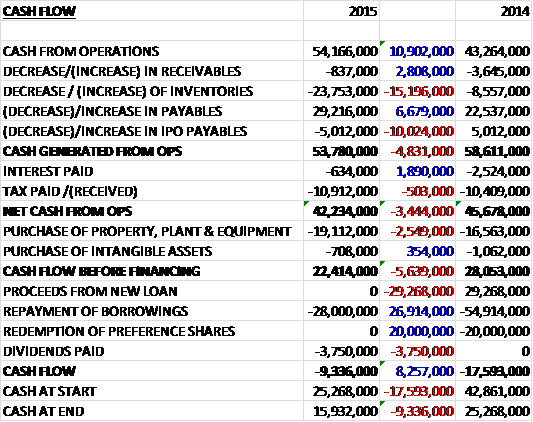

Before movements in working capital, cash profits increased by £10.9M to £54.2M. The working capital was broadly neutral but due to a much larger growth in inventories than last year, partially offset by a lower interest payment, the net cash from operations came in at £42.2M, a decline of £3.4M year on year. The group then spent £19.1M on tangible assets, primarily relating to the opening of new stores, and £708K on intangibles to give a free cash flow of £22.4M. Some £3.8M was spent on dividends with the rest being used to pay back borrowings and the cash outflow for the year was £9.3M and the cash level at the end of the year was £15.9M.

During the year the group grew their like for like sales by 2.4%, ahead of expectations. It should also be noted that in the first half of the year was an exceptional period which benefited from a late Easter, fewer competitor openings and the one-off loom bands craze. The board are therefore expecting the first half of the new year to be relatively subdued, not helped by currency headwinds (if the current weakness in the Euro continues there will be a detrimental effect of £4M on EBITDA), but the second half of the year should benefit from softer sales comparisons, a strong first half store opening programme and the contribution of this year’s late store openings.

This year the group had a number of non-underlying expenses. They are calling their “strategic initiatives” non-underlying which includes the Spanish stores and this accounted for expenses of £2.2M. The group also incurred £1.5M of costs relating to the distribution facility in the SE of England, together with the costs to dispose of the existing temporary facility. They are also counting the amortisation of the Poundland brand as non-underlying, this accounted for £1.1M, and finally the group incurred further fees relating to its listing of £263K and £2M relating to the proposed acquisition of 99p stores.

The Harlow distribution centre is a purpose built 350,000 square foot facility opened in August replacing the temporary facility in Hoddeston. Harlow will now serve as the main depot for SE England and will also provide initial support to the business as they trial the Dealz stores in Spain. The combined distribution centres have increased distribution capacity so that the group is now able to operate about 750 stores. They are currently working on a new distribution centre in the NW of England which is scheduled to open in 2017.

The group is able to generate pay backs from their new stores in around a year so they will continue to add to their store base. They believe that there is potential for more than a thousand Poundland stores in the UK with a potential for a further 70 Dealz stores in Ireland. They therefore plan to continue opening stores at similar rates as in the last four years, adding about 60 net new stores per year, of which about 10% are expected to be in Ireland.

In Spain, the group expect to open up to ten new stores over a two year period, which will initially be supported from the UK distribution centres. The Spanish operations are staffed by a core local team with extensive Spanish retail experience and are supported by a UK-based senior management team. The pilot store’s performance is being assessed ahead of any further roll out in Spain or elsewhere in continental Europe. The customer response has been positive and sales in line with plan. Whilst the board are confident they will succeed in Spain, there is still work to do in developing the economic model. For example, they need to improve the proportion of general merchandise within their mix and they need to increase the local product range. Currently, local sourcing accounts for 20% of sales and Spanish suppliers are increasingly working in partnership with the group.

The group are exploring some other new growth opportunities such as the potential development of a transactional website to access new customers as well as developing new store formats such as a city centre format which is a smaller store designed to operate in high footfall city centre locations with a focus on impulse and convenience purchases.

During the year the group agreed to purchase 99p stores for £55M conditional on Competition and Markets Authority permission. They are now working with them in a Phase 2 review of the acquisition and they are hopeful that they can proceed. If they are successful in the acquisition, they will add over 250 new stores to their portfolio.

During the year the group entered into a new banking facility consisting of a revolving credit and working capital facility of £55M, of which £30M was drawn down to repay the existing long term debt. At the end point of the year the group had a net cash position of £13.9M compared to a net debt position of £4.7M at the end of last year. It is worth noting, however, that the group, in line with many retailers, has a huge operating lease liability off the balance sheet with some £92.6M due within a year and some £645M in total. The group also have outstanding capital commitments of £3.3M at the year-end.

The group has a significant transaction exposure with increasing, direct sourced purchases from its suppliers in the Far East, with most of the trade being in US dollars. In addition to this they are exposed to transaction risk on the translation of surplus Euro balances generated by the Irish business, and to a lesser extent the Spanish trial, into Sterling. The policy allows these exposures to be hedged for up to a year and a half forward in order to fix the cost in Sterling.

At the current share price the shares trade on a PE ratio of 13.1 but this increases to 16.7 on next year’s consensus forecast which seems a little steep. After the group paid out its first dividends, the shares are now yielding 3% which increases to 3.3% on next year’s forecast.

Overall then this has been a fairly good year for the group. Profits were up, as were net tangible assets and although operating cash flow was down, this was due to an investment in inventories and cash profits grew. Like for like sales were up but the board point out that this was due to an exceptionally strong H1 which is unlikely to be repeated in the coming year.

I have to say kudos to management for pointing this out as so many times in some other companies they fail to mention this. Having said that, I do think the accounting for non-underlying items is a bit aggressive. The opening of the new distribution centre should help growth, and the company is definitely in an expansion phase with large numbers of new stores opening but they will have to keep an eye out for costs, particularly the bulging operating lease commitments going forward.

With a forward PE of 16.7 and dividend yield of 3.3% these shares are no exactly cheap and when we add on the operating lease commitments to debt, there is a bit net debt figure here and I feel this is a bit risky for me. Unless things change, I will not be covering Poundland going forward.