Cohort provides a wide range of services and products for UK and international customers in defence and related markets. There are four main businesses. MASS is a specialist defence and technology business, focused mainly on electronic warfare, information systems and cyber security. MCL is an expert in the sourcing, design and integration of communications and surveillance technology, as well as support and training for UK end users including the MOD and other government agencies. SCS is a defence and security consultancy, combining technical expertise with armed forces experience and domain knowledge. SEA is an advanced electronic systems and software house operating in the defence, transport and offshore energy markets.

Following the acquisition and integration of J&S, the SEA business has been restructured into four market facing divisions which comprise the Maritime Division, including design, development, production and support of its naval communication systems, sonar, torpedo launch and other naval systems; the Research and Technical Support Division, including its capabilities in the land and research markets of defence; the Software division, including the transport work as well as other civil and non-maritime products, its training and simulation capabilities and other information systems; and the Subsea Engineering division, developing and delivering the business’ activities in the offshore energy market. The four divisions will be supported by a single production facility at its Barnstaple site following the integration of the former SEA and J&S facilities at Beckington, Bristol and Barnstaple into one.

It has now released its final results for the year ended 2015.

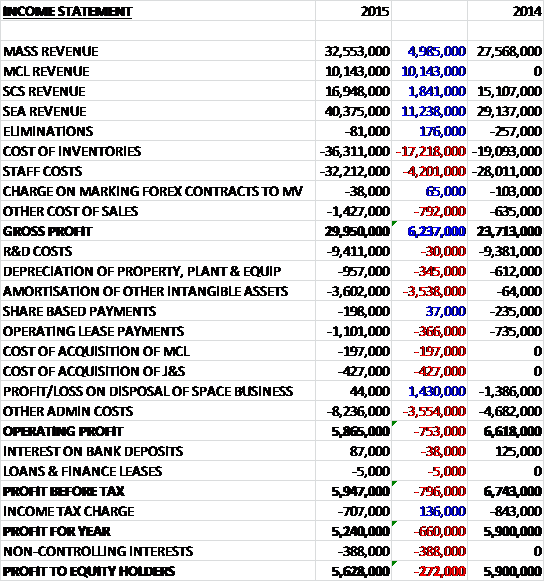

Revenues increased across all business segments when compared to 2014 with an £11.2M growth in SEA revenue, a £5M increase in MASS revenue, a £1.8M growth in SCS revenue and a maiden contribution of £10.1M from the MCL business. Cost of inventories grew by £17.2M, staff costs were up £4.2M and other cost of sales increased modestly but the gross profit was still £6.2M ahead of the prior year. The amortisation of intangibles grew by £3.6M year on year and other admin costs were up £3.6M, although there was no loss from the disposal of the space business that occurred last year which accounted for £1.4M, which meant that the operating profit was £753K lower than in 2014. A small reduction in interest received was offset by a lower tax payment and after the loss attributable to non-controlling interests is taken into account, the profit for the year comes in at £5.6M, a decline of £272K year on year.

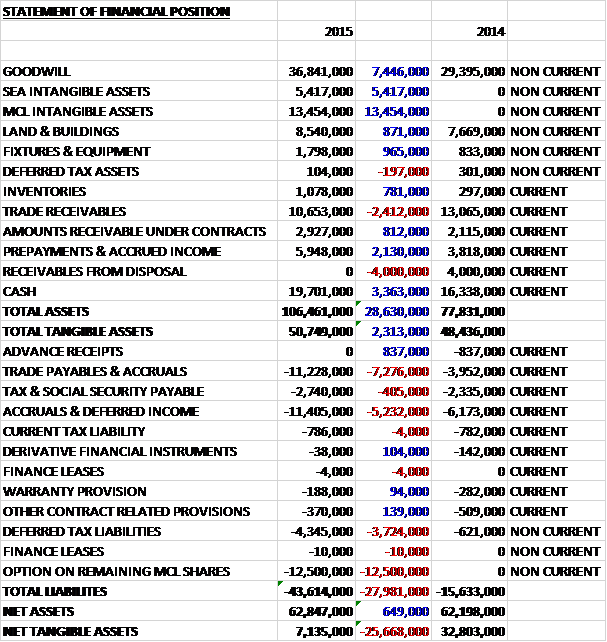

When compared to the end point of last year, total assets increased by £2.3M to £50.7M driven by an £18.9M growth in intangible assets, a £7.4M increase in goodwill, a £3.4M increase in cash and a £2.1M growth in prepayments and accrued income, partially offset by a £4M reduction of receivables following the disposal and a £2.4M fall in trade receivables. Total liabilities also increased during the year due to a £12.5M option on the remaining MCL shares that were not acquired, a £7.3M growth in trade payables, a £5.2M increase in accruals & deferred income and a £3.7M growth in deferred tax liabilities due the addition of intangible assets from the acquisitions. The end result is a net tangible asset level of £7.1M, a collapse of £25.7M year on year.

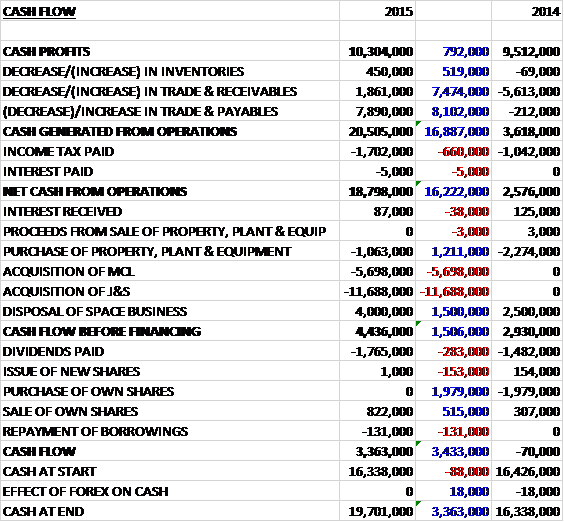

Before movements in working capital, cash profits increased by £792K to £10.3M. There was a big cash inflow from working capital, however, with a particularly large growth in payables due to supplier invoice slippage from the year-end into Q1 and after tax increased by £660K, the net cash generated from operations still came in at £18.8M, an increase of £16.2M year on year although given the reasons for the reduction in working capital this year, the operating cash conversion will be much weaker in 2016. The group then spent £1.1M on capex and a net £13.4M on acquisitions and still managed a cash inflow of £4.4M before financing. Of this, £1.8M was spent on dividends to give a cash flow for the year of £3.4M and a cash level at the year-end of £19.7M which is impressive given the acquisitions.

The adjusted operating profit in the MASS division was £5.5M, a growth of £500K year on year. A significant contributor to the increase in revenue was export EW operational support with extensions to its existing services in the Middle East taking its current workload through to the end of the 2016 calendar year. Educational deliveries were flat during the year but the business has continued to invest in its wider cyber offering for new commercial and government customers, the latter providing the first significant order wins and deliveries towards the end of the year.

The mix of work and the investment in cyber capability resulted in the division’s net margin being lower than last year, falling from 18.1% to 16.9% which is nearer to their long term expectations for the business as it grows its cyber offering which includes more brought in equipment. There is a portfolio of work including long-term managed service offerings, higher margin but unpredictable export business and more predictable but lower margin secure network and cyber activity in education, commercial, security and defence markets.

The division’s support contract for the NATO joint EW Core Staff, secured in 2014, was extended for a further year which provides MASS with further opportunities to access NATO customers as well as providing a growing work stream in its own right. The business enters the current year with a strong order book, increasing from £46.M this time last year to £53.4M, and pipeline of opportunities including exports.

The adjusted operating profit in the MCL division was £1.3M which represents ten months of contribution from the division and was close to expectations with a net margin of 13.1%. This performance was driven by the delivery of electronic surveillance systems to the UK Royal Navy, tactical satellite communication upgrades for British Army vehicles returning from Afghanistan and a number of other EW and communication deliveries for UK forces.

During the year the business designed, built and tested a one-off electronic system for a defence customer in under six months, a requirement driven by a demanding time sensitive mission, and a project that is likely to lead to the possibility of further orders. The business currently has a short order to delivery timescale, resulting in a relatively low current order backlog at any time and it ended the year with just under £3M on contract. The pipeline includes prospects for securing long-term, larger orders which if won, would help to build a higher and more predictable base load of work.

The adjusted operating profit in the SCS division was £1.3M, an increase of £300K year on year. This improvement reflects a continued focus on growing areas of the MOD budget, in particular domain hazard analysis and technical assurance which have grown as new military air platforms have been introduced into UK service. The business has also grown its NATO work and other export offerings. A further positive sign for the business was the improvement in its high level training offering to the UK’s joint Warfare Centre, a service they have been providing for over ten years and which was extended for a further year until March 2016 following an exercise of an option by the customer. The increased activity was a result of the UK’s return to normal patterns of deployment and training following the exit from Afghanistan and they also continued to secure further overseas work for this offering. The order book at the year-end was £9.8M compared to £10M at the end of last year.

The adjusted operating profit in the SEA division was £4M which includes seven months of contribution from the acquired J&S business but no contribution from the sold Space business, and represents an increase of £200K when compared to last year. The continuing business saw adjusted operating profit grow by 28% and revenues increase by 32%. The growth in revenue was due primarily to the securing of an initial common EXS contract which extends the ECS system to cover two additional Astute class boats to bring the number under contract up to seven, the four Vanguard class boats and certain of the Trafalgar class vessels.

This increase offsets a deterioration in the transport revenue where an export contract delivered last year was not repeated. In net margin terms, the effect of these changes was a small reduction on a like for like basis from 13% to 12.6%. The business continued to make good progress on its External Communications System for the Astute class of submarines, with the first boat carrying the system having now gone to sea.

The defence research revenue was slightly up on last year. The business has continued to deliver a major research programme on soldier equipment known as Delivering Dismounted Effect to its customer, the Defence Science and Technical Lab. In the transport market, the business maintained deliveries of Roadflow units to UK customers. They made good progress on their red light enforcement system, which is derived from Roadflow, obtaining the necessary technical clearance for the system. They now have to wait for formal sign-off by the Home Office to enable the system to be fully deployed, with its output admissible as evidence in future prosecutions.

The division had a very strong operating cash flow in the year with good receipt management in the final quarter and slower than expected invoicing from its suppliers which caught up in the first few months of 2016.

The acquired business of J&S contributed just £100K of adjusted operating profit on revenues of £7.9M. This was below the board’s expectations and was as a result of delayed orders for naval support and its low profile array sonar. These orders have now been secured and delivery has commenced so they now expect J&S to deliver a return next year in line with expectations at the time of the acquisition.

The offshore energy business was acquired just at the end of its peak activity period in the summer but despite the depressed oil price it has secured its largest ever contract for a subsea distribution unit from Apache for over £1M. The integration of J&S has progressed well and was mostly complete by the end of the year. The division incurred £200K of integration costs in the year and this is expected to realise annual savings of around £500K so a great return there. The division’s closing order book of £68M underpins next year’s revenue nicely, especially in the submarine and other naval system work.

Order intake for the year was £114.3M compared to £68.5M last year and a further £5.4M and £32.6M of orders were added to the order book with the acquisitions of MCL and J&S respectively.

There are a number of interesting projects completed by the group during the year. SEA is delivering torpedo launch systems to the Malaysian Navy for deployment on a fleet of offshore patrol vessels; SCS provides the communication and information system to the EU’s counter-piracy operation; MASS provides the UK’s electronic warfare database based on THURBON; MCL provides tactical Nano UAV systems for front line operations; SCS has renewed its contract to provide training and exercise support to the UK’s Joint Forces Command; SCS provides expert non-lethal weapons technology advice to DSTL; SEA is leading research into the future British infantryman through its framework for the DSTL; and SCS provides independent technical analysis for air platforms entering UK service, including JSF and Air Seeker.

It is worth noting that the group is heavily reliant on a small number of clients. The UK MOD is the largest and accounts for 38% of revenue and another large client accounted for 22% of revenues this year and the MOD is probably more important even than this as many other orders were ultimately sourced from the MOD but received via other contractors. With the Government running a significant budget deficit there is a risk that further controls in defence expenditure could be introduced and given how reliant the group are on the MOD as a customer, this is probably the key risk facing the company in my view. Another operating risk is the short visibility on revenues in the SCS and MCL businesses due to the short typical contract duration in these divisions.

There were a couple of acquisitions during the year. In July the group acquired 50% of Marlborough Communications for a total consideration of £8.8M satisfied entirely by cash, generating goodwill of £2.4M with other intangible assets of £7.8M. In the ten months following the acquisition, the business generated adjusted operating profit of £1.3M. There is an option for the purchase of the remaining 50% of the business which is exercisable by the end December 2016 and capped at £12.5M.

In October the group acquired J&S ltd for a cash consideration of £11.7M. The acquisition came with intangible assets of £6.8M and generated goodwill of £5M. In the seven months since acquisition the business generated just £100K to adjusted operating profit. At the end of April the group sold its space business to Thales for a consideration of £5M in cash. Going forward, the group have stated that they will look to make at least one acquisition in 2016 and are putting in place enlarged bank facilities to support their growth, which is expected to be about £25M.

The closing order book at the year-end was £134M compared to £81.7M at the end of last year which underpins the revenues for the coming year, although the UK defence market remains tight. Export prospects continue to strengthen and outside of defence, MASS is making progress with its cyber capability, especially in the security market, and in transport the level crossing enforcement system has completed all of the testing required to enable it to achieve UK Home Office approval. A number of long term orders were secured during the year so the board do not expect to see a repeat of this year’s sharp increase in the order book over the coming year. Overall the board considers that their order book and near-term prospects provide a good base for future progress.

At the year-end the group has a net cash position of £19.7M compared to £16.3M at the end of last year. At the current share price the shares trade on a PE ratio of 24.6, falling to 16.9 on next year’s consensus forecast. After a 19% increase in the total dividend, at the current share price the shares have a dividend yield of 1.5% increasing to 1.8% on next year’s forecast.

Overall then, this has been a decent year for the group marked by some large acquisitions. Profits were down but this was due to the effect of the acquisitions with a large growth in the amortisation of acquired intangibles. Net tangible assets fell considerably as a large amount of intangible assets were acquired with the businesses. Operating cash flow increased and generated plenty of free cash, although this was mainly due to the fact that payables increased substantially, although cash profits also saw a modest increase.

There was growth in most of the businesses with decent levels of order books – the orders for NATO sound interesting and could be a foot in the door for a big customer base. The acquired J&S business is not contributing as well as expected, however, due to some delayed naval orders which have subsequently been received. The focus on offshore energy is also a concern given the current state of the oil and gas industry, although a large order has been received there. In summery this is a nice business in my view but given the risks surrounding the new acquisitions, I think the forward PE of 16.9 is a little strong and the dividend yield of 1.8% doesn’t really offer enough reward to cover the risk. It is an interesting company, though, and one I will keep a close eye on.