Cohort has now released its interim results for the year ending 2016.

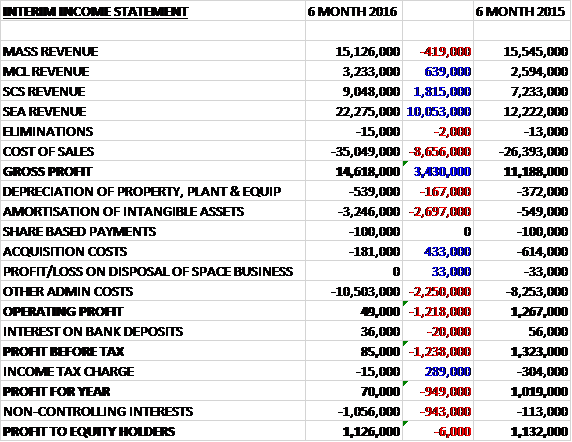

Revenues increased considerably when compared to the first half of last year as a £419K decline in MASS revenue was more than offset by a £10.1M growth in SEA revenue, a £1.8M increase in SCS revenue and a £639K growth in MCL revenue. After an increase in cost of sales, the gross profit was £3.4M higher than in the first half of 2015. Depreciation increased by £167K and amortisation grew by £2.7M but acquisition costs were £433K lower than last time. After a £2.3M growth in other admin costs the operating profit was down by £1.2M. Interest income was slightly lower but this was more than offset by a £289K reduction in tax charges and once the £943K growth in the loss attributable to non-controlling interests was taken into account, the profit for the half year was £1.1M, broadly flat year on year.

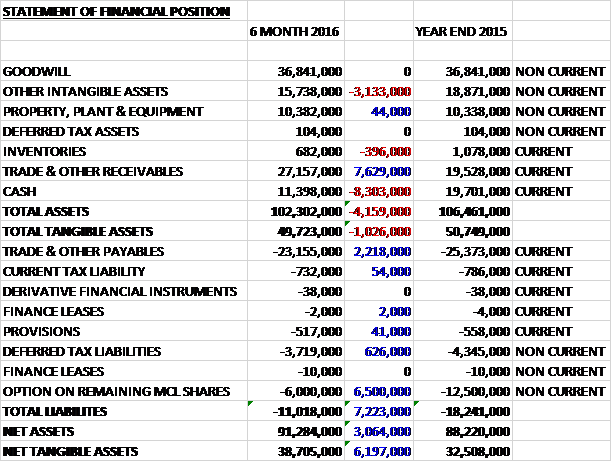

When compared to the end point of last year, total assets fell by £4.2M, driven by an £8.3M decline in cash and a £3.1M decrease in intangible assets, partially offset by a £7.6M growth in receivables. Total liabilities also declined due to a £6.5M reduction in the option on the remaining MCL shares, a £2.2M fall in payables and a £626K decrease in deferred tax liabilities. The end result is a net tangible asset level of £38.7M, a growth of £6.2M over the past six months, entirely attributable to the decline in the value of the option on MCL shares.

Before movements in working capital, cash profits increased by £1.1M to £3.9M. There was a big cash outflow in working capital, mainly due to a large growth in receivables which meant that after tax the net cash outflow from operations came in at £5.6M, a detrimental movement of £11.1M year on year. The group then spent £584K on capex and £670K so far on the EID acquisition which meant that before financing, there was a cash outflow of £6.8M. We then see £1.4M paid out in dividends and a mall net purchase of shares to give a cash outflow of £8.3M for the period and a cash position of £11.4M at the end of the half.

Order intake for the first half was £55.7M, down from £64.5M last year excluding the acquired order books of MCL and J&S which, when added to the total, resulted in a closing order book of £140M compared to £134M at the year-end. As expected the order intake was lower than last year which included a large order to extend SEA’s External Communications Systems to the whole UK submarine fleet. Further orders in respect of ECS are expected in the second half of the year.

The operating profit in the MASS division was £2.4M, a growth of £458K when compared to the first half of last year on a slightly lower level of revenue. The improved performance arose from increased revenue from higher margin electronic warfare support contracts, including the recently announced contract win in the Middle East and the operating margin of 15.7% is below what they expect to see for the full year. The division had a closing order book of £52.4M, of which £15M is deliverable in the second half of the year and this, along with some good opportunities, give the board confidence that the business will have a stronger second half.

The operating profit in the MCL business was just £19K, a decline of £145K year on year. This performance was a result of slower order intake but the recent hearing protection order for £11.2M, together with other programmes for which the company is bidding, will help give better forward visibility in future and this, combined with the £13.9M closing order book, of which £7.2M is deliverable in the second half and the fact the MOD’s order patterns are usually stronger in the second half, give the board confidence that the business will deliver a stronger second half.

The operating profit in the SCS division was £303K, broadly flat year on year with a fall of £5K on revenues that increased by nearly £2M which meant that net margin fell from 4.3% to 3.3%. This decline reflects a weaker mix, with higher levels of Air Systems work and less overseas support work as a result of the withdrawal from Afghanistan. The recently announced contract win to continue to provide support in the UK’s Joint Warfare Centre supports a closing order book of £17.7M, of which £7.2M is deliverable in the second half and again the board believe the business will perform strongly in the second half.

The operating profit in the SEA division was £1.8M, an increase of £691K when compared to the first half of 2015 as the integration of J&S continued. The increase in profit was achieved on higher revenues and the net margin of 7.9% was below the 8.8% achieved last year, a reflection of a mix of slightly lower margin work and a tough market for the offshore energy business. The closing order book of £56.1M included £19M of revenue to be delivered in the second half of the year and this, together with a pipeline of good opportunities and the expectation of the usual stronger second half gives the board confidence that this division, too, will make further progress in the second half as well as returning to a more usual operating margin.

Some £48.4M of the period-end order book is deliverable in the second half of the year and represents 90% of the consensus forecast revenue for the year.

In August the group announced it had agreed to acquire EID, a Portugal based supplier of advanced electronics, communications and command and control products and systems for the global defence market. At the same time they paid £670K, representing 5% of the total gross consideration of £13.3M. The total expected costs of the acquisition are estimated at £650K. Initially the group had expected to complete the acquisition by December but due to the political situation in Portugal following the general election, the completion has taken much longer than expected to resolve with a government with parliamentary support only sworn in towards the end of November.

With other urgent priorities for the new government, political approval of the transaction is likely to take some time so the group have agreed to acquire a 57% stake which equals the entire stake of EID’s private shareholders and gives them management control of the business and this is expected to take place before the end of January, though a limited further delay is possible if Portuguese competition clearance is required. This stake is being acquired at a cost of £7.7M, in line with the original acquisition terms. The group have agreed to acquire the Portuguese government’s stake as and when approval is given, provided this is no later than the end of June. This is turning into a bit of a mess actually.

As can be seen, the value of the option for acquiring the non-controlling interest in MCL, from £12.5M to £6M reflects the latest estimate of MCL’s performance for the next two years.

During the period the group concluded its negotiation with its banks and has recently put in place a new £25M revolving credit facility. This will be party utilised to fund the acquisition of EID and provides the group with further acquisition capacity as well as sufficient funding for day to day operations, especially in respect of export opportunities.

Overall, the closing order book of £140M and recent order wins provide a good underpinning to the second half of the year and the board expect, as seen in the last few years, a much stronger performance than in the first half. The Strategic Defence and Security Review recently concluded in the UK gives support to existing programmes, such as submarines, in which the group is engaged and foresees greater expenditure in areas such as Cyber and Special Forces. The board expect EID to deliver a small contribution this year with more significant contributions thereafter.

After a 19% increase in the interim dividend, at the current share price the shares have a dividend yield of 1.6% which increases to 1.8% on next year’s consensus forecast. The net cash position at the period-end was £11.4M compared to £6.7M at this point of last year and £19.7M at the end of 2015, although some £7.7M is still to be paid for the EID acquisition.

Overall then this has been a bit of a mixed half year for the group. Profit was flat year on year, although this does include a bit increase in amortisation charges. Net assets did improve to a more healthy level, however, due to the reduction in the value of the option for the rest of MCL. There was an operating cash outflow compared to an inflow last time due to a growth in receivables. The cash profits did actually increase year on year though.

Operationally, it was a bit of a mixed bag. MASS and SEA performed well on the back of some good Middle East contracts but SCS profits were flat due to lower margin work following the withdrawal from Afghanistan and profits at MCL fell due to a slower order intake – something the board expect to reverse in the second half. The EID acquisitions seems to be getting a bit messy and I am a bit concerned this will be a bit of a distraction and with a dividend yield of 1.8%, I am not sure this fully compensates the potential risk here. I will keep a watch on the shares for now.

On the 10th February the group announced that non-executive director Robert Walmsley had purchased 4,965 shares at a value of £16.5K to give him a total of 30,000 shares in the company.

On the 7th March the group announced that its proposed acquisition of a controlling stake in EID has received approval from the Portuguese competition authority. Their aim to take a majority stake in the business is running into some issues, however, as the new Portuguese government has indicated that it wishes to retain part of its existing holding. Discussions are underway to agree the terms of the relationship between the two future shareholders. This is starting to look a bit messy in my view.

On the 31st March the group announced that it had been awarded a further order by BAE to provide its External Communications System for the second stage of the common External Communications System for the Royal Navy. The value of this order will eventually be worth up to £17M and will cover further procurement and design activities.

The group is already committed to providing the ECS for five new build Astute class subs, having been awarded the initial contract in 2009. In October 2014 they were awarded a further order to commence design work on cECS, exctending ECS to all classes of Royal Navy subs. This second stage order continues cECS design and critical procurement activities into 2017, and further orders are expected in that year. In all, this programme is continuing in line with board expectations.