Ashley House has now released its interim results for the year ending 2016.

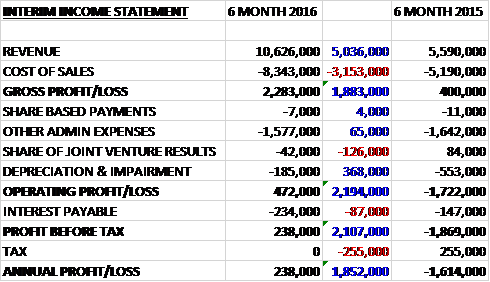

Revenues increased by £5M when compared to the first half of last year and given cost of sales grew by just £3.2M, the gross profit was some £1.9M higher. Admin expenses fell somewhat, and depreciation & impairment declined by £368K but there was a £42K loss from joint ventures as opposed to an £84K profit last time to give an operating profit some £2.2M better than the loss in the first half of 2015. Interest was somewhat higher and there was no tax rebate this time so the profit for the half year period came in at £238K, an improvement of £1.9M year on year.

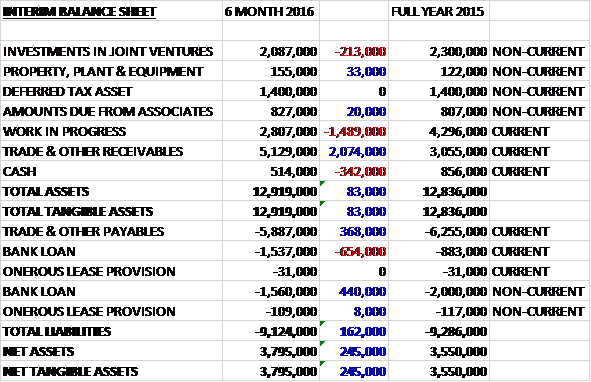

When compared to the end point of last year, total assets were broadly flat, up just £83K as a £2.1M growth in receivables was offset by a £1.5M fall in work in progress, a £342K decrease in cash and a £213K decline in investment in joint ventures. Total liabilities declined during the period, driven by a £368K fall in payables partially offset by a £214K increase in bank loans. The end result is a net asset level of £3.8M, a growth of £245K over the six month period.

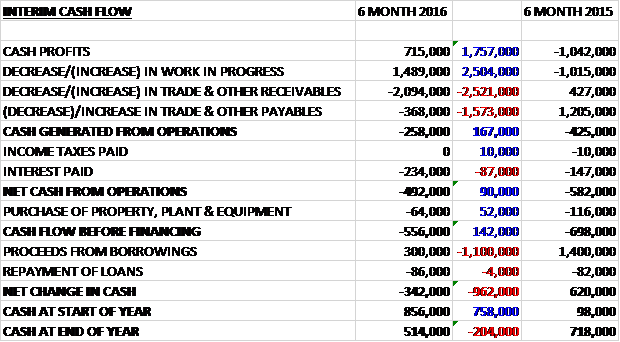

Before movements in working capital, cash profits grew by £1.8M to £715K. There was a cash outflow from working capital, however, as a growth in receivables was not quite offset by a fall in work in progress and after the increased interest was paid, the net cash outflow from operations was £492K, an improvement of £90K year on year. The group then spent £64K on capex and took out a net £214K of new borrowings which meant that the cash outflow for the period was £342K and the cash position at the end of the half was £514K.

In June the group opened their Extra Care development in Grimsby, marking their entry into this market. This was followed at the end of September by the signing of an agreement with the new Extra Care funding partner, Funding Affordable Homes and just before Christmas they reached financial close and had drawn down on the first part of the funding for the next two Extra Care schemes in Harwich and Walton on the Naze.

In the autumn statement the chancellor announced that housing benefit for social housing tenants would be limited to the local housing allowance rate from April 2018 for new or renewed tenancies taken out from April 2016. The Department for Work and Pensions is still working on how the policy will be implemented and whether Extra Care and similar schemes would remain exempted from such measures. Extra Care accommodation is much needed, and the group expect it to be exempted – there is an announcement expected in March.

The Health business continues, albeit at a slow pace. The group will shortly compete a GP centre in Danbury, Essex and are ready to commence on site with a further two schemes. The partnership with Integrated Pathology Partnerships is performing well where they have recently completed a pathology lab in Basildon and are about to commence on a lab refurbishment in Southend whilst pursuing further opportunities.

In Extra care there are two schemes on site (Harwich and Walton on the Naze) with total scheme values of £8.8M and there are also two schemes on site in the Health division with total scheme values of £1.5M. In Health there are also 11 schemes appointed with a value of £27.2M and in Extra care there are a further 17 schemes appointed with a value of £149.2M.

In December the group “novated” the non-core operations management element of the LIFT investment which is a service very different from the rest of the business. This has allowed the LIFT activities to be focussed on development activity. They remain committed to their LIFT joint ventures and are working with the partners to explore opportunities to provide further services within this framework.

The board are confident that the company will be profitable for the full year subject to the timing risk on the next Extra Care developments which is affected by the confirmation of government policy. At the end of the period the group had a net debt position of £2.6M compared to £2.2M at the same point of last year.

Overall then this was a comparatively decent half year period for the group. Profits were up, and a big improvement on the loss recorded in the first half of last year. Net assets also increased but we see a fall in work in progress as schemes progressed through to completion and were not replaced to the same level. The operating cash outflow improved from last year and the outflow was entirely due to working capital movements, with a cash profit evidenced (an improvement on last time too). They drew down the first funding from their FAH agreement to fund the next two Extra Cara schemes and this is very much the future for the group and a very positive move. Progress at the Health business remained slow, however.

The group has a very large pipeline of work but this has always been the case and the issue has been on progressing that pipeline in a timely manner. The funding agreement with FAH definitely helps in this regard but unfortunately another spanner has been thrown into the works with the proposed limits to housing benefit for social housing tenants. The board think that their Extra Care schemes will be exempted but until this is confirmed, this seems like a bit of a punt. I think at these price levels the company does look like an interesting value/recovery play but I would really like some more concrete evidence over government policy going forward before I take the plunge I think.

On the 1st March, Chairman Chris Lyons purchased 50,000 shares at a value of £5K which gives him a total holding of 226,500 shares. Last of the big spenders, huh?