Wynnstay has now released its final results for the year ended 2015.

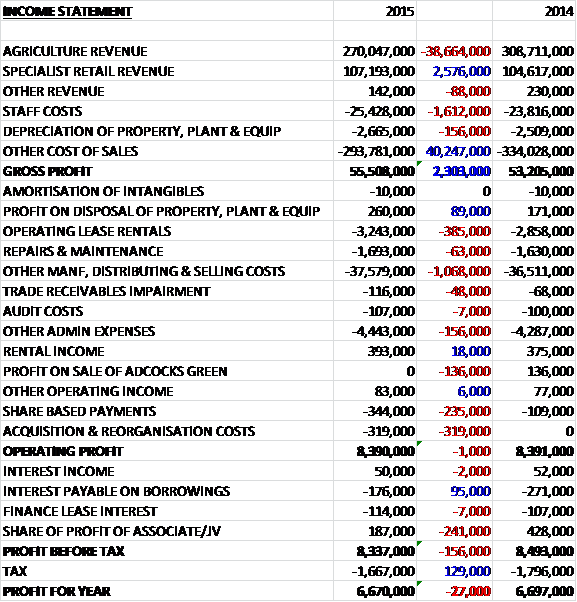

Revenues declined when compared to last year as a £2.6M growth in retail revenue, due to an increase in the number of outlets, was more than offset by a £38.7M decline in agriculture revenue with agricultural price deflation estimated to have accounted for about £32M of the reduction. Staff costs increased by £1.6M and depreciation was up £156K but other cost of sales fell by £40.2M and gross profit was some £2.3M ahead of last year. We then see operating lease rentals increase by £385K and other operating costs grew by £1.1M with admin expenses increasing by £156K. We also see a £235K growth in share based costs and acquisition costs were up by £319K which meant that operating profit was flat when compared to 2014. Interest payable declined by £88K but there was a £241K drop in the share of profits from associates and joint ventures reflecting the challenges of the agricultural market and after a £129K reduction in tax, the profit for the year came in at £6.7M, broadly flat year on year.

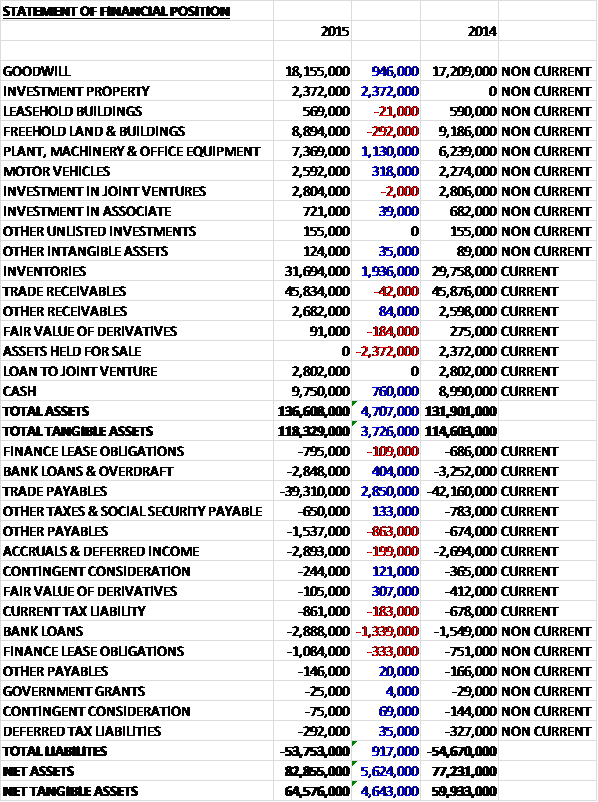

When compared to the end point of last year, total assets grew by £4.7M, driven by a £2.4M investment property, a £1.9M growth in inventories, a £1.1M increase in plant & machinery, and a £946K growth in goodwill, partially offset by a £2.4M elimination of the asset held for sale (perhaps this became the investment property?). Total liabilities declined during the year as a £2.9M fall in trade payables was partially offset by a £1M increase in bank loans and an £863K growth in other payables. The end result is a net tangible asset level of £64.6M, a growth of £4.6M year on year.

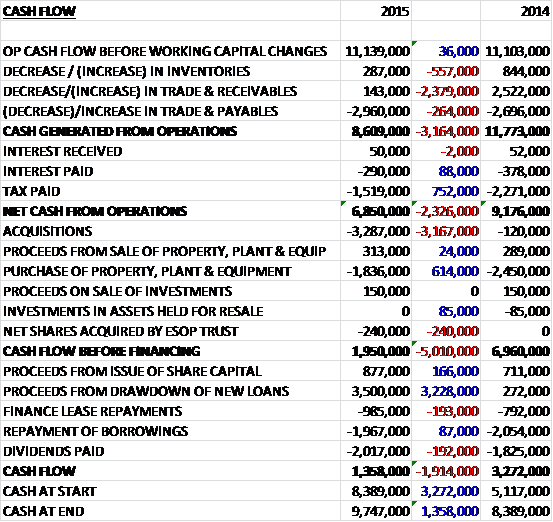

Before movements in working capital, cash profits were broadly flat at £11.1M. There was a cash outflow from working capital, however, with a particularly large fall in payables which meant that after a £752K reduction in tax paid and an £88K fall in interest paid, the net cash from operations came in at £6.9M, a decline of £2.3M year on year. The group spent a net £1.5M on property, plant and equipment and £3.3M on acquisitions to give a cash inflow of £2M before financing. The group then took out a net £1.5M in borrowings that was used to pay dividends of £2M and after finance lease payments of £985K there was a cash flow of £1.4M for the year and a cash level of £9.7M at the year-end.

The Agriculture division generated a profit of £4.1M, a growth of £332K year on year. The performance was helped by strong demand for feed in the first half and an improved raw materials performance. Whilst revenues were impacted by commodity price deflation, decreasing by 13%, the group achieved volume improvement in many product categories and although margins remained under pressure, the focus on operational efficiencies contributed to the improved financial performance.

In Feed Products, total feed volumes increased by 1.5% over the last year, in line with market trends. After a strong first half, demand for feed was more subdued in the second half, reflecting both the prolonged autumn weather and poor milk and meat prices affecting farmers. Slightly lower demand for dairy compound was balanced by an increased demand for blends and feed for poultry, beef and sheep. At Glasson, while overall volumes of raw materials were down year on year, the business generated a good financial contribution, supported by a favourable product mix. Good volumes of fertilizer and specialist products also offset a reduction in unit margins across these categories.

In Arable Product, the group continued to make progress in the sector, although margin pressure remained a feature. Sales of seed products were strong and volumes were in line with last year. Grain yields were good, although with output prices remaining disappointing, farmers have been reluctant to market their grain. The increased yields provided a good opportunity for the grain trading teams at Grainlink and Woodhead seeds, however, and combined volumes increased over the previous year. Demand for fertilizer was subdued in the first half as customers held back from buying in anticipation of a price reduction. The resultant spot market was strong but margins remained under pressure. Autumn demand for fertilizer was tempered by weaker farmer sentiment and the board anticipate a shift in seasonal sales activity to spring 2016.

The Retail division generated a profit of £5.1M, an increase of £207K when compared to last year. At Wynnstay Stores, total sales increased by 3.1% benefiting from the opening of a new store in Aberystwyth in November and the acquisition of Ross Feed at Ross on Wye in January, and S. Jones in September. On a like for like basis, sales showed a reduction of 1%, however, reflecting commodity price deflation. The acquisition of Agricentre was an important one, and provides the group with a trading entry into the West Country, bringing an additional eight units to the group. Its model of small units is wholly geared to farmers and mirrors the approach the group is taking with certain new stores.

At Just for Pets, total like for like sales increased marginally year on year. As expected, though, the profit contribution was lower than last year reflecting the costs associated with expansion. The group opened two new stores, at Cambourne in June and Reading in October, with a further outlet opening in Nottingham after the year-end. An additional outlet is expected to be added in spring 2016. Youngs manufactures and distributes a range of equine products. The business has performed strongly over the year, expanding its position in the market with further opportunities available from continuing growth of the specialist retail division.

The “Other” items generated a loss of £262K compared to a profit of £250K in 2014 as a result of reduced joint venture income mainly from agricultural activities.

During the year the Agricultural Supplies business completed three acquisitions and Glasson Grain completed one acquisition. The Agricultural division completed the purchase of Ross Feed ltd, a supplier of agricultural and hardware goods based in Ross on Wye for £447K, of which £60K was deferred. This acquisition generated £312K of goodwill and the business generated an operating profit of £123K last year. In September, an agricultural merchant based in Llanon was acquired for £143K which generated goodwill of £87K – this business made an operating profit of £40K last year; and in October the group purchased a West Country based Agricentre farm supplies business from T.G. Jeary for £2.7M, generating goodwill of £455K with an operating profit of £377K being generated last year. Finally, in September Glasson Grain completed the purchase of Horti Stores, a supplier of packaging materials to the horticultural and agricultural industries based in Skelmersdale for a consideration of £147K. This acquisition generated goodwill of £92K and the business generated an operating profit of £59K last year.

During the year Lord Carlile retired as non-executive director after spending 16 years at the company. He will be replaced by Steve Ellwood, an agricultural specialist in commercial banking having been head of agriculture at HSBC for ten years.

Going forward, output prices for farmers remain low, with the combination of high levels of world food stocks, tempered demand in developing countries and fluctuating international currencies delaying a return to acceptable pricing. This means that the group’s farmer customers will face ongoing challenges which will require further efficiencies throughout the agricultural industry. In light of continuing low farm gate prices and subdued farmer sentiment, the board’s view of the year ahead has become more cautious. Also, the prolonged mild autumn and late onset of winter has resulted in a slow start to the feed season and a slower start to early trading.

At the year-end the group had a net cash position of £2.1M compared to £2.8M at the end point of last year. At the current share price the shares trade on a PE ratio of 14.9 which falls to 14.1 on next year’s consensus forecast. After an 8.8% increase in the total dividend, the shares now yield 2.2% which grows to 2.3% on next year’s forecast.

Overall then this has been a bit of a subdued performance over the past year. Profits were broadly flat but net assets increased and although operating cash flow fell, this was due to a smaller decrease in receivables than last year and cash profits were flat. Some free cash flow was generated but not quite enough to cover the dividend. The agriculture business saw some improvement due to strong feed demand in H1, which tailed off towards the end of the year, and more cost-cutting. The operating profit in the retail division also increased, but this was due to more Wynnstay stores opening and like for like sales were broadly flat.

Going forward, the board are cautious for the year ahead due to increased pressures on their farmer customers and the slow start to the feed season following the prolonged warm autumn. With a forward PE of 14.1 and dividend yield of 2.3% along with the subdued outlook statement means there is not much to get excited about here in my view.

On the 9th March, Chairman Jim McCarthy purchased 5,000 shares at a value of £24,350. On the same day, non-executive director Philip Kirkham purchased 1,000 shares at a value of just under £5K. This represents both director’s maiden share purchase and is not really a particularly material amount.

On the 22nd March the group released an AGM statement where they informed the market that trading activity in the first four months of the year has been subdued following the downturn across the agriculture sector but has been broadly in line with management expectations.

In the Agricultural division, demand for dairy feed was reduced over the mild winter period but poultry, beef and sheep feed sales have remained in line with previous years. Demand for arable products has gained momentum over recent weeks after a slow start and is now up to the levels of the prior period. Grain trading volumes have increased compared to last year but as expected margins remain under pressure. The Glasson business continues to make a good contribution to the group but is not budgeted to repeat last year’s strong performance.

Trading at Wynnstay Stores has improved after a slow start and an active trading period is anticipated as livestock are turned out in the spring. The integration of Agricentre is progressing well. Like for like sales at Just for Pets were slightly behind those of last year but the roll-out programme is progressing well with new sites identified.

In all, there is nothing here that makes me want to buy the shares just yet.

On the 22nd March the group released an AGM statement where they informed the market that trading activity in the first four months of the year has been subdued following the downturn across the agriculture sector but has been broadly in line with management expectations.

In the Agricultural division, demand for dairy feed was reduced over the mild winter period but poultry, beef and sheep feed sales have remained in line with previous years. Demand for arable products has gained momentum over recent weeks after a slow start and is now up to the levels of the prior period. Grain trading volumes have increased compared to last year but as expected margins remain under pressure. The Glasson business continues to make a good contribution to the group but is not budgeted to repeat last year’s strong performance.

Trading at Wynnstay Stores has improved after a slow start and an active trading period is anticipated as livestock are turned out in the spring. The integration of Agricentre is progressing well. Like for like sales at Just for Pets were slightly behind those of last year but the roll-out programme is progressing well with new sites identified.

In all, there is nothing here that makes me want to buy the shares just yet.