Avingtrans is engaged in the provision of highly engineered components, systems and services and has two main divisions. In the civil aerospace market the group produces pipes for a number of aero engine suppliers into the civil airliner market and they enjoy market leadership in Europe as well as a leading position as an independent supplier in the rest of the world. In addition, they are building a position in assemblies and fabrications beyond pipes such as ducts and nacelles. They also have UK market leadership in the domain of aerospace component polishing and finishing.

In Energy and Medical the group are developing their position as a leading European supplier of energy industry process modules to the power and oil & gas markets. They are also involved in the nuclear decommissioning market as well as a variety of other niches in the renewable energy sector and emerging markets like shale gas. The group manufacture cryogenic vessels in order to supply OEMs in markets such as MRI and the like where they have a global market leading position. Finally, they design and manufacture fabricated poles and cabinets for roadside safety cameras and rail track signalling.

The group has a £219K investment in available for sale assets which is a 7% holding in Vehicle Occupancy ltd which is an unlisted start-up company, but no further detail is given.

It has now released its final results for the year ended 2015.

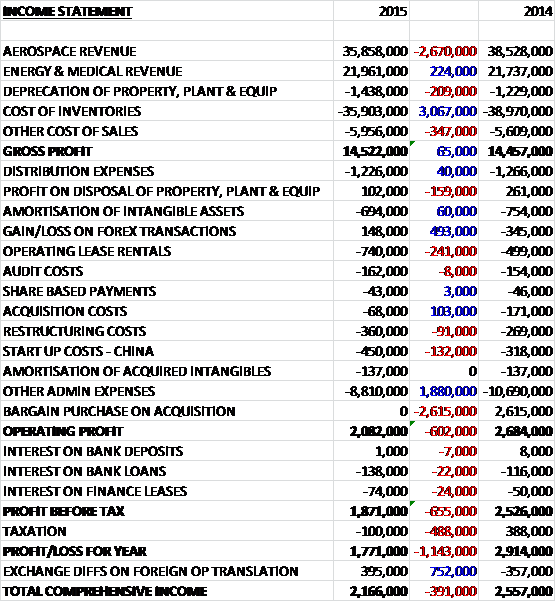

Revenues declined when compared to last year as a £224K growth in Energy and Medical revenue was more than offset by a £2.7M decrease in Aerospace revenue due to customer destocking. Depreciation was up £209K but cost of inventories fell £3.1M with other cost of sales up £347K which meant that the gross profit was broadly flat when compared to 2014. The group had a £493K positive movement in forex transactions but operating lease rentals grew by £241K and Chinese start-up costs increased by £132K before other admin costs declined by £1.9M. After a one-off £2.6M bargain purchase on acquisition last year that was not repeated, the operating profit fell by £602K. The interest on bank loans grew by £22K and the interest on finance leases increased by £24K so that after a £488K detrimental movement in the tax paid/received, the profit for the year came in at £1.8M, a decline of £1.2M.

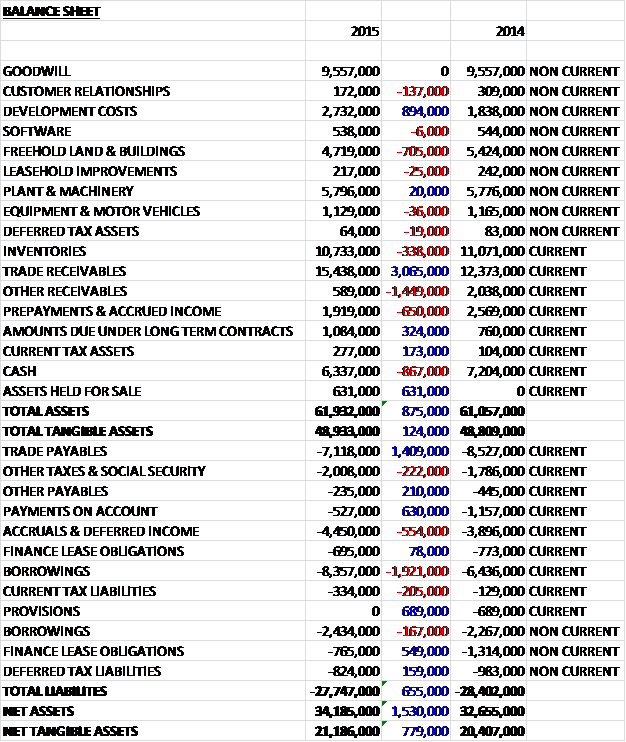

When compared to the end point of last year, total assets increased by £875K driven by a £3.1M growth in trade receivables and an £894K increase in development costs, partially offset by a £1.5M decline in other receivables and an £867K decrease in cash. Total liabilities declined during the year as a £2M growth in borrowings was more than offset by a £1.4M decline in trade payables and a £689K fall in provisions as all sites where dilapidation provisions were held were exited and various legal and other claims by customers were settled. The end result is a net tangible asset level of £21.2M, a growth of £779K year on year.

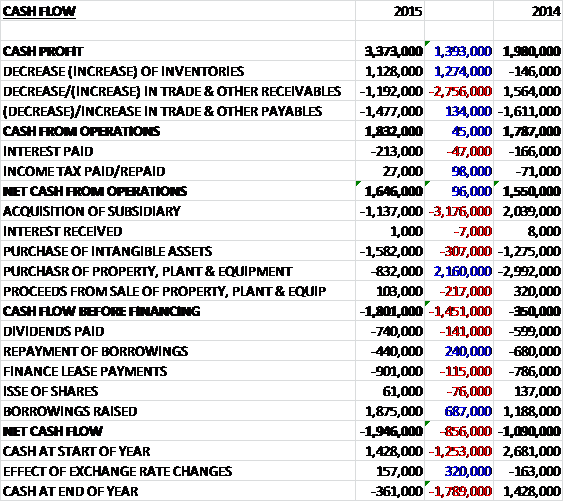

Before movements in working capital, cash profits increased by £1.4M to £3.4M. There was an outflow of cash through working capital, however, with a growth in receivables and a decline in payables to give a net cash from operations of £1.6M, a growth of just £96K year on year. The group spent £1.6M on intangible assets, mostly development costs relating to new customers’ MRI designs and waste storage equipment along with new designs for rigid pipes, light weight fittings and aerospace fabrications, and £832K on property, plant and equipment which doesn’t leave any cash for the £1.1M spent on acquisitions so before financing, there was a cash outflow of £1.8M. The group also spent £901K on finance lease payments and £740K on dividends (that they can’t really afford) and after a net £1.4M of new borrowings, there was a cash outflow of £1.9M and a cash level of -£361K at the year-end.

The civil aerospace market remains robust and between them Boeing and Airbus have a backlog of about 12,000 commercial jet orders and their 20 year demand projections remain at record levels.

The operating profit in the aerospace division was £2.7M, a decline of £1.6M year on year and included a £275K loss from the acquired RMDG business. In the first half of the year the group suffered a material decline in aerospace output due to customer programme volume changes and destocking. While this challenge has now fully abated, it has reduced markedly and they have concentrated on winning new business which has resulted in a £25M ten year contract with PFW (part of Airbus) to produce parts and assemblies for the A350 from the Farnborough facility.

The run rate revenues in the second half returned to the level of the previous period but they were unable to make up for the first half shortfall.

The order book is still strong with the new long term agreement secured with Airbus along with a Sonaca contract worth £5M over five years and these contracts help diversify the customer portfolio to a better balance of airframe and engine applications. As far as the different sites are concerned, Hinckley’s performance was severely impacted by the Q1 destocking events, though matters improved in the second half of the year. During the year the group exited the Derby site and transferred production to Hinckley and Swadlincote and they will conclude the lease arrangement for this site in 2016. The acquired RMDG in Swadlincote had a challenging year and the board have worked hard to stabilise volumes and margins but as expected, the business made a loss of £300K.

The performance at Farnborough continued to improve and the site is consistently profitable. Chengdu’s sales growth was curtailed by the associated Hinckley Q1 sales reduction, though output had stabilised by the year-end. The capacity of the site will be increased in the new year in anticipation of further customer demand and the need to expand pipe production in China. The composites business in Buckingham saw development expenditure and investment which caused losses to increase during the year. The C&H business in Sandiacre had another strong and consistent year with the barrel-type polishing equipment investment paying dividends and the board anticipate further capital expenditure of this sort in 2016.

The operating loss in the energy and medical division was £177K, a £1.1M improvement when compared to last year. The division was boosted by the win of a £47M ten year contract with Sellafield for the precision of three metre cubed boxes for the storage of intermediate level nuclear waste. This contract, together with a parallel contract awarded to another vendor, is the first step in a commercially significant programme by the UK government to repackage the legacy nuclear waste for long term storage and the group considers itself to be well placed to be a key partner for Sellafield in this programme over the next thirty years.

The abrupt reduction in the oil price shattered the recovery at the Maloney business. The prospect bank evaporated as customers delayed or cancelled their investment decisions and this reaction was universal with few projects surviving. The group have therefore downsized the business and exit the Aldridge manufacturing site. The oil price reduction meant that the growth intentions gave way to cost controls but despite the overall loss during the year, there was a modest profit in the second half. The loss included the ongoing start-up costs at the Metalcraft China facility where the build-up of MRI business from Siemens and others has been slower than expected. The Crown business continued to grow and made a profit as transport infrastructure business gradually returned and they worked on a new product for a new customer in the recycling arena.

As far as the individual businesses are concerned, Metalcraft in Chatteris saw steady business with Siemens and Cummins. Site delivery and quality consistency improved and the group began to see initial growth of other repeat customers. Key customer Meggitt saw the downside of the oil price and hence gave the group less business during the year. The site rolled out the Epicor IT systems and this has been bedding in reasonably well over the last few months. The nuclear decommissioning contract win will result in site preparations in 2016 but very little volume of business as the ramp up is quite slow.

At Metalcraft in Chengdu, the start-up losses were higher than in the original plan but they are containable as the business seeks to win business from a broader customer set. At Maloney Metalcraft in Aldridge, the oil price decline killed the prospects of the business. Whilst some restructuring costs have spilled over into the new year, the project to reshape the business is proceeding well and the win of a $3M Samsung Algerian gas field project in the second half shows there is still some new business out there to win.

In August 2014 the group acquired RMDG Aerospace for a cash consideration of £1.1M which is the value of the net assets owned by the business. Since the acquisition date the business had an adverse impact of £395K on operating cash flows. Last year, the group acquired Maloney Metalcraft. This acquisition resulted in a gain of £2.6M as a consequence of buying the business in a distressed state so the “gain on bargain purchase” was listed separately on the income statement.

The group continued to invest on their new composite pipe technology and produced some prototypes for the Paris air show this year and secured further grant funding for composites technology in the period.

The group is reliant on a relatively small number of large customers. The largest one, in the Aerospace division accounts for 22% of total group revenues and a large customer in the energy and medical division accounts for 13% of total group revenues. It is worth noting that the group is spending quite a lot on development at the moment. This year there was £1.4M of development costs compared to amortisation costs of £509K so it could be argued that the profits are over-stated by about £900K. Although the impairment of trade receivables did not show much of an increase this year, the amount of receivables overdue has increased considerably, up from £1.7M last year to £3.8M this year so this is perhaps something that should be watched.

The group is somewhat susceptible to a change in the sterling and US dollar exchange rate with a 10% adverse movement giving rise to a £123K loss. During the year the group appointed Les Thomas as a non-executive director. He is currently CEO of Ithaca Energy.

It is worth noting that the group has tax losses carried forward of about £5.2M that may be offset against future profits. During the year, management decided to relocate the direct production work undertaken by the Aldridge site within the Energy and Medical division to the Chatteris site, making it surplus to requirements. Consequently the freehold site at Aldridge was classified as held for sale. After the year-end, it was sold for £1.1M which resulted in a profit of £500K.

At the end of the year, the group had a net debt position of £5.9M compared to £3.6M at the end of last year. At the current share price, the shares trade on a PE ratio of 19.8 although this falls to 10.2 on next year’s consensus forecast. After an increase in the total dividend, the shares have a yield of 2.2% which increases to 2.6% on next year’s forecast.

Overall then this was a mixed year for the group. Profits declined but this was due to the gain on last year’s acquisition and without this, profits increased – although the above note regarding development costs should be taken into account. Net assets improved, as did the operating cash flow but there was no free cash generated. There were issues in both divisions, with profits in the aerospace division falling due to customer destocking in the first half of the year and while the performance in the energy and medical division did improve, the business is still loss making and oil and gas orders fell off considerably.

Going forward, the Sellafield contract does look interesting but with net debt increasing and an arguably unsustainable dividend of just 2.6% on offer, I will not be investing here yet.