Avingtrans has now released its interim results for the year ending 2016.

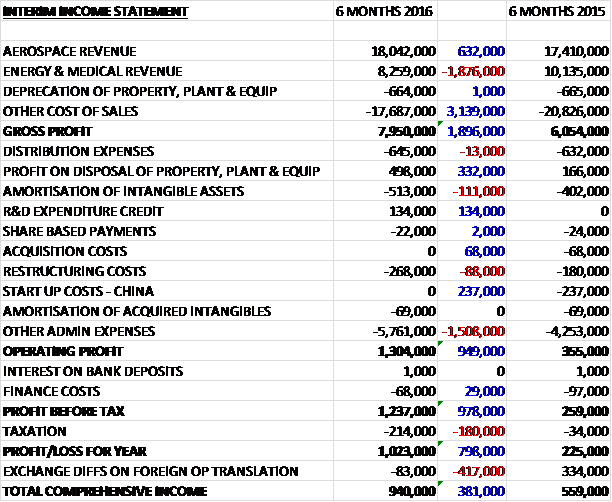

Revenues declined when compared to the first half of last year as a £632K growth in aerospace revenue was more than offset by a £1.9M decrease in energy and medical revenue. Cost of sales also declined, however, so the gross profit increased by £1.9M. Amortisation increased by £111K and restructuring costs were up £88K but this was offset by a £134K R&D expenditure credit, the lack of £68K of acquisition costs and no Chinese start-up costs which were £237K last time along with a £332K increase in the profit on the disposal of property, plant and equipment relating to the sale of the Maloney Aldridge manufacturing site. We then see a £1.5M growth in other admin expenses which gave an operating profit some £949K above that of the first half of 2015. Finance costs declined by £29K but tax was up £180K so that the profit for the half year period came in at £1M, a growth of £798K year on year.

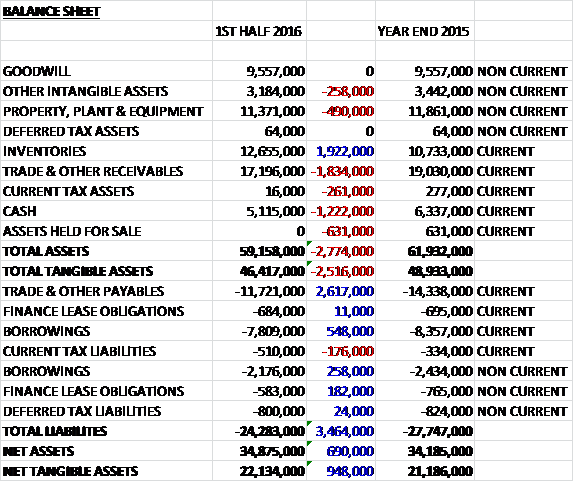

When compared to the end point of last year, total assets declined by £2.8M, driven by a £1.8M fall in receivables, a £1.2M decrease in cash, a decline of £631K-worth of assets held for sale and a £490K decrease in property, plant and equipment, partially offset by a £1.9M growth in inventories. Total liabilities also declined during the year due to a £2.6M fall in payables and an £806K decline in borrowings. The end result is a net tangible asset level of £22.1M, a growth of £948K over the past six months.

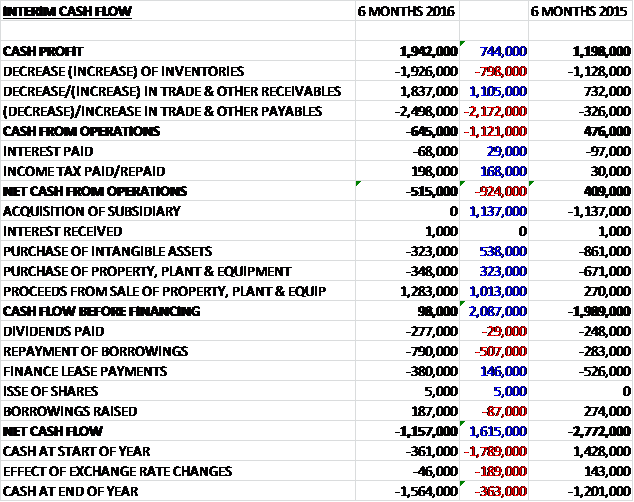

Before movements in working capital, cash profits increased by £744K to £1.9M. There was a cash outflow from working capital, however, with a particularly large fall in payables and even after £198K of cash was repaid to the group, there was a net cash outflow from operations of £515K, a deterioration of £924K year on year. They also spent £323K on intangible assets and £348K on property, plant and equipment but they had an income of £1.3M from the sale of the freehold building which meant that before financing there was actually a small cash inflow of £98K. The group then spent £277K on dividends, £380K on finance leases and a net £603K on the repayment of bank loans so that there was a cash outflow of £1.2M for the first half of the year and a cash level of £1.6M at the period-end.

The operating profit in the aerospace division was £1.9M, a growth of £675K year on year on revenues that increased by just 4% with the majority of the profit growth as a result of the restructuring programme undertaken over the past year. The benefits are still flowing through since the project to exit the Swadlincote site was finished during the period with the results to be seen in the second half.

The restructured division now has four sites. Hinckley is focused on pipe production and some specialist machining and will also become the centre of production for the new composite technology. Farnborough concentrates on fabrications including ducts and special processing of parts. Chengdu in China is the machining centre and also produces high volume pipe assemblies. Sandiacre houses the polishing and finishing business with a small satellite operation in Cheltenham.

Following the acquisition of Rolls Royce’s pipe business after the period end, the board estimate they have a market share of 22% of the addressable aerospace pipe market. As well as potential cost synergies, this new business provides Sigma with an excellent opportunity to rebalance its programme portfolio with the A350 and attendant Trent XWB engines being the best future prospects. The new business has two main sites – Nuneaton specialises in pipe production and is similar to the nearby Hinckley site whilst Xi’an in China specialises in machined parts.

The period saw the first trial orders for lightweight components associated with the group’s composite pipe technology programme. Although volume orders for these parts are still some way off, this is a significant milestone in the development project. During the first half the board also took the decision to transfer the non-aerospace components business to their Energy and Medical division from the second half of the year. In due course as new engine and airframe programmes ramp-up (notably the Trent XWB and the A350 with the Trent XWB being the exclusive engine) the board anticipated that divisional sales will increase to over £50M organically.

The operating loss in the Energy and Medical division was £167K, an improvement of £300K when compared to the first half of last year. The oil price continued to fall in the period but the new business model provides a base which enables the group to adequately cover their costs during this period. The group’s efforts to diversify into new markets and new customers has been rewarded with the business winning two important gas contracts valued at over £2M, with Samsung and Saudi Aramco and other gas prospects are apparently also in sight. Oil-related prospects are still at a low ebb, however which resulted in the decline in revenues.

As well as consolidating their position in the medical imaging market, Metalcraft has been making pre-production preparations for the Sellafield contract which starts in the second half with the layout of the initial production facilities required to manufacture the waste storage containers. Discussions with Sellafield about further opportunities are continuing and the board are optimistic that they will add to this contract in the coming years. The first contract is for 1,100 waste storage containers over ten years, worth £47M in revenue but Sellafield require over 40,000 such containers over the next 20 to 30 years so the board believe that a long term partnership is in prospect. This is potentially transformational for the division over the next few years.

Whilst the development of Metalcraft China has been slow, they have made progress in the period with Siemens and other MRI customers. As turnover is increasing, losses are gradually reducing and after the period-end the business was awarded a three year £3M contract with Bruker, a leader in analytical instrumentation with the products being produced in the UK and China. During the period the business was also awarded a three year £3M contract with Rapiscan, a leader in the global security screening market which is deploying new screening technology in airports around the world.

Prospects for Crown remain encouraging with road and rail infrastructure investments ongoing, although sales here are expected to be second half weighted due to the phasing of various projects. The board have seen promising progress with the FET environment technology where the initial carbon capture trial site is proceeding as expected and further tests are underway to widen the applications of the separation technology.

After the period-end, the group acquired Rolls Royce’s pipe manufacturing assets for £3.5M which gives the group a key future role on the Trent XWB engine. The acquisition of the Rolls Royce Pipe business does mean the group is dependent on one particularly large customer but the division is on track for a full year profit this year as opposed to a small loss last year. The deal is expected to complete in March and is expected to contribute to the results in 2017. Apparently this deal facilitates discussions with Rolls Royce about the supply of pipes for their new Trent XWB engine platform and in the meantime Sigma will produce all the pipes for this engine during the ramp up phase and the group are discussing longer term supply arrangements at present.

With good progression in the aerospace business and results for the energy and medical division expected to be second-half weighted the board remain optimistic about their prospects for the full year and remain confident about achieving their expectations.

The net debt at the end of the period stood at £6.1M compared to £5.9M at the end of last year. After a 10% increase in the interim dividend, the shares are now yielding 2.3% which increases to 2.6% on the full year forecast.

Overall then this has been another mixed period of trading. Profits and net assets did improve but there was a cash outflow at the operating level due to a big reduction in payables – cash profits actually increased – so once again the dividends are not covered by cash earnings. I would much rather the board stopped increasing the dividend and focused on preventing net debt increasing. The aerospace division performed better, mostly due to the restructuring activities performed previously, but sales only increased slightly which is disappointing given the poor first half of last year.

The energy and medical division showed further improvement but remained stubbornly loss making as the continued decline in the oil price affected sales. The group seem to be diversifying into gas projects but not enough to cover the loss in oil. Once again the Sellafield contract does offer some excitement going forward but it will be some time until it is contributing to any great degree. The board expect profits to be second half weighted so there should be an improved performance but they will have to perform very well to prevent any profit warnings in my view. I am not sure an uncovered dividend of 2.6% and forward PE of 10.2 adequately make up for the risks here. I am so far undecided…

On the 7th March the group announced that they have signed a ten year contract with Rolls Royce valued at more than £75M to supply pipe assemblies for a range of engine programmes including the rapidly growing Trent XWB variants fitted to the Airbus A350. The contract follows the acquisition of Rolls Royce’s internal pipe manufacturing business and I wonder if that was a condition of the contract being awarded? The assemblies will be manufactured in the UK and China and will provide a springboard for further recruitment as programmes such as the Tent XWB grow significantly in the coming years.

It is unclear how profitable this contract is but it does offer a decent platform and some certainty going forward and as such I have taken the plunge and bought in here.

On the 4th May the group announced that it has entered into an agreement to sell its Aerospace division to Anthony Bidco, a company controlled by funds managed by Silverfleet Capital, for an enterprise value of £65M which, after adjusting for debt and working capital will result in the company receiving proceeds of about £52M.

Following the transaction the group will continue to develop the energy and medical markets. As well as repaying the existing debts, it is intended that the group will return a substantial proportion of the proceeds of the sale to shareholders with the retained portion of the proceeds being used to continue to build a position in energy related markets and potentially in other high value engineering niches.

Last year, the aerospace division reported an operating profit of £3.3M and the net assets of the division are £26M. Following the completion of the disposal, the board expect to have net cash in excess of £47M. The company has received irrevocable undertakings to vote in favour of the disposal from shareholders representing 41.6% of the total issued share capital and I doubt they will have trouble obtaining enough.

The group as a whole has been trading in line with management expectations during the current year. Trading in the aerospace division has been marginally ahead of management expectations, driven by the Rolls Royce pipe business acquisition integrating ahead of schedule with integration costs that are lower than expected.

The energy and medical division continues to recover steadily and is expected to meet management expectations in terms of profit but sales are expected to be somewhat lower than expectations due to the Sellafield production start-up taking longer than expected and some delays in major gas contracts and prospects which have reduced the long term revenues that can be recognised in the current year. The board expect these revenues to be recovered in 2017, however.

The £47M ten year contract with Sellafield won last year represents less than 10% of the potential business that could be won with that customer and Sellafield accounts for about half of the nuclear decommissioning opportunities in the UK for the business with similar opportunities in other countries. There are also longer term opportunities in nuclear fleet refurbishment and the new build with EDF and others.

The board believes, therefore, that a focus on the prospects of the energy sector as well as a secure existing platform in the medical and biomedical equipment markets will provide the group the potential to achieve further growth.

So, this was a bolt from the blue. On the one hand, it is a bit of a shame to lose the most profitable part of the business but the price achieved is good and hopefully the board will be able to leverage significant value from the other parts of the business.

On the 30th June the group released an update on the return of capital to shareholders following the disposal of the Aerospace division. Following the disposal they had £47M in net cash and they intend to return £28M by way of a tender offer representing 100p for each share in issue (shares are currently at about 186p).

The balance of the net proceeds will be used to pursue the new strategy to invest in the energy and medical markets and more specifically to strengthen the group’s position in the nuclear sector and to pursue other related opportunities in the engineering sector.

On the 2nd August the group announced that it had signed a contract with EDF Energy worth £3.5M to supply components for their current fleet of seven nuclear power stations across the UK. Maloney Metalcraft will supply gas-cooling process-critical valves for each of the seven EDF managed gas-cooled reactors around the country. The contract is part of a life extension programme that will also see the business providing engineering support and on-site services to EDF as part of the deal. These contracts will continue until the end of life of the power stations.

The business designed and supplied the original Carbon Dioxide gas drying systems for the stations back in the 1970s but with further delays to the Hinkley Point C programme, extending the life of these older nuclear power stations has become critical.