Victoria Oil and Gas has now released its interim results for the year ending 2016. The company has changed its accounting reference date to 31st December and will release audited results for the seven month period to the end of December by the end of May. During the prior year a change in accounting treatment resulted in Cameroon Holdings being treated as an associate as opposed to an unlisted investment. The 35% ownership in the associate recovers a portion of the royalties paid by the group.

Revenues increased by $7.3M when compared to the first half of last year largely due to the gas consumed by ENEO. Production royalties grew by $619K and depreciation was up $3.7M which meant that gross profit was $3.1M ahead of last time. Sales and marketing expenses declined by $759K but share based payments were up $1.6M with other admin costs down $360K. We then see other gains/losses swing to the negative to the tune of $1.1M and after a $1.1M share of profit from the associate the group had an operating profit of $740K which, due to $49.8M of impairments last time, represented a $52.3M positive swing. Finance costs grew by $352K but income tax costs were down by $547K which gave a loss for the first half of the year of $890K, a decrease of $52.5M year on year.

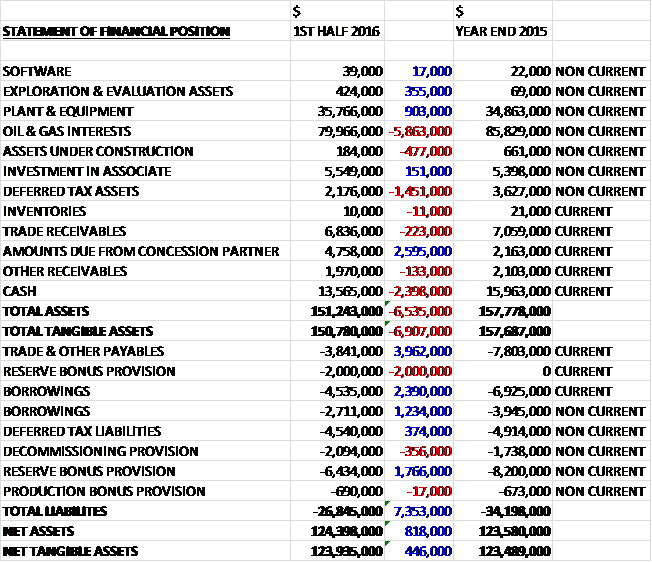

When compared to the end point of last year, total assets declined by $6.5M driven by a $5.9M fall in the value of oil and gas interests, a $2.4M decrease in cash, and a $1.5M decline in deferred tax assets, partially offset by a $2.6M increase in the amounts due from a concession partner and a $903K growth in plant and equipment. Total liabilities also declined during the period due to a $4M fall in payables and a $3.6M decrease in borrowings. The end result is a net tangible asset level of $123.9M, a growth of just $446K over the past six months.

Before movements in working capital, cash profits increased by $7.9M to $8.7M. There was a cash outflow through working capital, however, with a growth in receivables and a fall in payables which meant that the operating cash flow was $2.9M, a positive movement of $10.4M year on year. The group then spent $1.7M on tangible assets, mainly pipeline related, and $379K on intangibles and after a $971K dividend receipt from an associate there was a free cash flow of $1.8M. After finance costs of $871K and the repayment of $3.1M worth of borrowings, the cash flow for the half year was $2.2M and the cash level at the period-end stood at $13.6M.

The profit in Cameroon was $1.9M compared to a loss of $1.4M in the first half of last year. Gas sales for thermal and retail power were 656mmscf, a reduction of 63mmscf year on year whilst gas sales for grid power were 874mmscf compared to zero last time. In total, the average daily gas production was 8.85mmscf per day compared to 3.91mmscf per day last time; and condensate sales increased from 11,334bbls to 23,110bbls. Gas prices remained largely unchanged throughout the period due to the fixed price contracts in place but condensate prices have been negatively impacted by the global downturn in oil prices.

The gas sales figures currently represent 100% of the sales of the Logbaba project but during 2016, revenues will be split in accordance with the participating interests with just 60% being attributable to GDC as all of the exploration costs are expected to have been recovered. Management expect the point of revenue sharing to resume during Q1 2016.

ENEO consumed at the higher dry season level for June before reducing to the lower wet season take or pay levels for the remaining five months of the period. January 2016 marks the return to the dry season with the grid power sector now recording consistent consumption in excess of 9mmscf per day with January actually producing an average production of 13.9mmscf per day.

Within the period the group started the supply of gas to Dangote Cement, a 1.5M tonne per year clinker cement plant and also connected Societe Industrielle Camerounaise des Cacaos, a subsidiary of a Swiss-owned chocolate group and one of the world’s largest producers of cocoa. The business increased its capacity from 32,000 to 50,000 tonnes per year of cocoa following connection to the gas.

The loss in Russia was $464K compared to the $49.8M loss in the first half of 2015 relating to the full impairment of the assets.

It is worth noting the increase in receivables. Some $4.8M of these receivables (compared to $2.2M at the end of last year) are due from RSM and relate to RSM’s funding obligation for its 40% participating interest in the Logbaba concession. As the group are expecting RSM to start receiving its own share of earnings from the concession, I assume these don’t represent non-payment of receivables but perhaps indicate the ramp-up in gas sales.

The key objectives for the group in the year ahead are to increase gas supply to customers by 30%; to successfully complete a two well drilling programme for the expansion of gas reserves; to complete designs for increasing the gas treatment plant capacity to 40mmscf per day; to add over 13km to the pipeline network by building in new industrial areas; to progress new market products such as compressed natural gas; to continue to reduce production overheads across the group; and to expand business development efforts into other parts of Africa. The capital projects planned for 2016 will be funded through a combination of operational cash flows, partner contributions and debt.

The group has engaged Petrofac to manage the initial well design and services procurement phase of the 2016 well drilling programme and at the time of writing they had issued a letter of credit in the amount of $2M to a drill rig supplier for mobilisation costs and an additional $2M is committed upon presentation of a valid bill of lading of the specified drill rig. Further drilling-related purchase orders and commitments to date amount to $3.3M (a total of $7.3M committed so far then) and the company’s remains on track to spud the first of the two new wells by the middle of the coming year.

After the period-end, in February, the group reached an agreement with Glencore to acquire a 75% participating interest in the Matanda Block PSC with Victoria acting as operator. The assignment is conditional in the proposed work programme being agreed and other customary approvals from the government in Cameroon which will determine the acquisition date. The block borders the Logbaba concession at the southern boundary with about 70% of the block onshore. It is highly prospective for significant natural gas and gas condensate resources. The other 25% interest is held by Afex Global. One of the key attractions of the block is its proximity to the existing gas processing plant and pipeline network.

During the period, James McBurney resigned as a director and Iain Patrick was appointed as a non-executive director in December.

At the period-end the group had a net cash position of $6.3M compared to $5.1M at the end of last year.

Overall then, this has been a period of progress for the group. The losses fell and net assets grew modestly. There is also real progress on cash generation with the operating cash flow increasing and some cash actually being generated before financing, although it was all swallowed up by loan repayments. These figures represent the first supply to ENEO for grid power but it was also mostly during the wet season which has lower demand. As we enter the dry season, revenues should increase but unfortunately this coincides with RSM resuming its 40% share of sales so this will have a real impact on the figures.

Over the coming year the group is drilling two wells which will apparently be paid for using cash and debt (ie no placings) but whether this is achievable, I am not sure. They currently have $13.6M in cash with $7.3M of that already committed to the initial stages of the first well. It is unclear how much headroom is on the banking facilities but I suspect they will need to be renegotiated. The acquisition of the Matanda block looks to be a great, opportunistic play and one that adds a great deal of more potential.

I am torn here, for the first time in a long time, VOG is actually looking to be a decent investment but until I know how much the 60% of revenues will actually look like in profit terms and the costs of the wells, it is hard to take the plunge.

On the 13th April the group announced that it had agreed a $26M debt facility to support its production expansion at Logbaba through to 2017. They aim to avoid the equity markets whilst ensuring gearing is restricted to appropriate levels.

During 2016 the group intends to increase gas production from the Logbaba project by 30%, following the doubling in production in 2015. The key elements of the expansion programme are to drill one twin well and one step out well at the Logbaba plant sire with the objective of increasing production reserves; extend the Bonaberi pipeline to customers with gas service agreements in place; and to increase the gas processing plant capacity in three phases to handle the expected increased gas flow from wells. It is the group’s objective to fund the development through operating revenues and capital contributions from RSM (good luck with that!) in addition to the funding announced here.

The new facility has a repayment period of five years and incurs interest of 7.15% per annum.

On the 19th April the group released an operations update covering Q1 2016. Total gas sales of 1,131.2mmscf was an increase of 726.6mmscf when compared to Q1 last year. This growth has come entirely from an increase in supplies for grid power with thermal sales remaining flat at 250.6mmscf and retail power reducing by 53.4mmscf to 37mmscf. The total amount of condensate sold more than doubled to 13,591bbls. This resulted in revenues pf $12.8M and a net cash position at the end of the quarter of $4.6M compared to $5.9M at the end of the prior quarter.

These figures are in line with internal expectations as the quarter covered the first half of the dry season where gas consumption in the grid power sector is typically higher.

Following the approval of the work programme at the forthcoming operating committee meeting, the board expect to begin first work on Matanda at the end of 2016 once they have completed the Logbaba drilling campaign. Of the two wells to be drilled at Logbaba, one is a twin of the La-104 well drilled in 1957 and the other will be a step-out well that will be drilled into a target that is intended to prove up more of the group’s reserves. Both the wells will be drilled from a drilling pad adjacent to the gas plant and they will be tied into the production facilities immediately after they are completed.

In addition to developing the gas reserves, one of the wells has an additional objective of an exploration tail. This is to be drilled from the base of the Logbaba formation down to 4,200m below the surface to test the hydrocarbon potential of the Mundeck formation which had gas shows in La-104. A contract has been signed with Savannah Oil Services to provide the drilling rig for the project and it is currently on route to Cameroon. Petrofac is providing well design and project management services and the detailed design and programme preparation has started.

Major site preparation work is underway including slope stabilisation, full security fence line, levelling for drilling rig track and drilling pad preparation. New warehousing for rig supplies, storage and camp civils are also under construction and long lead time orders have been placed. The current plan is to start drilling in late Q2 and to complete by the end of the year. The budget total is less than $40M, significantly below the initial estimates but the start of the programme has resulted in some preliminary expenditure which explains the lower cash position at the end of the quarter.

The process plant expansion study has been completed. Stage one of the gas plant expansion to 25mmscf per day capacity (up from 20) is in the preliminary engineering phase and further phases will commence to tie in with well results.

An agreement was reached with SATOM, a road construction company, to lay GDC gas pipe and a bitumen road at the same time. 2.1km of pipeline has been laid during the quarter to be commissioned in phases over Q2 and new thermal customers are scheduled to come on line in Q2.

So, the new debt facility is good news as it reduces the need for a dilutive placing and things seems to be progressing well. The sales to grid power look decent enough but sales to other customers look rather disappointing.