The group has interests in Zimbabwe and Romania and has not generated any revenue to date. It has now released its final results for the year ended 2015.

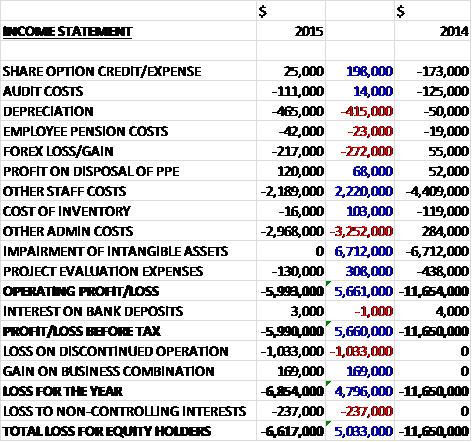

There were no revenues during the year as the group is pre-production. There are assets, however, after they were transferred from exploration costs, depreciation increased by $415K year on year. There was also a $272K swing to a forex loss. We then see a $2.2M decline in staff costs, offset by a $3.3M increase in other admin costs but there was no repeat of the $6.7M impairment of intangible assets that occurred last year and the operating loss improved by $5.7M. After a $1M loss from discontinued operation and a $169K gain on business combinations, the loss for the year came in at $6.6M, a decline of $5M year on year.

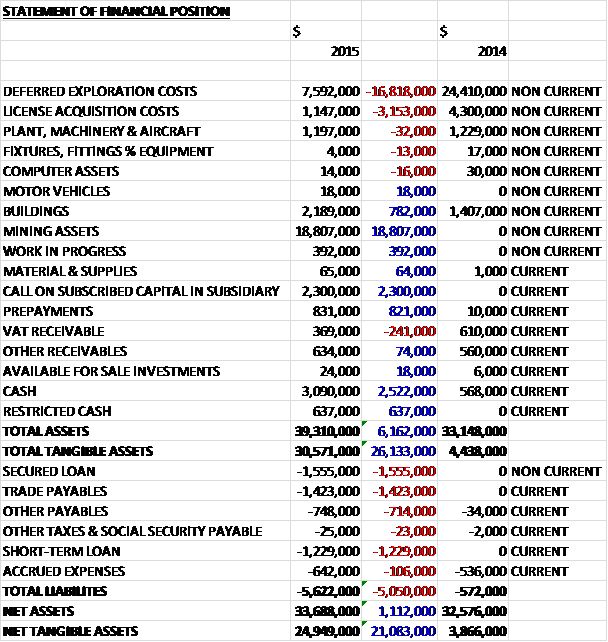

When compared to the end point of last year, total assets increased by $6.2M driven by an $18.8M growth in mining assets, a $2.3M call on subscribed capital in a subsidiary and a $2.5M increase in cash, partially offset by a $16.8M decline in deferred exploration costs as they were transferred to mining assets, and a $3.2M fall in license acquisition costs as they were also transferred to mining assets. Total liabilities also increased during the year due to a $1.4M growth in trade payables, all relating to Mineral Mining, a $1.6M increase in the secured loan, a $714K growth in other payables relating to the $625K payable to Baita, and a $1.2M growth in the short-term loan. The end result is a net tangible asset level of $24.9M, an increase of $21.1M year on year.

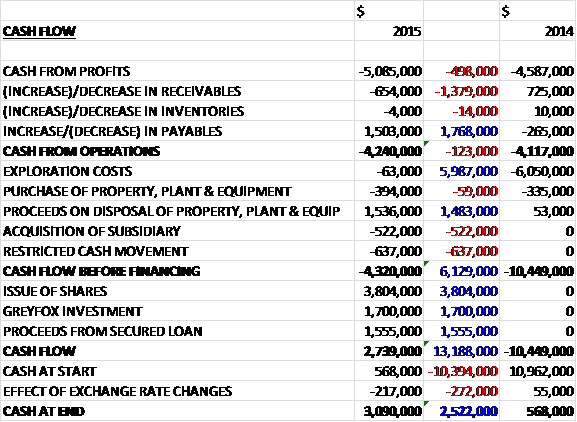

Before movements in working capital, the cash loss increased by $498K to $5.1M. There was a cash inflow from working capital due to an increase in payables so the cash outflow from operations was $4.2M, an increase of $123K year on year. The group then received a net $1.1M from the disposal of property, plant and equipment, and spent $63K on exploration costs along with $522K on acquisitions before a $637K increase in restricted cash meant that before financing there was a cash outflow of $4.3M. The group then issued shares which brought in $3.8M, received $1.6M from new loans and $1.7M from the Greyfox investment to give a cash inflow of $2.7M for the year and a cash level of $3.1M at the year-end.

The group has acquired a 50.1% interest in the operating opencast Manaila Polymetallic Mine and has started a number of projects to improve the efficiency and productivity of the mine. It may also be possible to extend the life of this mine by extending the open cast mine over the existing license boundary and by developing underground mining operations. They are also awaiting the transfer of the mining license for their 80% owned underground Baita Plai Polymetallic Mine.

The 50% owned Pickstone-Peerless gold mine project in Zimbabwe is well advanced and the board expect first gold production in Q3 2015. Overhead costs in the country have been materially reduced.

In Zambia the Kalengwa Kasempa copper project has been disposed of. The group retains ownership of the Nkombwa Hill rare earth project and agreement has been reached with the new owners of ACR Zambia to facilitate the development of this property over the next three years. In doing so, the group’s ownership will be diluted to 35% of that currently, but in a project that should develop materially.

In March 2015 the group exercised an option to acquire 80% of Mineral Mining, a Romanian company which is in administration and whose principal activity is ownership of the Baita Plai Polymetallic Mine and the principal reason for the acquisition was to reopen and operate this mine. Mineral Mining is subject to insolvency proceedings and as a result the mining license was transferred to a state company, Baita. Under the protocol, it was provided that a sub-license on the mine be granted back to Mineral Mining if the business was not declared as bankrupt which will be formally ended when it is merged with the group’s Romanian subsidiary. The acquisition remains subject to certain bureaucratic processes.

There is a debt due to Baita payable on the grant of the sub-license, the precise amount of which is disputed but will not exceed $625K (this is now included in an escrow account and is recorded under restricted cash). There are also $1.4M of trade payables relating to Mineral Mining and of this amount, $950K falls due for payment on the restitution of the mining license and the balance is payable by instalments starting on the restitution of the license.

It is worth noting that the other 20% of Mineral Mining is held by a group of senior directors of the group. Under an option agreement, should the option be exercised, the company would be required to pay up to $3.6M partly for contractual sums due to the former owners, partly to retire existing debts and partly towards due diligence costs, operational overheads and mine rehabilitation. This option was exercised when the company acquired their 80% interest.

The Baita Plai Polymetallic mine licence area contains eight skarn pipes, the first two of which currently contain the majority of the 1.8M tonnes of mineral resource, in situ grading 2.19% copper; 128g/t silver; 3.46% zinc; 3.07% lead and 1.41g/t gold. The mine is fully developed to 18 levels with all the necessary mining equipment, ore transport and hoisting facilities in place. Milling and flotation circuits are in place enabling the company to recommission operations reasonably quickly and cost effectively. Some of the equipment is old, but serviceable, and will be replaced through an orderly modernisation programme.

Significant areas of the unexplored skarn pipes are accessible, subject to re-entry procedures and will enable the resources of the company to be increased and upgraded in future. Following completion of the transfer of the mining licence, BPPM is expected to enter production in late 2015.

In July, the group announces that it had concluded an agreement to purchase just over 50% of the issued share capital of Sinarom Mining Group, a business that is operating the open pit Manaila Polymetallic Mine although this is still subject to the registration of the sale at the Romanian Trade Resistry. The mine has 1.8M tonnes of mineral resource, grading 1.1% copper; 45.9g/t silver; 1.86% zinc; 0.95% lead; and 0.63g/t gold. This is a working mine which will underpin the transformation of the group to a fully-fledged mining operation. Production started in August and a sale of the first concentrate batch is now being negotiated between different buyers.

In March 2015 the company concluded an agreement whereby it disposed of the whole of its interest in African Consolidated Resources Zambia ltd while retaining full ownership of the Nkombwe Hills rare earth project through continued ownership of Fisherman Mining ltd, subject to am earn-in agreement with the purchaser whereby they will acquire up to 65% interest in the project over the next three years. The proceeds from the sale of the business was $100K plus a further $1M conditional on the purchaser obtaining full access to the Kalengwa Mine property.

The group has also disposed of the Harare office for $1.4M and an exploration aircraft for $200K.

In Zimbabwe, the indigenisation regulations stipulate that all companies registered in the country with a net asset value of $500K or more transfer at least 51% of their issued to shares to indigenous persons within a five year period. These regulations are relevant to Canape Investments and its subsidiaries which are group companies registered and operating in Zimbabwe. Following the investment agreement with the partner in the Pickstone-Peerless gold mine, these regulations now come into effect in respect of Dallaglio Investments but the method of implementation of these regulations is unresolved and the group intends to await government guidance on this issue.

All other Zimbabwe businesses in the group are in a net liability position at the reporting date due to them being financed by loans from the holding or other group companies. As such, the directors believe that there is currently no compulsion to effect any transfer of shareholding in these subsidiaries to any third party or enter into any plan to do so. The full effect that this legislation might have on the operations of the group is yet to be quantified and is subject to some uncertainty.

The group has taken out secured borrowings of $1.6M at a hefty interest rate of 12% per annum. The loan is repayable in four equal six monthly amounts starting in April 2016 and it contains a conversion option whereby on default, the loan will be converted into Vast shares, although the directors think that this eventuality is unlikely. A short term loan of $1.2M was provided by a company associated with the chairman. This loan bears interest at 15% and is convertible at the lender’s election, into new shares at an issue price of 1.5p or the lowest price at which the company secures new funding prior to the repayment date. It has been agreed that the conversion rights will be exercised and it will be repaid by the issue of 154,649,140 shares at a value of 0.5p each.

During the year, in July, the company raised about $2M through a placing and a subscription at a price of 1.2p per share to further the company’s opportunities in Romania and for general corporate purposes. The board expect one of the Romanian mines to start generating cash in September 2015 and PPGM is expected to be cash generative in the same period. They are exploring debt finance as an alternative funding instrument, being mindful of the significant dilution that has been endured over the last year.

At the year-end the group had authorised capital expenditure amounting to $2.8M in respect of the Pickstone-Peerless gold mine in Zimbabwe and this expenditure will be incurred before the end of September 2015. At the year-end the construction of the new facilities is substantially finished, mining operations have started and the plant has been commissioned and is operation. First sales are expected within days and this will complete the transformation of the group’s activities in Zimbabwe from exploration to production.

It is worth noting that there are ongoing litigation proceedings in Zimbabwe relating to diamonds acquired in the country. It is fairly convoluted but I think the upshot is that the group is alleged to have registered claims to the diamonds in the names of non-registered companies which was prejudicial to the ministry of mines or that the group was illegally in possession of the diamonds which are being held in a vault at the Reserve Bank of Zimbabwe. The charges have been laid against a company which is a shelf company that has no staff. I doubt much will come of the litigation but I also seriously doubt the group will ever see their diamonds again!

At the year-end, the group has sufficient cash resources to support minimum spend requirements and general overheads for the next year but further funds may be required to finance the group’s working capital requirements and the development of the Romanian assets. The group has accumulated tax losses of $21.3M at the year-end. They are clearly feeling the pinch and various measures have been put in place to contain costs including placing staff on half salaries, retrenchment of excess staff and cessation of exploration activities to focus on mine development.

As there are no profits, there is not much point looking at the PE ratio for this year but on next year’s (admittedly rather old) forecast, the shares are trading on a forward PE of 8.1. At the year-end, the group had a net debt position of $306K.

Overall then, this seems to have been a year of progress for the group but it is still in the early stages and will need to raise further capital going forward to advance its mines. The Manaila mine looks most promising in the short term, having started production in August but the group still await a mine license at Baita Plai which seems like it is quite an old decrepit mine which will need some considerable investment going forward. It is expected to be in production by late 2015. The Pickstone-Peerless mine also has some $2.8M of investment to pay in the short term but should be producing gold in Q3. Zimbabwe frankly sounds like a bit of a nightmare location. Overall, there is far too risk in my view at the moment but I will keep track of progress.