Kalibrate Technologies has now released its interim results for the year ending 2016.

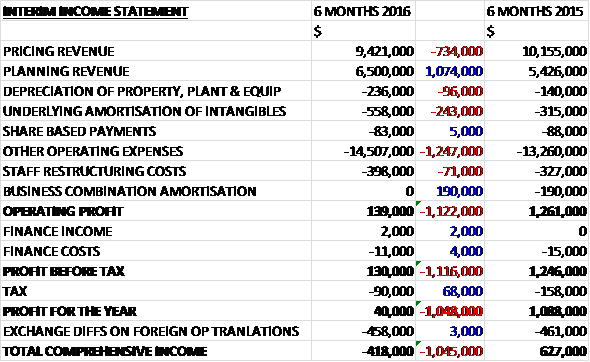

Revenues increased when compared to the first half of last year as a £734K decline in pricing revenue was more than offset by a £1.1M growth in planning revenue. Depreciation was up £96K and amortisation increased by £243K with other operating expenses growing by £1.3M. We also see exceptional items increasing by £71K relating to staff restructuring this year due to the downsizing of certain legacy areas of the business, and mostly flotation costs last time, but there was no amortisation of acquired intangibles which gave an operating profit some £1.1M below that of last time. After a modest improvement in finance costs, tax expenses fell by £68K which meant that the profit for the period was just £40K, a decline of £1M year on year.

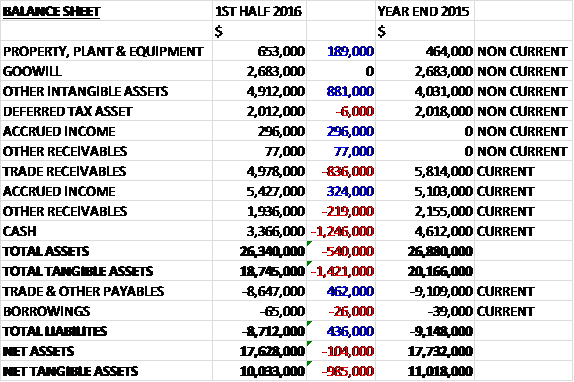

When compared to the end point of last year, total assets declined by £540K driven by a £1.2M fall in cash, an $836K decrease in trade receivables and a £219K fall in other receivables, partially offset by an £881K growth in other intangible assets, a £620K increase in accrued income and a £189K growth in property, plant and equipment. Total liabilities also declined during the period due to a £462K decline in payables. The end result is a net tangible asset level of £10M, a decline of £985K over the six month period.

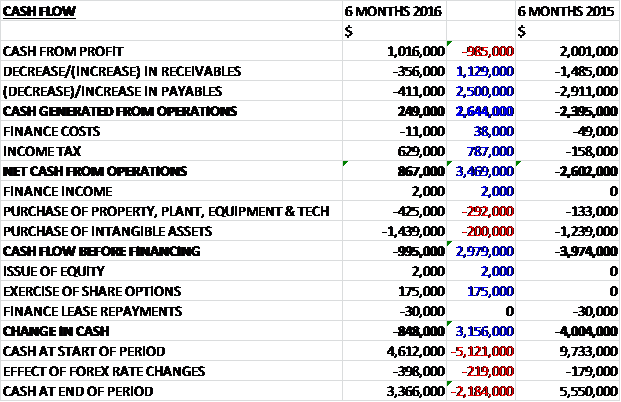

Before movements in working capital, cash profits fell by £985K. There was a cash outflow through working capital, but this was less than last time and after a £38K decline in finance costs and a £787K swing to a tax receipt, the net cash from operations came in at £867K, a positive swing of £3.5M year on year. The group spent £425K on tangible assets and £1.4M on intangibles, however, which meant that before financing there was a cash outflow of £995K. (It is worth noting here that amortisation was just £558K compared to the spend on intangibles, which was £1.4M). After a cash income of £175K from the exercise of share options, the cash outflow for the six month period was £848K and the cash level at the period-end was £3.4M.

The underlying loss in the Pricing division was £1M, a detrimental movement of £1.9M year on year on revenues that declined by 7.2%. This decline was related to the timing of closing several perpetual pricing license deals that were slated for this half of the year but have been pushed into the second half, along with a reduction in the non-core Price Tracker business line. Since the period-end, they have closed these deals with a healthy pipeline of other deals remaining for the second half of the year. By the period-end, the group have secured new managed services clients and the total managed service client base stands at 32. The focus is on continuing to convert existing clients and adding new clients to the managed services offering and they have increased staff resources to support the offering.

The underlying operating profit in the Planning division was £1.6M, a growth of £680K when compared to the first half of last year on revenues that increased by 20%, driven by significant increases in revenue from the European market and inroads made into the newly deregulated markets of India and Latin America. Going forward, the business typically leads the deregulation cycle as well as industry consolidation that is a trend in Europe and North America.

In North America, the group closed several pricing deals as SaaS, which is positive from a recurring revenue perspective. There was also a timing effect of closing a significant perpetual pricing license deal which slipped into H2 and has since been signed. Additionally there was a reduction in the group’s Price Tracker business. The planning business experienced a 2% increase due to the signing and implementation of several new market studies. Overall the net effect caused the revenue to decline by 4.8% in the period to £7.4M.

Revenue in Europe was about 16% higher due in part to the successful implementation of the significant market planning business. The new planning deals allowed the group to re-enter the markets of France, Belgium and the Netherlands. The pricing business was down in this half of the year due to fewer perpetual and SaaS pricing deals signed, but the pipeline for H2 remains strong for both pricing and planning.

The revenue for the rest of the world was flat year on year as the group saw increases in business related to the newly deregulated Mexican and Indian markets and increases in SE Asia offset by decline in the Japanese and African markets. With the deregulation trends continuing in various countries around the world, they see growing demand for both pricing and planning products in the ROW region. They experienced fairly rapid receptivity to its products in the newly deregulated Mexican market where retailers are adjusting to the new landscape.

While they experienced increased revenue in the Indian market, the overall marketplace is being more measured in its approach to deregulation so the process is moving at a slower pace than Mexico. The Japanese market experienced a decline in revenue mostly related to one of the group’s major clients placing its orders on hold for this half of the year as it completes its merger with another Japanese business. The markets of Africa and Japan have also seen softness in revenue related to the negative currency valuation trends, making the group’s products less competitive.

The decline in oil price has led to a fall in the average retail price of motor fuel. In times of prolonged price drops, the integrated refiner/retailers can experience capital pressures which may lead to delays in capital spending. To date the group has not experienced any demonstrable effects on its business but they continue to monitor the situation. The board believe that their business has been sheltered from the negative effects of the lower oil price because their client base comprises companies that mostly don’t participate in upstream activities; their pricing platform is a longer term business process that is not easily replaced; the volatility in fuel prices creates a greater need for companies to utilise the group’s products so that they can better navigate the changes; and with the continued trends of countries deregulating fuel prices there will be a need for solutions for pricing and planning.

A new merchandise Pricing and Promotion offering allows the company to provide both pricing and promotion data analytic solutions to convenience stores which aids retailers that operate both motor fuel and convenience operations. This also opens the market for convenience only retailers to work with the group’s products. As a result of cross-selling initiatives, another significant client now uses both the Pricing and Planning solutions, bringing the total using both to 32. In addition to these sales efforts, they have managed to record a 100% customer retention record.

Last year India, Mexico and Kenya announced that they plan to deregulate the operating control of motor fuel procurement and resale in their respective markets. The group are focused on all active deregulation processes and all potential areas of deregulation to ensure that they are involved in these opportunities. They are actively pursuing clients in certain countries in SE Asia and Africa in advance of the deregulation announcements that are anticipated to occur within the next two years. The group also provide business advice around the effects and process of government deregulation of motor fuel infrastructure.

The group have been marketing their 7 Elements for Fuel and Convenience Retail Success. This is a strategic analytic process that enables fuel and convenience retailers to understand and optimise performance across the entire consumer experience. The process uses a combination of proprietary modelling, extensive global market and site data sets and an understanding of fuel and convenience retailing to define a 7E score for each retailer in the market. It combines information that the group have amassed in their data warehouse to measure and provide a score upon which retailers can benchmark themselves against. This is the cornerstone upon which the group will deliver growth.

The group maintains up to date traffic stats at over 4 million traffic points in various countries around the world. They have resold this global data and continue to focus their efforts on finding new markets to sell this data to support the Planning business.

The planning business holds a lower initial gross profit during the start-up phase of a project because of the labour expense associated with the data collection, model set up and analytic modelling associated with some of the market studies and as such, the overall EBITDA margin was negatively affected in this half of the year. The group has a robust pipeline of pricing deals for H2, in addition to more Planning deals, which, if closed, could provide gross profit performance similar to prior periods.

The group have invested to strengthen their sales and marketing efforts, particularly related to dedicated resources to support the deregulation opportunities around the world, increased product development resources as well as added operational infrastructure to support growth in the managed services business. Many of these initiatives were started last year and as such, this half year period bore the full run-rate effect of these expenditures compared to the ramp-up period last year. In addition, the group also invested in its new Merchandise Pricing and Promotion platform, an additional offering through which the group can sell to its existing client base and attract new clients.

No dividends were proposed during the period but the board remain confident in the group’s ability to meet expectations for the full year as they are continuing to see good demand for their products both in core and new geographies. The group has $22M in recurring revenues as of the period-end, an increase of $1M over the past six months. The order book continues to improve due to ongoing demand for SaaS and as of the period-end, the order book stood at $42M compared to $41.4M at the end of last year.

During the period the group launched their new Merchandise Pricing and Promotion platform with pilots underway. During the second half they plant to commence marketing their Merchandise offering to both existing and potential clients. They continue to target growth opportunities in new geographic markets and are positioned to be a global partner for their large accounts by having 24/7 hosting capability which allows them to further opportunity to increase the recurring revenue.

On the 17th March the group announced that it had entered into a $5M revolving line of credit with PNC Bank. The facility will be used for the issuance of performance bonds of credit, forex facilities, potential business development opportunities and general working capital. It is for a two year term with an interest rate of 2% above LIBOR and there is an unused facility fee of 0.25%.

Overall then this has been a difficult half year period for the group. Profits have reduced and they are barely at a break-even level now; net assets have declined; and although the operating cash flow did increase, no free cash was generated and the improvement was down to better working capital movements with cash profits falling year on year. The pricing business incurred a loss this year which is being blamed on three large contracts slipping into the second half of the year (all of which have now been signed), and a decline in the non-core Price Tracker business. Conversely, planning profits have grown year on year with the improvement led by contract wins in Europe, Mexico and India with the latter two countries benefiting from deregulation of the industry.

In Japan, the group suffered from a major client merging with another business during the period but hopefully orders will pick up form them going forward. The board do seem confident of the H2 performance picking up the slack from a poor H1 but to me it looks like they have quite a lot to do to meet expectations for the full year. I suppose the convenience offering may be a driver for growth but I see no particular reason to invest in here on the hope that there are no further issues going forward.