Matchtech has now released its interim results for the year ending 2016. Following the integration of Networkers, the reporting structure of the group has changed to two main reporting segments, Engineering and Technology. The new Engineering segment includes the engineering business previously reported together with the Networkers engineering business and the professional services brands of Barclay Meade and Alderwood. The Technology segments includes the Connectus brand previously reported in professional services and the remaining Networkers business.

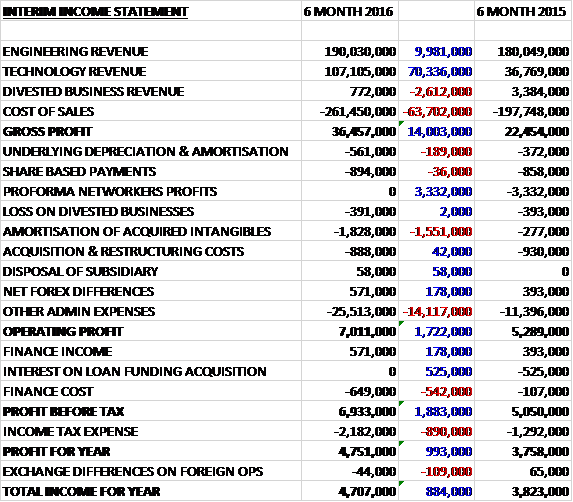

Revenues increased when compared to the first half of last year with a £70.3M growth in technology revenue and a £10M increase in engineering revenue. Cost of sales also increased to give a gross profit £14M above that of last time. There was a £3.3M charge for proforma Networkers profits last year, which I’m not sure I understand but this year amortisation of acquired intangibles increased by £1.6M, as would be expected following the acquisition. Other admin expenses increased considerably to give an operating profit £1.7M ahead. Finance income increased by £178K but finance costs remained broadly flat before an £890K growth in tax expense due to irrecoverable withholding tax in the acquired Networkers business and meant that the profit for the period came in at £4.8M, a growth of £993K year on year.

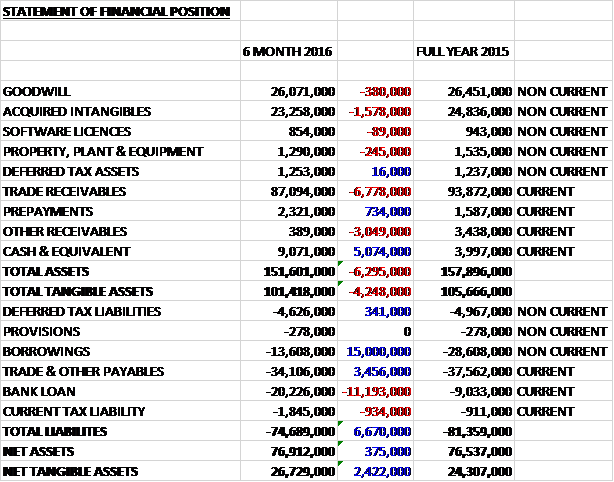

When compared to the end point of last year, total assets declined by £6.3M driven by a £6.8M fall in trade receivables, a £3M decline in other receivables and a £1.6M fall in acquired intangibles, partially offset by a £5.1M increase in cash. Total liabilities also decreased during the period as a £3.8M fall in borrowings and a £3.5M decline in payables was partially offset by a £934K growth in the current tax liability. The end result was a net tangible asset level of £26.7M, a growth of £2.4M over the past six months.

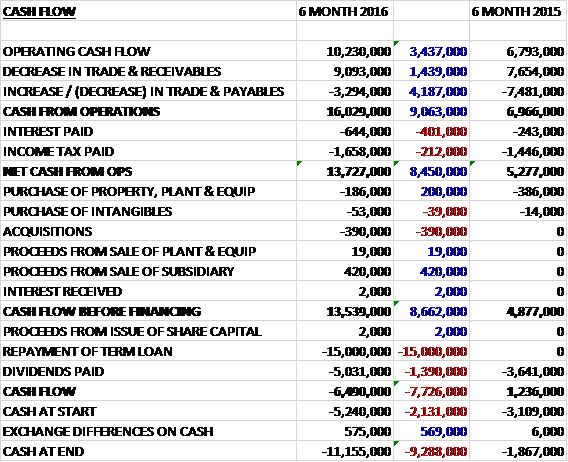

Before movements in working capital, cash profits increased by £3.4M to £10.2M. There was a cash inflow through working capital as a large fall in receivables was only partially offset by a decline in payables but both interest payments and tax costs increased somewhat to give a net cash from operations of £13.7M, a growth of £8.5M year on year. The group did not spend much on capex, with £186K going on tangible assets and £53K going on intangibles and the £390K spent on acquisition was offset by £420K received from the sale of a subsidiary. This meant that there was a strong free cash flow of £13.5M which was used to repay £15M of loans but a £5M dividend payment gave rise to a cash outflow of £6.5M and a cash level at the period-end of -£11.2M.

Overall the performance in the period was in line with management expectations with NFI growth in Engineering of 7% and Telecoms of 11% compared to the second half of last year, with IT down 9% on H2 2015 and falling by 20% compared to the first half of last year as demand for skilled engineers remained strong in the UK. Overall contract NFI declined by 2% to £26.5M when compared to H1 2015 and permanent fees increased by 2% to £9.4M. When compared to H2 last year, the performance is much better, however, with a 2% and 12% growth respectively.

The operating profit in the Engineering business was £6.1M, broadly flat year on year with an increase of just £6K. Contract NFI increased by 5% to £15.3M and permanent fees grew by 12% to £6.4M. There was a strong performance from infrastructure with NFI up 19% year on year. There is continuing high demand in the rail sector, mainly in project delivery, in property largely with private sector structure/service work and in water with design/project delivery phases. With many major projects in the pipeline, such as the Thames Tideway Project, HS2, Crossrail phase 2 and the Wessex to Waterloo line improvements, the group have long term visibility in this sector.

In Energy, whilst the low oil price means activity remains muted globally, the group has diversified in recent years which meant that two thirds of their business lies outside the oil and gas market. There are an increasing number of requirements for candidates throughout Europe in the renewable energy, transmission and nuclear markets. In renewable energy the main focus is within offshore and onshore wind programmes where there a number of upcoming opportunities in Northern Europe. Within the transmission area there are extensive upgrades being carried out to the electrical grid infrastructure throughout Europe, whilst in the nuclear sector there are a number of new reactors being planned in the UK alone.

Investment in the UK automotive manufacturing industry continues, which is flowing down through the supply chain, where the need to design new automotive technologies, particularly hybrid and alternative fuel transmissions, is increasing. The group are also seeing signs of UK automotive companies looking to re-shore certain operations and further expand. The aerospace sector is focussed on increasing manufacturing production rates, as no major new aircraft models are in the pipeline. The large aftermarket retrofit and interior suppliers are struggling to keep up with design and production demand, hence increasing the group’s opportunities with SMEs.

In maritime much of the growth is coming from the international team, particularly in Canada where the NSPS naval ship building programme will span the next thirty years and the group is well positioned as a key supplier of global talent to the two prime shipyards. Elsewhere, super yacht build and cruise liner refit and repair projects in Europe are creating opportunities in design, build and project management.

The operating profit in the Technology business was £4M, a growth of £3.2M when compared to the first half of last year. Contract NFI reduced by 10% to £11.2M and permanent fees fell by 14% to £3M year on year, although against the second half of last year, contract NFI was down 2% and permanent fees were up 8%. Telecoms was in line with the first half of last year but IT was down 20%.

Although overall demand for IT staff remains high, the shortage of candidates in specific areas means that the group needs to be increasingly specialist in their approach. The group are focused on six core markets, five of which are across specific technology skillsets, with the objective of becoming the leading specialist recruiter in each of these markets. They are digital/mobile development, cloud, cyber security, leadership and ERP. At the same time they will build on their success in the public sector, expanding their teams in the NHS through their presence on the non-medical framework as well as developing their central and local government business.

The telecoms market is currently quite buoyant as it increasingly converges with the IT sector. In addition, they are seeing growth in Asia from the continued expansion of 4G. They have also seen a resurgence of fixed line business in North America and Europe where there is a renewed investment in cable laying, enabling higher quality and faster streaming. As 5G is eventually rolled out the group are well placed to support their clients as the technology is deployed.

The integration of Netoworkers continues to go well. The group have identified nearly £2.3M in annualised synergies since the acquisition which will be fully realised in 2017. The board expect to identify additional cost synergies as they continue the integration process and combine the remaining back office functions by the end of this year.

With the board mindful of the increased caution in economic forecasts in recent months, based on opportunities won, trading in the two months since the half year and continued close cost management, they anticipate the group’s results for the year will be in line with management’s expectations.

After a 6% increase in the interim dividend the shares are currently yielding 4.8% but this falls to 4.3% on the full year forecast for some reason. The forward PE ratio at the current share price is 10.2 which looks like decent value. The group had a net debt position of £24.8M compared to £33.6M at the same point of last year.

Overall then, this was a fairly mixed period for the group with the Networkers acquisition masking sluggish underlying demand. Profits were up, net assets increased and the operating cash flow improved with a strong generation of free cash, although perhaps it might be an idea to hold off a bit on the dividends while the debt is paid off.

The performance in the engineering division was flat as a growth in infrastructure NFI was offset by continued difficulties in the energy market following the oil price collapse. The acquisition meant that profits in the technology division increased but like for like NFI declined as the IT business suffered due to a lack of suitable candidates.

Clearly the Networkers acquisition is the main differentiator in performance and the integration seems to be going well. There is still quite a bit of debt here but the balance sheet can support it and despite the sluggish underlying performance, the forward PE of 10.2 and dividend yield of 4.3% seems pretty decent value to me. I am now back in there.

On the 18th July the group announced that they intend to change their name to Gattaca. They will continue to trade through their core brands Matchtech and Networkers, however. They will also have a new ticker. Good grief, it was a decent enough film but I can’t get behind this one! The change of ticker is going to balls up my charting software too.

On the 4th August the group released a trading update covering the year ending 2016 where the board reiterated that they expect profits to be in line with previous expectations. Total NFI is up 34% with contract up 35% and permanent increasing by 30% but this is due to the acquisition and like for like NFI was up just 1% reflecting a 4% growth in permanent NFI and flat contract NFI. By market, this reflected a 6% growth in engineering NFI and a 6% decline in technology NFI. The second half of the year was slightly stronger, however, with a 3% increase compared to a 1% decline in H1.

There was strong annual growth in infrastructure, professional staffing and engineering technology offset by a weaker performance in oil & gas and maritime. The IT market segmentation and sales restructure carried out in Q4 is already starting to show an improvement with NFI stabilising in H2 as further benefits are expected to be seen in the coming year.

During the period the group appointed regional MDs to run the Asia and Americas operations and a number of experienced UK based consultants and managers are transferring to the Dallas office in order to accelerate the development of the engineering business in the US. The integration of Networkers is expected to be fully completed by December 2016.

At the year-end, net debt stood at £27.5M, down £6.1M over the year. Demand for skilled engineers remains strong in the UK and so far the group have not seen any impact on vacancy flow in the six weeks since the Brexit vote. They have seen strong growth in the Engineering division and in Technology the sales restructuring undertaken in the IT business gives the board confidence for the coming year.

This all seems to be quite good – momentum seems to be improving after a poor first half and so far there does not seem to be any Brexit issues – could be worth an investment at these levels.

On the 11th August the group announced that CEO Brian Wilkinson purchased 47,722 shares at a value of £170K which gives him a total of 92,722 shares – this is actually a fairly hefty purchase.