Character has now released its interim results for the year ending 2016.

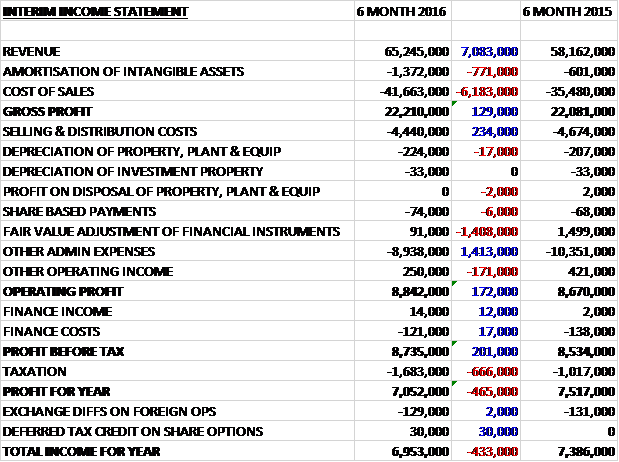

Revenue increased by £7.1M when compared to the first half of last year but this growth was broadly offset by an increase in amortisation and other cost of sales so that the gross profit was £129K above that of last time. Selling and distribution costs fell by £234K and a lower fair value adjustment of financial instruments, reliant on exchange rates at the balance sheet date, was offset by a fall in other admin costs and after the other operating income declined by £171K, the operating profit was £172K ahead of last time. There was a modest fall in finance costs but the tax charge increased by £666K which meant that the profit for the period came in at £7.1M, a decline of £465K year on year.

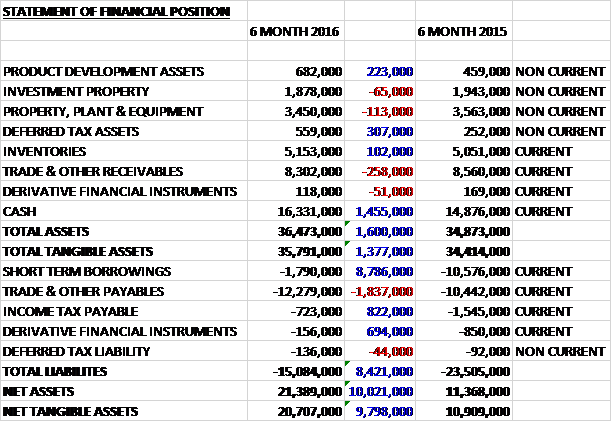

When compared to the end point of last year, total assets increased by £1.6M driven by a £1.5M growth in cash. Total liabilities fell during the period as an £8.8M fall in short-term borrowings, an £822K decrease in income tax payable and a £694K decline in derivative financial liabilities were partially offset by a £1.8M growth in trade & other payables. The end result was a net tangible asset level of £20.7M, a growth of £9.8M over the past six months.

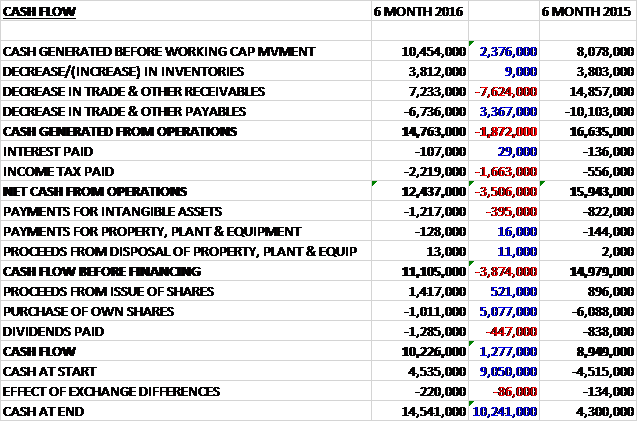

Before movements in working capital, cash profits increased by £2.4M to £10.5M. There was a cash inflow from working capital, although this was less than last time as the fall in receivables was less pronounced and after a £1.7M growth in tax payments, the net cash from operations was £12.4M, a decline of £3.5M year on year. The group spent £1.2M in intangible assets and £128K on fixed tangible assets to give a free cash flow of £11.1M, and after some cash was spent on dividends and the group received cash from new shares, the cash flow for the first half of the year was £10.2M and the cash level at the period-end was £14.5M.

The group have made good progress with overseas sales, particularly in the US and overseas sales now make up 24% of the total compared to 17% in the same period of last year. Underlying margins have remained consistent but the increase in international sales has led to a slight decrease.

The top performing brands during the period included Peppa Pig, Little Live Pets, Minecraft, Scooby Doo, Fireman Sam and Teletubbies. Peppa remains the lead brand but there has been strong demand for the Teletubbies product since launch in January, from which time it has performed well. New licenses secured in the period include Stretch Armstrong, a range of products will be launched on a global basis including the US where a new TV series is being developed by Netflix.

During the period the company acquired a total of 213,936 of its own shares at a cost of £1M with the average price of £4.70 per share but there have been no further buy-backs since the period-end. It remains part of the group’s strategy to continue to repurchase their own shares when appropriate under the current share buyback programme, although they don’t seem to be being cancelled so I’m not sure what the ultimate intention is.

In February, Kiran Shah and Jon Diver took on the sole role of joint MD. At the same time the group appointed CFO Mark Dowding to the board as group finance director, and Character Options MD Jerry Healy as group marketing director. Clive Crouch was also appointed as a non-executive director. Also, after being involved with the business since 1991 and the executive chairman since 1995, founding director Richard King relinquished his executive role on the board, however he will remain as non-executive chairman.

Current trading continues to be encouraging and the group remains on target to achieve market expectations for the full year.

At the end of the period the group was in a net cash position of £14.5M compared to £4.5M at the year-end and £4.3M at the same point of last year. After a 40% increase in the interim dividend, the shares are yielding 2.5% which increases to 2.7% on the full year consensus forecast and the forward PE ratio is 11.1 at the current share price.

Overall then, this was a solid set of results. The profit did fall but this was due to a higher tax charge and pre-tax profit increased. The net asset level showed strong growth and although the operating cash flow fell, this was due to working capital movements not being as strong as last time and cash profits increased with loads of free cash being generated.

The US seems to be working quite well with an increase in sales and both the Teletubbies and stretch Armstrong look interesting going forward. There is a fair amount of change at the board level which can be a risk so well worth keeping an eye on but with a strong net cash position, a forward PE ratio of 11.1 and yield of 2.7% these shares look good value to me.

On the 23rd June the group announced it had purchased and cancelled 45,000 shares at a value of £232K. It has the capacity to buy back a further 3,093,700 under the authority granted at the AGM.

On the 11th July the group announced that non-executive director David Harris purchased 3,000 shares at a value of £13.2K. He now owns 51,403 shares.

On the 14th September the group released a trading update where they stated that they had made solid progress and they expect to deliver results in line with market expectations. All of the major product ranges have performed well.

A recent extension to the portfolio is Stretch Armstrong, produced under a master license agreement with Hasbro and sold on a global basis. Sales in both the UK and international markets have started very well and the group is currently developing a wider range of interesting products within the brand. Another new product range launched recently is Twozies, a girls’ collectable item. Early results are promising and the board is confident that the product will become a top 10 brand in 2017.

A significant proportion of the group’s purchases are made in US dollars and the increasing strength of the currency against Sterling puts pressure on profitability. Nevertheless, the board believes that they can continue to mitigate the resulting increased costs through the expansion of the international business and active programmes of monitoring all costs and rationalising operations where possible.

On the 21st September the group announced that finance director Mark Dowding purchased 10,000 shares at a value of £43.5K which gives him a holding of 83,841 shares. Also, non-executive director David Harris purchased 4,597 shares at a value of £20K to give him a holding of 56,000 shares.

In addition, on the 22nd September the group purchased for cancellation 292,402 shares at a value of £1.3M. This represented about 1.36% of the total issued share capital.