Bioquell has now released its final results for the year ended 2015.

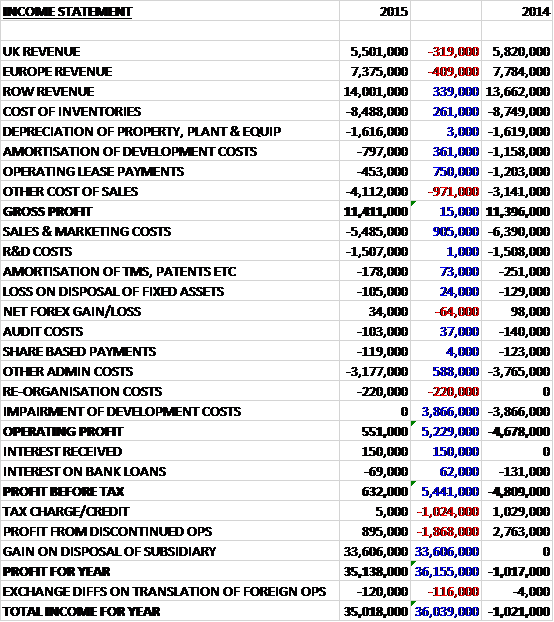

Revenues declined when compared to last year as a £339K growth in ROW revenue was more than offset by a £409K decrease in European revenues and a £319K decline in UK revenue. Cost of inventories fell by £261K, amortisation was down £361K and operating lease payments fell by £750K, but these costs were offset by a growth in other cost of sales to give a gross profit that was flat year on year. Sales and Marketing costs fell by £905K, however, and admin costs also decreased but there was a one-off £220K reorganisation cost relating to costs of redundancies in Q4, before the lack of development cost impairments, which were £3.9M last year, meant that the operating profit showed a £5.2M positive swing. The group then received £150K in interest and paid out less in finance costs before a £1M reduction in tax income, mainly due to changes in deferred tax, a £1.9M fall in profits from discontinued operations and a £33.6M gain on the disposal of a subsidiary gave a profit for the year of £35.1M, a positive movement of £35.1M year on year.

When compared to the end point of last year, total assets increased by £28.7M driven by a £44.7M growth in cash, partially offset by a £6.9M fall in fixtures and equipment, a £5M decline in trade receivables, a £1.4M decrease in land and buildings and a £961K decline in prepayments and accrued income. Total liabilities fell during the year due to a £1.8M decrease in accruals and deferred income, a £1.3M fall in bank loans and a £643K decline in deferred tax liabilities. The end result was a net tangible asset level of £56.1M, a growth of £34.8M year on year.

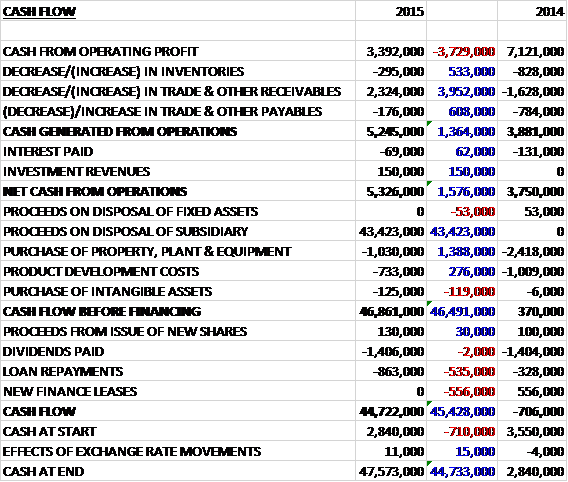

Before movements in working capital, cash profits declined by £3.7M to £3.4M. There was a cash inflow from working capital, however, with a particularly large fall in receivables so that after some interest income was received too, the net cash from operations came in at £5.3M, a growth of £1.6M. The group spent £1M on property, plant and equipment; £733K on development costs and £125K on other intangible assets and after the £43.4M cash receipt from the sale of the subsidiary, there was a cash flow of £46.9M before financing. Of this, £863K was used to repay loans and £1.4M was paid out in dividends to give a cash flow for the year of £44.7M and a cash level at the year-end of £47.6M.

Underlying demand from the Life Sciences and Healthcare sectors increased in the year. Micro-organism contamination remains an ongoing challenge in these sectors around the world and regulatory oversight is increasing. There was a significant increase in sales of Qube and the group launched a new, small and easy to use room decontamination technology designed for the healthcare market, the BQ-50 which saw encouraging levels of initial market demand. Cost reduction in the second half of the year resulted in annualised savings of about £1M.

Life Sciences revenues increased by 1% to £19.1M, in part reflecting a markedly improved performance from the Asia Pacific business offset by a year on year decline in the US. Healthcare revenues were flat at £4.2M but the prior year included a one-off order to the Middle East worth some £500k. Defence revenues declined by 14% to £3.5M and total services revenues fell by £400K to £10.9M reflecting some headwinds encountered in the US with the RBDS decontamination service business.

Geographically, the business in Asia Pacific improved significantly under different management and the start-up in Germany grew strongly reflecting the strength of the life sciences sector in the country. In addition, the Irish business started to show real progress towards the end of the year following a difficult first half. The US should be the group’s largest market and during the year they made changes to the way they take their products to market and have made further changes since the year-end to improve the performance of this business.

The board see substantial opportunities for their Qube product range, particularly on the back of developments associated with cell therapy. They continue to improve their Pod products, which enables them to convert open plan units in hospitals to single occupancy rooms in a matter of hours. To date they have focussed these activities on the UK but they intend to roll out internationally during 2016. The defence business remains lumpy. In the short term the order book is relatively low but the prospect list for 2017 and beyond is better than it has been for some time.

In May 2015 the group sold TRaC Global which carried out their testing, regulatory and compliance work. The business was profitable, making £3.5M in 2014 and the group made a £33.6M gain on disposal with a cash receipt of £44.5M.

The substantial phase of significant capital investment in new products and services is essential over and going forward the board would expect to see product line extensions and technology updates but a markedly lower requirement for investment in product development. Moreover, the bio-decontamination division generated cash in 2015 on a standalone basis. The Asian life sciences business has responded well but there is still more work to do in the US business, however the prospects for the group’s products and services in the life sciences sector look encouraging.

Going forward, the board believes that their product range is well positioned to benefit from strong underlying drivers of growth and underlying demand for the eradication of bioburdon and the provision of an aseptic environment remains strong in the life sciences sector. Antibiotic resistance and hospital acquired infections are increasing issues for healthcare providers globally and there remains ongoing geopolitical stress in a number of parts of the world which helps drive demand for the defence business. Overall, the new year has started steadily.

Given the huge £47.6M net cash level it is pretty much meaningless to try and value the company on a PE ratio, especially given that there does not seem to be any market forecasts. The board have decided that it would not be appropriate to pay a dividend for the year.

In addition to the results, the group have announced that the board have concluded that it would be helpful for the strategic review process and in the best interests of shareholders if a substantial proportion of cash was returned to shareholders by way of a tender offer. They intend to launch a tender offer in respect of 50% of the issued share capital at a price of £2 per share and they have 42.7M in shares in issue so they are returning the equivalent of £1 per share. I am not sure I fully understand why the cash on the balance sheet is making things difficult but the tender amount of £2 seems fairly good for shareholders although I am unsure as to exactly how the process works.

Overall then, this seems to be a fairly solid update. The remaining business now seems to be profitable on an underlying basis, net tangible assets increased following the disposal and the operating cash flow improved with a decent amount of free cash being generated, although this was due to a decline in receivables and cash profits fell year on year. The life sciences business recorded broadly flat revenues as growth in Germany and Asia offset declines in the US; the healthcare business was also flat, although this was a decent performance given the large one-off Middle East order received last year; the defence business performed less well with declining sales due to difficulties in the US.

The main event is obviously the TRAC sale and the fact the group is returning much of the cash to shareholders. Given the muted start to the year with “solid” trading and the fact a buyer for the rump of the business still does not seem to be forthcoming, I am wondering if I should sell my shares here after making a modest profit.

On the 21st June the group announced the results of its tender offer. A total of 20,405,814 shares were tendered by shareholders and purchased for £40.8M, representing about 47% of the total share capital.