Revenues increased when compared to last year with a €19.3M growth in gaming NGR and a €3.7M increase in sports NGR and after variable costs increased by €10.9M, the gross profit was some €12.1M ahead. Personnel expenditure grew by €5.4M and technology costs were up €2.7M but office and travel costs fell by €1.8M. Forex differences worsened by €698K and amortisation grew by €873K due to the prior increased spend on IT, but this was offset by a €377K fall in the Betit put option value and a €4.8M positive movement in the value of derivative financial instruments.

We also see a host of non-underlying costs which included €12.5M of acquisition professional fees, a €9.5M cost relating to the fair value of adjustment of the currency option, €847K of PR fees and €1.2M relating to Romanian tax amnesty payments. All this meant that the operating profit came in some €15.2M below that of 2014. As far as finance costs are concerned, the main movements were a €656K reduction in the unwinding of the discount on the Betboo consideration, offset by the first €1.2M interest payments paid on the Cerberus loan. After tax increased by just €119K, the profit for the year was €24.7M, a decline of €15.9M year on year.

When compared to the end point of last year, total assets increased by €23M, driven by a €7.8M growth in prepayments, a €7M increase in cash, a €3.3M growth in cash balances with customers, a €3.8M Winunited option asset, a €2M increase in income tax reclaimable and a €1.2M growth in software licenses, partially offset by a €1.2M decrease in the value of the Betit investment following an impairment. Total liabilities also increased during the year as a €19.8M initial Cerberus loan was taken out, a €9.9M forward contract liability was incurred, a the share option liability increased by €11.6M, accruals grew by €4.7M and income taxes payable increased by €2.2M, partially offset by a €2.5M reduction in the amount due on the William Hill loan. The end result, once goodwill is removed, is a net tangible asset level of -€4.8M, a detrimental movement of €21.3M year on year.

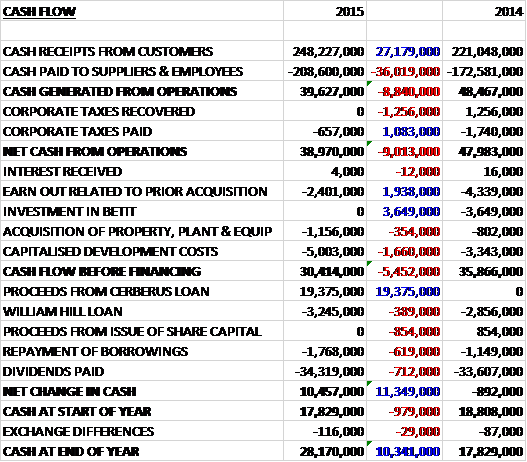

Cash receipts from customers grew by €27.2M but cash paid to suppliers and employees increased by €36M which meant that after tax the net cash from operations came in at €39M, a decline of €9M year on year. The group spent €2.4M on the earn-out for a prior acquisition and €1.2M on property, plant and equipment, along with €5M on development costs which meant that the free cash flow was €30.4M which was all spent on €34.3M of dividend payments. We also see the group paid back €3.2M of the William Hill loan and €1.8M of other loans but took out €19.4M in new loans from Cerberus to help pay for some of the pre-acquisition costs. The end result was a cash inflow of €10.5M and a cash level of €28.2M at the year-end, although this should be viewed in the context of the post-year-end acquisition.

Clean EBITDA in the second half of the year was €28.6M which compares favourably to €26.8M in H2 last year and €25.5M in the first half of this year. The group has been impacted during the year by the point of consumption tax in the UK and by EU VAT imposed by certain jurisdictions on gaming revenues. The combined impact of that on the enlarged group during the year was €12.4M.

Sports wagers increased by 15% to €1.683BN during the year but sports margin softened somewhat from 9.8% last year to 9.2% in 2015. This meant that sports revenue increased by 3% to €113.8M but gaming revenue fared much better with a 17% growth to €133.9M although total daily sports NGR was €712K in Q4 which was the highest quarterly total during the year. Q1 2016, when including bwin results saw sports wagers of €10.626M per day with a sports margin of 8.8% generating daily NGR of €1.843M.

Over the coming year the group hope to quickly assimilate bwin.party into the group and drive cost synergies; increase the product quality to improve the customer experience; increase the sports margin and cross sell additional gaming products to customers; focus marketing expenditure on areas where they can measure the return on investment; fully leverage the substantial IP across the enlarged group; review non-core assets and identify potential disposals; and inject a cultural change to bwin.part to recognise financial performance as the success trigger for incentives.

As part of the requirements for the acquisition of Bwin.Party, the group had to “cash confirm” that is had sufficient Sterling funds to meet the obligations of the acquisition. As the loan facility from Cerberus was denominated in Euros, a call option was purchased for €5.3M in September to sell €365M and purchase £256M, a rate of £1 to €1.425. In December it was decided to terminate this option and replace it with a forward contract with option components.

Entering into this transaction resulted in a refund of €5.6M and a new sale of €365M and a purchase of £260.7M, a rate of £1 to €1.4. By the year-end, forex rates had moved and the rate used by the group for the translation of its GBP current assets and liabilities was £1 to €1.36249 whilst the effective rate behind the valuation of the GBP obligation under the flexible forward was €1.3621 which resulted in a revaluation charge of €9.9M shown as a forward contract liability. Additionally there was a €627K adve3rse movements on other forex differences, mostly relating to the retranslation of the remaining outstanding William Hill loan.

In March 2015 the group contracted with Winunited for the day to day back office operations of their business. Under the terms of the agreement, GVC obtained a call option to purchase the Winunited assets comprising various intangible assets. The exercise period for the option is in the three months prior to the five year anniversary (so Jan to March 2020) and no consideration was paid for the option. As things stand at the year-end, this call option is determined to be an asset worth €3.8M. The Betit call option is valued as a liability of €736K and can be exercised between July and September 2017 with a minimum call option price of €70M. Betit underperformed against the previous forecast provided by the management which decreases the expected value of assets so the available for sale assets decreased by €1.2M, and the cost of the options, with the liability falling by €1M.

In September the group entered into an agreement with Cerberus for a loan of up to €400M in order to part fund the acquisition of bwin. Under the terms of the loan, a hedging loan of €20M could be drawn down in advance of the acquisition in order to fund the hedging arrangement for the conversion of the loan funds into sterling and to pay for initial costs including loan arrangement fees. The balance of €380M was drawn down in February 2016 and the full amount of the loan is to be repaid by September 2017. The loan incurs an astonishing interest of 11.5% above a 1% EURIBOR floor so the priority must be to pay back this very expensive financing, particularly as there is also a 1% anniversary fee and a 2.5% 18 month fee.

One thing that is a constant niggling annoyance with this company is the generous share option scheme. Last year the board awarded themselves 3,450,000 options at an exercise price of 1p, some 125,000 were surrendered during the year so there remained 3,325,000 existing at the year-end. These awards will vest in full on the share price being equal to or exceeding £6 per share for three months but these options were cash-cancelled after the year-end on the completion of the acquisition and the proceeds were re-invested in new GVC shares. In all, the board are very generously remunerated here with the CEO taking home €4.7M and the Chairman trousering and incredible €1.7M.

In addition, some 3,200,000 fully vested share options that were granted in 2010 and 2012 were surrendered which meant that the board would receive cash payments of €12.2M. The first payment of €508K was made but subsequent payments were put on hold pending the outcome of the acquisition and at the year-end the outstanding liability was €11.8M, although these were also cancelled after the year end. As far as I can tell, there are now about 17.8M options over shares that will pay out if the total shareholder return ranks median or above the FTSE250. At least these actually have an exercise price, being 422p but they really do seem excessive to me.

After the year-end, obviously the major event was the acquisition of bwin.party in February for a total consideration of €1,508M. This generated goodwill of €951.9M and the consideration was paid as follows: €1,201.5M was paid in GVC shares; €278.5M was paid in cash; and €28.3M in cash settled options. There was also €9.6M of business combination costs that were incurred in 2016. Last year the acquired group earned clean EBITDA of €108.5M but made a pre-tax loss of €40.2M.

Following the acquisition the group expects to generate significant synergy savings through integration and restructuring of operations which include the migration of GVC’s sportsbook onto bwin’s technology platform; the termination of all sponsorship programmes; restructuring bwin.party’s casino and poker operations, including integrating GVC’s poker operation onto the bwin platform; operational efficiencies in customer services, IT and marketing functions; and the integration of some back office functions which may lead to redundancies.

As already stated above, the cash element of the acquisition was funded through drawing down of the Cerberus loan facility. On the same date as the acquisition, the group issued additional shares at a price of 422p. These shares consisted of 27,978,812 placing shares, including the purchase by directors under the terms of the LTIP and 7,566,212 subscription shares. The cash consideration of these shares was £150M. The net proceeds of these shares are to be used to fund reorganisation costs of £44M, repay existing debt facilities of bwin.party of £45M and to fund working capital of £56.1M.

The group has appointed three additional non-executive directors: Norbert Teufelberger, who joints from bwin.party; Stephen Morana and Peter Isola and are seeking admission to the premium segment of the official list as soon as practicable.

It should be noted that the group are somewhat susceptible to the Brexit vote as it may increase the volatility of global currency and financial markets along with potentially reducing their ability to operate in certain EU markets without a change in domiciliation which could carry a higher tax burden. As well as licenses in the UK and Gibraltar, they also have licences in Malta, Denmark, Italy, France, Romania, Greece and Germany.

In Q1 2016, total group NGR was €167.7M, up 180% following the acquisition of bwin at the start of February. Like for like NGR per day was up 9%. Year to 20th April like for like NGR was up 13% for the group as a whole, with GVC brands up 18% and bwin brands up 11%. Party Poker showed the first year on year quarterly growth in five years and the group is on track to secure €125M of synergies by the end of 2017, the full benefit of which will be seen in 2018. Net debt as of the 17th April was €193M with gross cash of €327M. Daily NGR at bwin, since it became part of the group, increased 8% in Q1 2016.

At the current share price the shares are trading on a PE ratio of about 17.5 which increases to 20.1 on next year’s consensus forecast, although not much can be taken from this really as it is a year of significant disruption. The 2017 forecast of 11.5 is possibly more relevant here. The dividends paid out during the year represent a yield of about 8.9% but going forward there will be no dividends paid in the coming year as one of the conditions of the debt financing, so the forward yield for 2016 is zip.

Overall then, this has been a year of change for the group. Profits declined but this was due acquisition-related professional fees and the fair value adjustment on the currency option and underlying profits increased. Net tangible assets declined and are now negative but this is likely to change after the acquisition and as it is mainly equity related, net tangible assets should actually increase. The operating cash flow declined but there was still plenty of free cash generated, even if it is all paid out in dividends.

Gaming NGR showed impressive growth in the year, up 17% but growth in sports NGR was more pedestrian. Like for like NGR in Q1 was up an impressive 18% with even the bwin brands showing an 11% growth. The acquisition is clearly the big news and the Cerberus loan is a bit of a concern – it is a very expensive form of funding and a bit of a shame the acquisition couldn’t be completed with a cheaper loan. There is no dividend for the coming year and the PE ratio looks expensive but skipping ahead to 2017, the shares look a bit cheaper with a PE ratio of 11.5. This is a tricky one – if the loan can be paid off quickly, this is probably a good investment. The Brexit vote is a bit of a worry at the moment though and overall I think the risks just about outweigh the potential rewards.

On the 23rd May the group announced that it had signed terms to license its online sportsbook and gambling platform to Betfred. The ten year transformational B2B agreement involves the full migration of Betfred’s online business including all its sportsbook and gaming offering, to the GVC platform on an exclusive basis. The board continue to see opportunities to drive revenues from its proprietary technology. This is a significant deal for the group and I am tempted to hop back in here.

On the 24th May the group announced that average group pro-forma revenues per day in Q2 are currently 11% higher than the corresponding period last year and 15% up on a constant currency basis.

On the 13th June the group announced that the New Jersey Division of Gaming Enforcement issued an order concluding its prelim investigation of GVC in connection with its acquisition of Bwin. They concluded that GVC possess the requisite good character, honesty and integrity should it file for a transactional waiver. They determined that the New Jersey licenses held by Bwin should remain valid under the new ownership, all of which is good news.

On the 13th July the group released a trading update covering Q2. Overall trading has been strong with both GVC (24%) and bwin (12%) brands achieving double digit growth on a constant currency basis. On a pro-forma basis NGR per day in Q2 increased by 11% with a growth in constant currency of 16%. The group benefited from an above average sports margin in the period of 9.9% with particularly favourable results during the first half of the Euro 2016 tournament.

In addition, pro-forma sports wagers per day increased by 9% in constant currency. Gaming NGR per day also grew by 11%, helped by improved cross-sell from sports and new casino content.

It is expected that the move to a premium listing will take place from the start of August, which should enable them to join the FTSE 250. The integration of the enlarged group is progressing in line with expectations and remains on track to secure €125M of synergies by the end of 2017. From an operational perspective in the short to medium term the board believes that the Brexit result will have little or no material impact on the group with 90% of the customer base coming from outside the EU.

Overall, although there is still much to do, the board remains confident for the rest of the year and after these results, I do too. If I can find a decent entry point I think I will buy back in here.

On the 1st August the group announced that it received approval by the UK listing authority to the transfer of the listing to the premium segment which should enable them to join the FTSE 250.

On the 2nd August the group announced that it had entered into a commitment with Nomura for a replacement of their financing which will be applied towards the repayment of the secured €400M loan with Cerberus, of which €386.5M currently remains outstanding. The Nomura loan will be a €250M unsecured loan at an interest rate of 2% above Euribor with the balance of the Cerberus loan being repaid from existing cash resources. This paves the way for a return to dividend payments in 2017.

The group have also reported that trading has continued positively with July like for like revenues per day up 26%, boosted by the Euro 2016 tournament. The net debt at the current time stands at €154.3M.

This is very positive news and I am happy to keep holding here.