Aureus Mining has now released its Q1 results for the year ending 2016.

Now that New Liberty has entered commercial production, the group has earned $8.3M in revenues with mine operating costs coming in at $7.7M. With a $2.6M impairment of ore stockpiles and $1.9M of depreciation, however, the group incurred its maiden gross loss of $2.9M. Legal and professional expenses increased by $132K but there was a $292K positive forex movement when compared to Q1 last year and after other expenses fell by $96K the operating loss grew by $2.6M. There was a $495K reduction in the warrant derivative loss but interest expense was up $867K to give a loss for the period of $5.6M, an increase of $2.9M year on year.

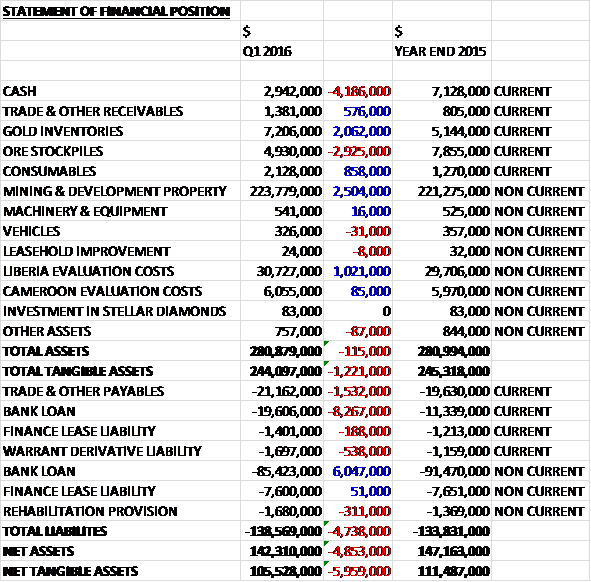

When compared to the end point of last year, total assets declined by $115K driven by a $4.2M decline in cash and a $2.9M decrease in the value of ore stockpiles due to a $2.6M impairment, partially offset by a $2.5M increase in the value of mining and development property, a $2.1M growth in the value of gold inventories as a result of restrictions in moving gold through Brussels airport, a $1M increase in Liberian evaluation costs, an $858K increase in consumables and a $576K growth in receivables mainly relating to prepaid insurance costs. Total liabilities increased during the quarter due to a $2.2M increase in bank loans, a $538K increase in warrant derivative liabilities and a $1.5M growth in payables. The end result is a net tangible asset level of $105.5M, a decline of $6M over the quarter.

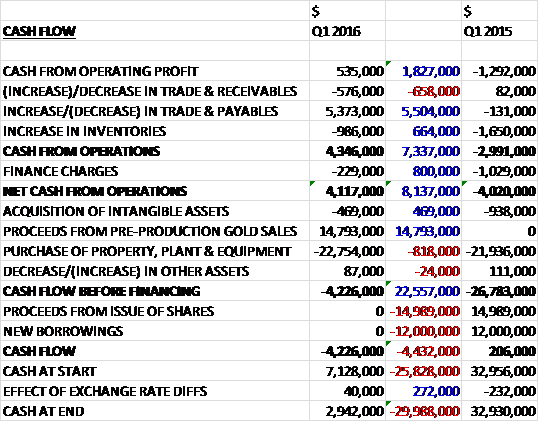

Before movements in working capital, cash profits came in at $535K, an improvement of $1.8M when compared to Q1 2015. There was a large increase in payables, however, and even after finance charges there was a net operating cash flow of $4.1M, a positive movement of $8.1M year on year. The group spent $469K of this on intangible assets and $22.8M on property, plant and equipment and after $14.8M of proceeds from pre-production gold sales, there was a cash outflow of $4.2M in the period and a cash level at the period-end of $2.9M.

During the quarter, the group mined 264KT of ore at a grade of 3.32g/t. Of this, the group milled 252,578 tonnes of ore at a grade of 3g/t which produced 22,706 ounces of old. They sold 19,249 ounces and the average realised price was $1,198 per ounce. Since the mine entered commercial production in March, the all in sustaining cash cost was $1,153 per ounce due to the low mining rates so there is still much work to do. Gold sales were impacted in March by restrictions on transporting gold through Brussels airport following the terrorist attacks with the gold stockpiled being shipped through a different route in April.

Excavation work continued to focus on the flood bund along the south of the final pit limit to prepare for the rainy season with an additional 456,648 tonnes of material moved during the quarter. Mining operations were focused upon both the Kinjor and Larjor starter pits and opening access to fresh rock before the onset of the wet season in late Q2.

Mining during the period was hampered by low excavator availability due to undercarriage problems with both of the excavators. Replacement undercarriages for these units were sourced and shipped to the mine in March. To improve production levels at the mine five new 100 tonne capacity haul trucks and one excavator were delivered in April and mobilised ready to start mining operations in May.

During the period, process plant optimisation activities continued with a particular focus on improving recoveries from the gravity circuit and in delivering operational improvements in CIL leach kinetics. Additionally, preventative maintenance activities were undertaken around the process plant with a view to improve plant availability. These activities resulted in more stable operating conditions being experienced in the process plant towards the end of the quarter.

As part of these optimisation activities, a fresh carbon supply was introduced into the Carbon in Leach tanks of the process plant. This resulted in an increase in overall gold recovery to levels in line with overall plant operating specs of about 90% recovery.

During the quarter exploration work focused on the near mine potential around the New Liberty mine with pitting and regolith mapping around the western portion of the Bea Mountain license. This work aimed to test for concealed mineralisation along major and secondary structures close to the New Liberty plant. Much of the soil sampling around the mine has been found to be in residual or depositional regimes and therefore pitting is needed to reach the saprolite sections. Pitting has been undertaken in order to check underneath these regimes and sample representative saprolite. The focus of this work is along major and secondary structures identified by geophysics.

The results from some of the pits along major structures have shown that there are some indicators of gold mineralisation which soil sampling did not detect. Further pitting is ongoing to follow this gold anomalism and define targets for further work. Other areas of structural and regolith interest have been selected for geological mapping in Q2.

At Ndablama, throughout the quarter pitting on additional soil anomalism was undertaken to the south and to the west in order to gain a better understanding of the geology of the area and testing additional areas of mineralisation which have not been previously identified. At Weaju, in Q1 mapping along the SW of the project shows the potential to increase the strike of mineralisation for another 800m to the SW. Further mapping and sampling will be done going forward to better define the surface expression of mineralisation.

At Leopard Rock, pitting has been undertaken to test the surface continuation of mineralisation following on from detailed mapping of the Ndablama project the results of which will enable further follow up work in Q2. Detailed mapping of the 8km extent of the Yambesei shear zone was completed during Q4. Pitting along the entire length of the Yambesei shear was started in Q1 and has been completed over Gondoja, Musa and Gbalidee. Further pitting will be undertaken in Q2 focusing on Welinkua and Koinja.

At Silver Hills, work focused on the Belgium target during Q1 with pitting and mapping having increased the strike extent of mineralisation to 1km. This mineralisation which is highlighted by a NE trending shear has the potential to extend over 3km up to the Bruges target located in the NE. Detailed soil sampling and pitting was undertaken during the quarter connecting Belgium target to Antwerp. Channel samples highlighted the potential for high grade zones, associated with intense silicification and shearing. Further pitting, mapping and soil work is ongoing at this target to further trace the mineralisation along strike.

At the Matambo Corridor, during the quarter geological mapping started in the eastern part of the 15km gold corridor. It covered the area around the Bomafa prospect and resulted in locating a main band of greenstone which underlies the soil anomalism with lithosamples confirming the trace mineralisation at surface. Mapping will continue during Q2 with the aim to cover the remaining part of the corridor towards Bangoma and Saanor.

The latest Ebola flare-up occurred in Guinea in March and resulted in a high risk contact travelling to Liberia resulting in three confirmed cases. On 29th April, Liberia began a 42 day period of increased surveillance and following this period if there are no new cases the country will once again be declared Ebola-free.

As previously announced, the process plant detoxification circuit has now been operating to original design specs resulting in higher concentrations of cyanide WAD in the process effluent. The group had therefore been operating with process water in a closed circuit.

Recent heavy rainfall resulted in a small overflow of effluent from the Tailings Storage Facility onto the wetlands area. The group is conducting remediation work to rectify the issues in the detoxification circuit and to manage future water discharge from the TSF in order for processing operations to restart in the near future. The investigations to date indicate that there has been no adverse impact on any human settlement but further investigations are in progress and in view of this leakage, a decision was taken to suspend processing operations on May 7th.

The group is working with the appropriate authorities and local communities in order to mitigate against any environmental related risks. The EPA is in the process of reviewing and approving the proposed remediation work required to rectify the detoxification circuit and to manage future water discharge from the TSF. Approval from the EPA and MLME is required before gold processing operations cam restart and the company is working to develop a start-up plan to recommence processing as soon as possible.

During this temporary suspension of processing operations the group is taking the opportunity to effect a mill reline, undertake other preventative engineering maintenance and repairs as well as modifications to the detox circuit proposed by the expert consultants. Furthermore mining operations are continuing at New Liberty in order to build up ore stockpiles and undertake waste stripping.

In January the company completed the acquisition of Sarama Investments which holds the Cape Mount licenses for a total consideration of 5,648,310 Aureus shares. The acquired licenses are contiguous to the company’s Bea Mountain license and are located close to the New Liberty mine. As a result of the acquisition, the group’s total land portfolio in Liberia has increased to 1,683km2 from 1,402km2.

The company has net current liabilities of $25.3M and has about $19M of debt repayments due over the next year. Based on discussions with the lenders to date, there is a reasonable expectation that they will be able to agree a debt repayment schedule but there is material uncertainty which may cast significant doubt about their ability to continue as a going concern. The loan facilities are fully drawn and the senior facility’s first repayment of $3.1M was originally supposed to be in January. This has so far been deferred to the end of this month but I would have thought it would have to be deferred again. The company currently has $5.5M of cash and is monitoring its working capital position closely.

On the 23rd May the group released an update. They have made good progress towards its objective of achieving a controlled start-up of the gold processing plant within the next two weeks subject to final approval of the MLME. The EPA has granted permission to proceed with the construction of holding zones within the wetlands area downstream of the tailings storage facility which will enable better aeration of surface waters and improved retention times. They have engaged technical experts to assist with various modifications within the process plant and detoxification circuit to ensure that discharges into the TSF comply with environmental and operational permits.

A number of technical studies by international consultants are underway, to review the company’s environmental and social actions plans and ensure compliance with the IFC’s performance standards. Ore stockpiles currently stand at about 73,431 tonnes at a grade of 3.78g/t. Total production for the year to date is 30,000 ounces.

Overall then this was another difficult period for the group although in some ways some progress has been made. They are still loss making and net assets fell over the quarter but there was a cash profit made and the delay in making payments to suppliers meant that there was actually a decent amount of free cash produced. Unfortunately it is not enough to keep the lenders at bay and the most recent repayment deadline is looming.

There were further operational problems during the period with issues associated with the excavators and after the end of the quarter, the released of cyanide into the local environment has caused processing operations to be suspended for much of May. With the debt repayment looming, this is very poor timing and this company seems far too risky to invest in at the moment.

On the 1st June the group announced that it had received approval from its lender group to further defer its first debt repayment to the end of June. The company continues to progress towards its objective of achieving a controlled start-up of the gold processing plant with plant modifications and remediation measures to optimise the detoxification circuit meeting completion. The board expects to receive approval to recommence processing operations in the coming days but for now they are still on stand-still and I can’t see any other outcome other than a large placing to clear the debt here.

On the 9th June the group gave an update regarding production. The EPA has granted the company permission to discharge from its Tailings Storage Facility and issued a permit for future discharges in compliance with the International Cyanide Management Code limits. A detailed start-up plan has been submitted to the ministry for formal approval and modifications to the gold processing plant and detoxification circuit are nearing completion.

The re-start of gold processing operations is currently targeted for mid-June following the completion of gravity circuit screen replacement works and a full mill reline. Mining operations have continued with a current run of mine ore stockpile balance of about 105,694 tonnes at a grade of 4.02g/t.

Prior to the re-start of processing operations, the group intends to complete a full reline of the ball mill which was previously scheduled to be undertaken at the end of June. This reline involves the mill being fitted with more heavy duty liners than originally supplied and improved lifters and grates.

The detailed start-up plan submitted includes a gradual ramp up in operations with waste and low grade ore towards name plate capacity at ROM grade ore, and including scheduled periods of plant downtime to allow for performance testing and additional modifications to be made within the process plant. It is anticipated that this controlled start up process will be started with the support of staff from the MMSA.

Investigations to date have shown that cyanide discharge exceeding ICMC compliance guidelines and the environmental laws of Liberia have been recorded on the TSF and downstream from the TSF periodically since mid-December. These exceedances can be attributed to operational issues at the plant, including complications with the oxygen plant, the detoxification circuit and on site lab resulting in a lack of stable operating conditions.

On the 15th June the group announced that it had entered into an agreement for an equity financing with MNG Gold. The $30M equity investment at 3.21p per share represents a premium of 22% to the closing price of the previous day. MNG will become a 55% shareholder in the group and will appoint three representatives to the board. Serhan Umurhan will be appointed CEO and Geoff Eyre as CFO.

MNG Gold has assets in Turkey, Burkina Faso and Liberia and is owned by Mehmet Gunal. Funds raised will be used to reduce outstanding creditor balances, increase working capital and facilitate the ramp up of the processing plant. The group has also received credit approval from its lender group for a four month default waiver during which time they will work to reschedule the debt repayment profile.

The financing will be completed as a private placement with two tranches. The first will be 59,533,674 shares and a promissory note of $12.3M to MNG. Tranche 2 will be 331,111,209 shares at a price of 3.21p for aggregate gross proceeds of $15M. The promissory note will be unsecured and will bear interest at 12% per annum. The principle amount will be converted into shares at 3.21p per share and will automatically convert into shares with the closing of tranche 2 of the offering as long as the required PIFs are cleared by the TSX. Should they be rejected, the promissory note will be payable six months from the date of issue.

Current CEO and CFO David Reading and Paul Thomson will resign, although Paul will continue for another year in a consultancy role. With the price now at 3.87p, I am very surprised it has held up so well.

On the 23rd June the group announced that it has received approval for the plant start up process. They also stated that they now have adequate funding available to support working capital needs and preparations are underway for the commencement of the plant pre-start procedure which will be initiated following the arrival of a consignment of additional reagents that they are working to expedite to the site.

On the 15th July the group announced that it had closed tranche 2 of the equity financing with MNG Gold pursuant to which the company has issued 331,111,209 new shares at a price of 3.21p per share to MNG, raising proceeds of $15M. The promissory note in the principal amount of $12.3M automatically converted into 271,577,546 shares so an aggregate of 662,222,429 shares have been issued.